Skip to main content

Skip to main content

Tunisia: Ben Ali's founders face transition

Ahmed Abdelkefi built two things. His restaurant Dar El Jeld has defined traditional Tunisian fine dining for 35 years. His investment firm became AfricInvest — Africa's most active PE fund, documented in 25 countries. He is in his mid-eighties. Neither has a succession plan.

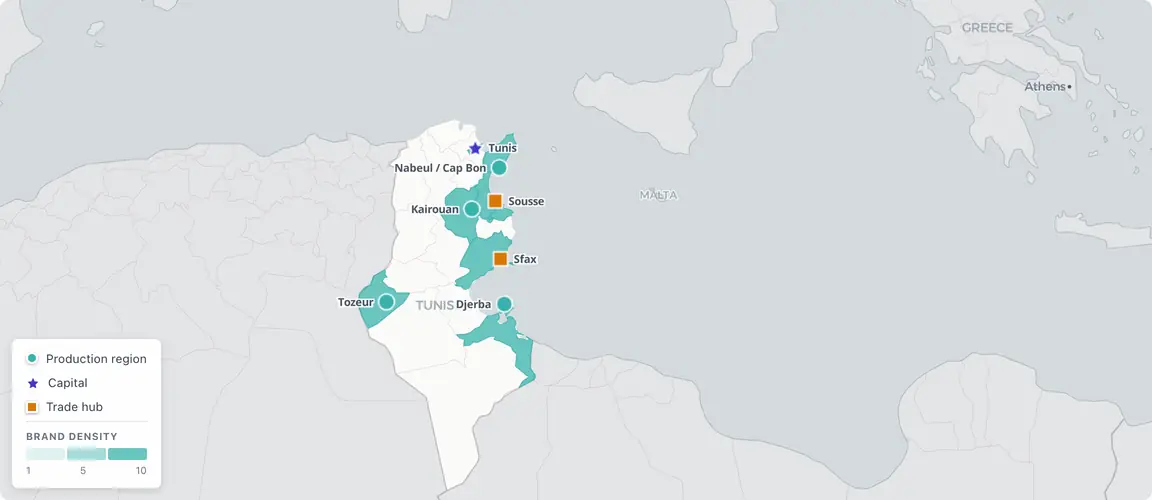

Tunisia's founder-owned brand geography: coast, medina, and estate

The Ben Ali generation, 1987–2024

Ahmed Abdelkefi built two things that define Tunisia’s founder economy. The first is Dar El Jeld: the restaurant that has anchored traditional Tunisian fine dining in the UNESCO-protected medina of Tunis since 1989, known across the Maghreb for its plaster-lattice courtyards and the cuisine of the old Hafside city. The second is Tuninvest, founded in 1994, which grew into AfricInvest — one of Africa’s most active private equity firms, documenting investment readiness and succession risk across 25 countries in consumer goods, financial services, and healthcare. Abdelkefi is now in his mid-eighties. Neither institution has a publicly documented succession plan.

This is not an exception. It is the structural condition of the Tunisian founder economy in 2026: a country that built the institutional infrastructure to document succession intelligence for the rest of the continent, while leaving its own founder-owned brands — more than 150 at commercial scale in six sectors, built during Ben Ali’s economic opening between 1987 and 2010 — without a single database record, investment filing, or succession structure. The intelligence apparatus exists, headquartered in Tunis. It has not been turned inward.

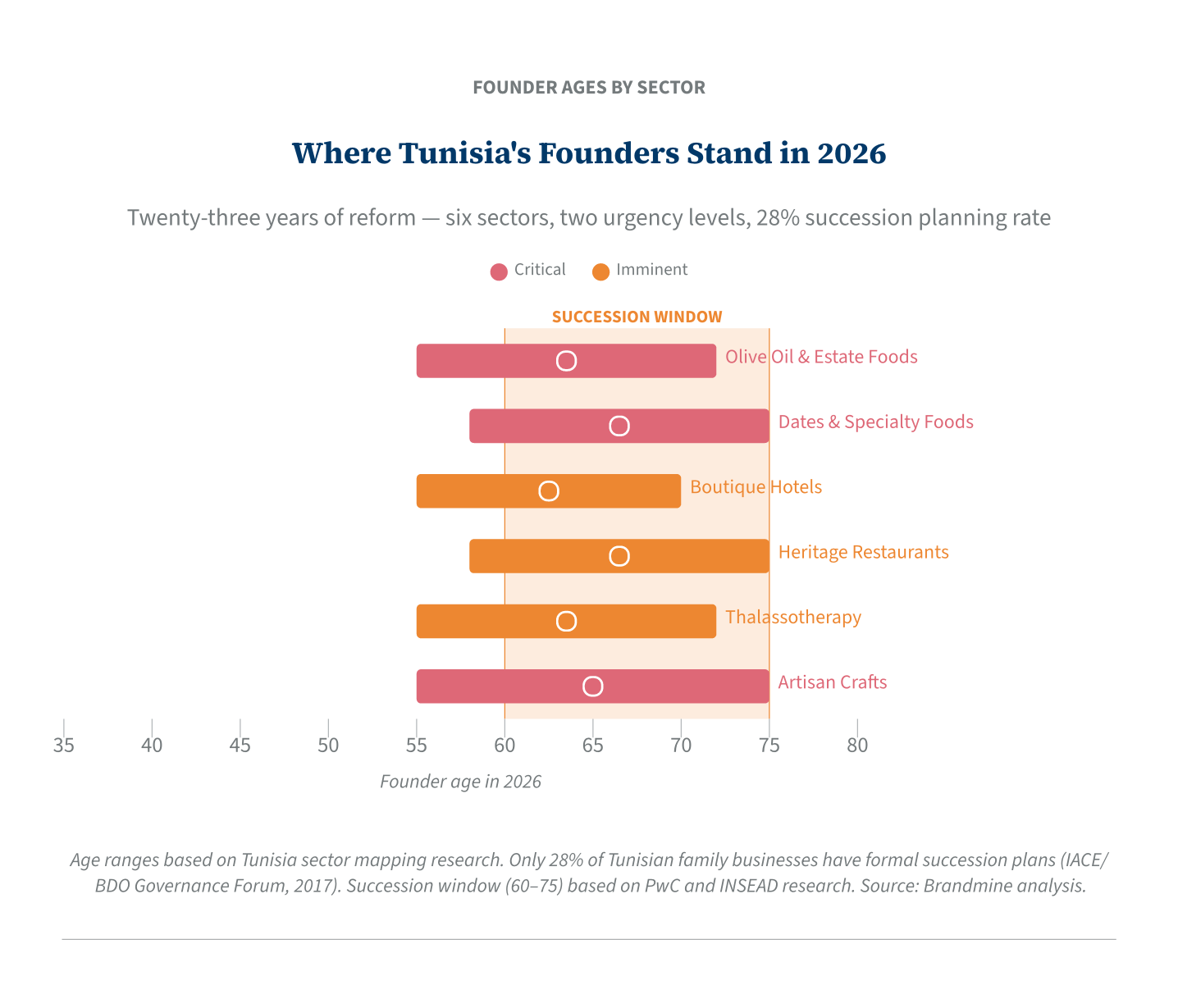

Tunisia’s founder generation belongs to the same synchronized transition wave Brandmine documents across emerging markets — the 28,000 founder-owned consumer brands at commercial scale whose founders built during the reform eras of the 1980s and 1990s and are now entering the succession window simultaneously. In Tunisia, the reform wave ran for twenty-three years. Across olive oil estates, harissa dynasties, boutique hotels, heritage restaurants, thalassotherapy centres, and artisan craft operations, the succession emergency it produced is arriving now, sector by sector, with no institutional infrastructure to manage it and no synthesis of the intelligence that would allow an outside investor to act.

Ben Ali’s dividend: twenty-three years of founder formation

Tunisia has welcomed 10.25 million foreign tourists in 2024, surpassing pre-pandemic figures.

Tunisia’s founding wave differs structurally from almost every country in Brandmine’s universe in one fact: it lasted a generation. Most emerging-market succession waves were compressed by a single reform rupture — Mongolia’s private sector was created in roughly two to three years after the 1990 democratic revolution; Russia’s voucher privatization ran from 1992 to 1997. Tunisia’s wave, opened by Ben Ali’s coup in November 1987 and sealed by his flight in January 2011, ran from one end of a generation to the other.

Law 87-51 reorganized the relationship between the state and the private sector. An extended privatization program sold off state-owned enterprises across agriculture, food processing, tourism, and light manufacturing. The consequence was not one founder cohort but two. The early wave — founders who entered the market between 1987 and approximately 1995 — are now 65 to 75 or older. They represent Tunisia’s most acute succession cases. The late wave — founders active from 1995 through 2010 — are now 55 to 65, approaching but not yet at peak transition pressure.

Both cohorts arrive at 2026 with the same inheritance problem. Tunisia’s family business sector is, structurally, an economy without succession infrastructure: no sustained family-office advisory tradition, no PE fund explicitly targeting founder-to-successor transactions in consumer brands, and a legal and currency framework that makes diaspora capital reentry operationally complex. The IACE/BDO Governance Forum study, the most comprehensive assessment of Tunisian family business succession readiness to date, found in 2017 that only 28 percent of Tunisian family businesses had implemented formal succession plans. Thirty-nine percent had none at all. The family businesses in that study account for approximately 70 percent of Tunisian GDP and 90 percent of industrial firms.

Three crises have since concentrated the succession pressure further. The 2011 revolution disrupted approximately 400 enterprises linked to the Ben Ali and Trabelsi families — confiscations that damaged or rerouted some brands while leaving others untouched. The 2015 Bardo Museum and Sousse terror attacks collapsed tourist arrivals for two years and pushed the hospitality sector to near-closure. COVID-19 delivered the third blow: eighteen months of near-zero international travel for an economy whose founder-owned hospitality brands had been built on European visitor flows. The operators who held through all three are now the most crisis-documented founder cohort in North Africa. They are also the most urgently approaching transition.

Six sectors, one generation, no succession documentation

Olive Oil & Premium Estate Foods — Critical urgency. An estimated 25–40 founder-owned estates operate at commercial scale, with founder age bands of 55–72. Tunisia controls approximately 20 percent of the world’s certified organic olive groves — the production scale is among the most significant in global organic commodity supply. The premium segment is less documented: family estates with named founders, award-winning extra-virgin output, and export relationships across France, Germany, and the Gulf. Ben Ali-era founders — Topoliva (Djerba, 1991), Barhoumi (Kairouan), Domaine Chograne — are in or entering the succession window peak. A sector spotlight is on Brandmine’s research roadmap.

Dates & North African Specialty Foods — Critical urgency. An estimated 15–25 founder-owned brands operate at commercial scale, with founders aged 58–75. The anchor brand is Boudjebel/VACPA (Sfax, founded 1982), led by third-generation CEO Ahmed Boujbel: a world leader in Deglet Nour date exports, shipping more than 18,000 tonnes annually to four continents under Fair For Life certification. The second anchor is Le Phare du Cap Bon — the harissa brand Bakha Gastli founded in 1946 with a French partner and now in its third generation under Sofiene Gastli, one of the oldest surviving founder-family-led consumer operations in the Maghreb. Harissa is globally trending as a premium condiment. The founder-owned Tunisian brands defining the premium segment are entirely undocumented.

Boutique Hotels & Maison d’Hôtes — Imminent urgency. An estimated 20–30 founder-owned properties operate at commercial scale, with founders aged 55–70. Tunisia’s boutique hospitality operators have survived three consecutive existential crises: the 2011 revolution, the 2015 terror attacks, and the 2020–2021 COVID collapse. Tourism Minister Sofiene Tekaya confirmed in January 2025 that Tunisia had welcomed 10.25 million foreign tourists the previous year, surpassing pre-pandemic levels. The maisons d’hôtes of Sidi Bou Saïd, Djerba, and the historic medinas that held through the decade of crises now arrive at the succession threshold simultaneously. Dar Saïd in Sidi Bou Saïd, Tunisia’s first boutique hotel (inaugurated 2001), is the cluster’s reference property.

Heritage Restaurants & Traditional Cuisine — Imminent urgency. An estimated 8–15 establishments operate at commercial scale, with founders aged 58–75. The defining cluster is the Abdelkefi portfolio — Dar El Jeld and Fondouk El Attarine, both in the UNESCO-protected Tunis medina — operated by a founder now in his mid-eighties. These are not heritage-tourism novelties; they are Tunisia’s most referenced traditional dining addresses across three decades of international travel coverage. No publicly documented succession structure exists for either.

Thalassotherapy & Wellness Tourism — Imminent urgency. An estimated 8–12 independent founder-owned centres operate at commercial scale, with founders aged 55–72. Tunisia is Africa’s most developed thalassotherapy market and the world’s second-largest after France. Of approximately 60 centres, 84 percent are hotel-annexed — a filter that leaves roughly ten independent founder-operated businesses generating approximately 200 million TND (~$63M USD) annually. Bio Azur Hammamet, Tunisia’s first thalasso centre (founded 1994), is the sector’s anchor. The pool is small; the signal quality is high.

Artisan Craft Brands (commercialized) — Critical urgency. An estimated 15–25 brands have moved from artisanal production to commercial distribution at scale, with founder age bands of 55–75. ONAT registers approximately 200,000 artisans in Tunisia; the commercialized-at-scale subset represents a concentrated succession window. Multi-generation pottery dynasties in Nabeul are mid-transition now — the founding patriarchs of several prominent ceramic families have recently entered the final decade of active management, with succession structures largely unresolved. A sector spotlight is on Brandmine’s research roadmap.

The AfricInvest paradox

The succession infrastructure problem in Tunisia is not a gap — it is a structural misdirection. AfricInvest manages what it describes as Africa’s most active PE fund, with documented investments across 25 countries and a Maghreb PE Fund IV that closed its first tranche at €152 million in 2018, backed by the European Investment Bank, British International Investment, SwissCap, and FMO. Its portfolio documentation, investment methodology, and succession analysis cover companies from Dakar to Nairobi. It has produced no publicly available analysis of the succession risk embedded in the founder-owned consumer brands operating in the city beneath its headquarters.

This is not a criticism of AfricInvest — it is a description of the intelligence gap the Brandmine methodology is designed to fill. The Francophone and Arabic press corpus that documents these brands is extensive; it has simply not been synthesized for the international institutional investor audience that would act on it. The Gulf family offices already active in the Maghreb, the European specialty food distributors with established Tunisia relationships, and the diaspora capital that understands these markets — none of them have access to organized succession intelligence on Tunisia’s founder cohort. That gap is the opportunity.

Two factors add operational complexity. The Saied consolidation of 2021–2023 and Tunisia’s currency non-convertibility regime restrict the speed with which international capital can reenter the market through managed succession transactions. This is friction, not prohibition — the most logical buyers, Gulf family offices already active in the Maghreb and European specialty food distributors with established Tunisia relationships, face fewer of these constraints than diaspora-based investors. And the Ben Ali-era ownership context means that some pre-2011 brands require ownership history verification before commercial engagement — standard Narrative Due Diligence practice, not a disqualifying filter. The research protocols that handle this complexity already exist; the synthesis applying them to Tunisia’s consumer brand ecosystem does not.

The IACE/BDO finding — 28 percent succession planning rate, 39 percent with no plan at all — reflects the broader family business population. For founder-owned consumer brands at commercial scale, where enterprises were built by individuals during a reform wave rather than inherited through generations of family business tradition, the succession planning rate is almost certainly lower.

Documented in the press, absent from every database

The three crises that defined Tunisia’s 2011–2021 decade did not eliminate the founder cohort. They documented it in ways that no database has yet captured. The brands that kept operating through political transition, collapsed tourist arrivals, and near-zero hospitality revenue are not merely survivors — they are the crisis records. The Narrative Due Diligence material that makes these brands documentable exists precisely because they held through conditions that would have ended less resilient operations.

The succession arithmetic is straightforward. The 1987–1995 founding cohort is 65 to 75 or older in 2026. The IACE/BDO study data is from 2017; nine years later, the urgency is higher and the documentation has not changed. The Abdelkefi cluster at Dar El Jeld, the Barhoumi olive oil estate in Kairouan, the Gastli family’s harissa brand at Le Phare du Cap Bon, Bechir Ben Maad’s Topoliva on Djerba island — these are not hypothetical succession cases. They are succession cases in progress, documented in the Francophone press, accessible to a researcher who looks, and absent from every institutional investor database. The press trails are there. The corporate registry filings exist. The research requires Arabic and French, familiarity with Tunisian business culture, and the synthesis methodology. None of those are available in the sources that institutional investors habitually consult.

Tunisia’s olive groves have been producing oil since before Rome was a republic. The estates selling premium oil from those groves today are run by founders who are 60, 68, 72 years old. The century that separates their olive trees from theirs is not the risk. The next decade is.