Skip to main content

Skip to main content

Thai Wellness: After the Acquisition Wave

In March 2025, Nikkei Asia placed Karmakamet alongside Gentle Monster and Cotti Coffee as Asia's most coveted retail tenants — while the brand had never opened a single international store and had never taken a baht of debt. Japan had just paid premium prices for the Thai wellness brands on the same Sukhumvit block. Two founders were still there.

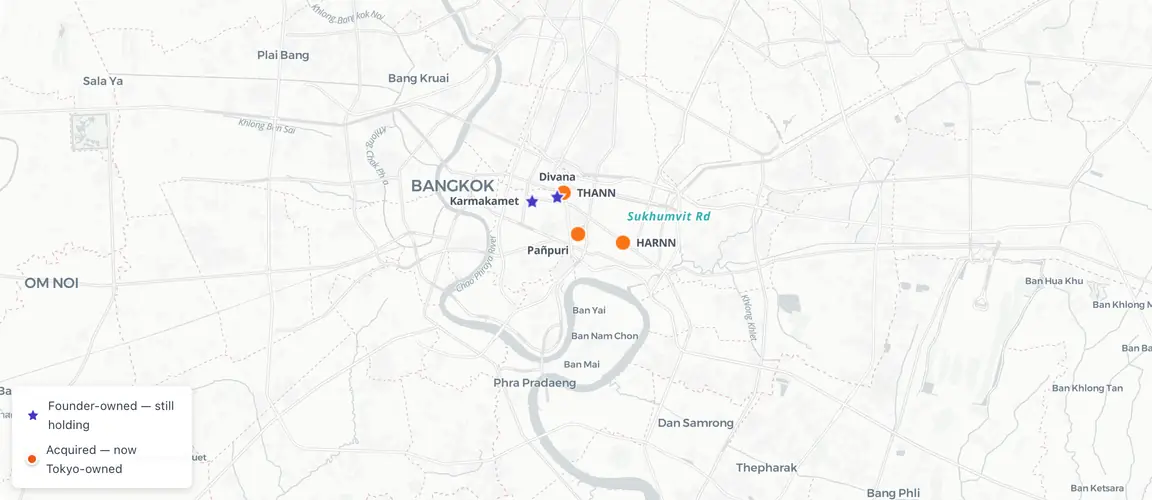

Bangkok's Sukhumvit Corridor — Holdouts and Departed

Who stayed after the buyers came

In March 2025, Nikkei Asia published its annual list of Asia’s most coveted retail tenants — brands that Japanese mall developers were actively pursuing for flagship positions. The roster placed Karmakamet alongside Gentle Monster, the Korean eyewear brand whose stores generate thousand-dollar queues before opening, and Cotti Coffee, the Chinese budget chain expanding across Southeast Asia. Karmakamet, the Bangkok aromatherapy brand, had never opened a single international store. It had never accepted a baht of external capital. Its founder had spent four years studying Buddhist dharma after a business partner defrauded the company.

Japan, meanwhile, had just paid premium prices for the Thai wellness brands on the same Sukhumvit corridor where Karmakamet operates. The acquisition wave that ran from 2018 to January 2026 consumed an entire generation of crisis-born Thai wellness brands — HARNN, Pañpuri, THANN, and Erb — all of them purchased by Japanese conglomerates and Thai holding companies within seven years. The brands that sold were born from the same 1997 Asian Financial Crisis, built on the same Bangkok geography, and trained on the same crisis-discipline playbook as the two that didn’t.

The geography of staying

Bangkok’s Sukhumvit corridor — the 10-kilometre stretch from the Chidlom and Ratchaprasong intersection east toward Thonglor — produced an improbable concentration of premium Thai wellness brands across the two decades following the 1997 baht collapse. HARNN established its first retail locations here. Pañpuri built its flagship in the same geography. THANN positioned its Bangkok presence within the same arc. Divana operates three of its seven luxury spas within walking distance of each other in this corridor. Karmakamet’s flagship sits at Siam Square, at the western edge of the same Skytrain line.

The brands that sold are now controlled from Tokyo. Kosé Corporation closed on Pañpuri in December 2024; Rohto Pharmaceutical signed for 51% of THANN one month later. Both transactions were documented by PitchBook, Bloomberg, and Nikkei. The brands that didn’t sell — Divana and Karmakamet — are still where they started.

This is the fact that no deal platform has indexed. PitchBook’s documentation of the acquisition wave is complete, transaction by transaction, acquirer by acquirer. Its documentation of the brands that stood in the same corridor and declined to sell is absent. Those decisions were made in Thai-language press, founder podcast appearances, and Siam Commercial Bank success-story interviews that no institutional analyst systematically reads.

What the databases miss

The intelligence gap is structural, not incidental. Thai private company ownership decisions are not disclosed through the same channels as listed-company transactions. What exists is distributed across Prachachat Turakij (ประชาชาติธุรกิจ), founder podcast archives, and publications like ManGu Magazine — all in Thai, none of them indexed by any English-language deal intelligence system.

PitchBook tracked both the Kosé-Pañpuri and Rohto-THANN transactions. It contains no record of the conversations Divana and Karmakamet declined to have — no documentation of the offers considered, the rationale for refusal, or the operational decisions that followed. That documentation exists. It has never been assembled in a language institutional capital reads.

The result is a specific blindspot: two brands at the same export and scale inflection point their sold peers occupied before Tokyo arrived — documented exclusively in Thai-language press, invisible to the screens that would otherwise surface them.

Divana: the prepared founders

In October 2001, Swissair dismissed all non-Swiss citizen employees following the airline’s financial collapse. The September 11 attacks had accelerated a liquidity crisis already underway, and the restructuring eliminated every position held by non-nationals within weeks. Among those laid off were two Thai cabin crew — Pattanapong Ranuraksa and Thaneth Jiraswakedelok — who had spent years absorbing Swiss service standards on international routes.

They had been preparing for this.

“On the day we were laid off, we saw three types of people,” Pattanapong told Siam Commercial Bank in a 2019 interview. “The first type cried and didn’t know what to do. The second type protested angrily and threatened to sue the company. And the third type were people who had prepared themselves for the situation before it happened — that was us.”

What they had prepared was a luxury day spa concept. While still flying international routes, Thaneth had written his academic thesis on the feasibility of the Thai spa market. He had documented the gap: thousands of affordable massage shops, ultra-luxury hotel spas at five-star rates, nothing delivering Swiss-caliber service consistency with Thai healing tradition at a middle-premium price point. They had the thesis. They had the service standards. They had the crisis.

They invested their remaining savings to fit out four treatment rooms on Sukhumvit — 90,000 THB (~USD 2,000) after fit-out costs. For three months, they worked from 8 AM to 1 AM performing every function from CEO to housekeeper. Revenue was insufficient for cash flow. A friend on opening day predicted “your business won’t last.” By months four and five, word-of-mouth ignited and revenue never stopped growing.

Twenty-five years later, Divana operates seven luxury spas across Bangkok, Chiang Mai, and Phuket — each housed in a century-old heritage mansion that no chain spa can replicate — plus a medical spa brand, three cafés, a therapist training academy, and more than 250 aromatherapy SKUs. Annual revenue reached an estimated THB 300–400 million in 2024. The 2025 target is THB 600 million, with THB 100 million in new investment committed for Pattaya and expanded Chiang Mai operations.

COVID-19 was the second existential test. With 80% of clientele being international tourists, Thailand’s border closures eliminated most of Divana’s revenue base. CEO Pattanapong described the crisis in Prachachat Turakij as having “completely reset all business to zero.” The company kept approximately 500 employees through the closure. It accelerated e-commerce through Shopee, Lazada, and TikTok Shop, expanded its medical spa concept targeting domestic customers, and grew product retail from a secondary revenue stream to roughly half of total income. Products now include a 250+ SKU aromatherapy line selling through six King Power duty-free outlets, international retail channels, and the brand’s own platforms.

No institutional capital was raised. No acquisition conversation reached a term sheet. The two founders who had prepared before 9/11 did the same before COVID — and the crisis discipline they built under a “Swiss watch” philosophy of precise, punctual, premium service carried through both.

Karmakamet: three crises, zero debt

Natthorn Rakchana’s grandfather had been a Hainanese Chinese medicine trader in To Deng subdistrict, Narathiwat Province — Thailand’s restive deep south — making incense from traditional recipes. He ceased production the year Natthorn was born, 1971. Natthorn grew up in Bangkok, studied interior design, and won Thailand’s Subannahongsa Award for costume design on the 2003 cult film Angulimala. He could have stayed in cinema.

Instead, he bought 200 kilograms of essential oils and opened a stall at Chatuchak Weekend Market. The founding product: incense blended from his grandfather’s Hainanese recipes, priced at 360 THB when the market standard was three items for 100 THB.

For the first eight months, monthly revenue equalled exactly the cost of rent — 12,000 THB. “I remember the first 8 months after opening, we sold only 12,000 baht per month — exactly equal to the rent. That means those 8 months were an absolute disaster,” he told thematter.co in 2017. He and co-founder Sommarat Phithakkingthong survived on 2,000–3,000 THB per month in personal income each. Month nine: a new product launch delivered 80,000 THB in a single day — 6.7 times the entire previous monthly revenue. The inflection was permanent.

The second crisis was more personal. During Karmakamet’s growth phase — estimated 2007–2012 — business partners defrauded the company. The betrayal triggered a broader partnership restructuring. “The ego I thought I could use as a tool for building my life — it collapsed. I was completely devastated,” Natthorn told ManGu Magazine in 2023. Rather than litigate or raise emergency capital, he entered four years of Buddhist dharma study and mindfulness practice, rebuilding the brand’s philosophical infrastructure from the ground up. One month after recruiting a new partner, the company was restructured and operational.

The framework that emerged from that retreat — a rejection of conventional business ambition, zero advertising spend, zero debt — became Karmakamet’s most durable competitive asset. “Success — this is a myth that the capitalist system designed as a tool to lull people into surrendering to the money game,” he told thematter.co in 2017. The brand has grown on word-of-mouth alone across its entire history.

COVID-19 delivered the third test. Ten of Karmakamet’s fourteen stores closed. The Karmakamet Diner restaurant at Phrom Phong shut permanently rather than sustain losses against zero revenue. But Natthorn had built an online sales department before the pandemic, anticipating digital market shifts. That team pivoted to e-commerce within weeks of the closures. By late 2023, Karmakamet operated 14 stores with plans for 7 more. By 2025, the network had reached 16 locations — and Nikkei Asia reported that Japanese mall developers had designated Karmakamet a priority “killer tenant” for their next expansion cycle.

Marketing manager Wisarut Chaloemsitthaphat confirmed international expansion plans for 2026–2027, with Japan as the priority market. The Japanese e-commerce platform karmakametshop.co.jp has been operational for years. US distribution runs through Amazon. Australian retail carries products through The Object Room. The physical international stores haven’t arrived yet. When they do, Karmakamet will join a retail export roll-out from the same country that just paid premium prices to acquire its direct peers. It has never taken a single baht in debt.

The pattern holds

Divana and Karmakamet are not isolated cases. Bobby Duchowny arrived in Phuket from Hollywood, where he had worked in film production. He discovered Thai botanical aromatherapy and founded Lemongrass House in 1996 on the same principles: zero external capital, zero institutional backing. The 1997 Asian Financial Crisis arrived in his first year. The December 2004 Indian Ocean tsunami devastated the Andaman coast infrastructure his Phuket-based production depended on. COVID-19 closed two years of hotel spa contracts globally. Lemongrass House survived all three, became a UNICEF supplier, and now operates 52 outlets across 12 countries. Still founder-owned.

Its 52-outlet footprint across 12 countries exceeds the international scale any of the four acquired brands had achieved at the time of their sale. HARNN operated primarily across Thai domestic retail when Tanachira arrived. Pañpuri’s reach was similarly concentrated in Bangkok hotel spa channels. Lemongrass House built an export operation larger than its acquired Bangkok corridor peers — from Phuket, not Sukhumvit, and without a baht of debt at any stage.

The pattern across Thai wellness brands that refused institutional capital is consistent. Each crisis that demanded a strategic decision was answered with an operational pivot — not a capital raise, not an acquisition conversation. The discipline was built into the brand from the start. The founders who built these companies treated the discipline as the asset, not the product.

The indicators Tokyo already screened for

Divana and Karmakamet now show the same export and scale indicators that HARNN, Pañpuri, and THANN showed three to five years before Tokyo arrived. Divana holds six King Power duty-free outlets, operates across multiple Thai cities, and targets THB 600 million in 2025 — the growth trajectory THANN was at before Rohto screened more than 500 Thai companies and selected it. Karmakamet is confirmed for Japan physical store expansion in 2026–2027, carries active US and Australian e-commerce distribution, and received the same “killer tenant” designation from Japanese mall developers that preceded the Gentle Monster and Cotti Coffee international roll-outs.

The strategic acquirer logic is visible in the transaction record. Kosé’s “Milestone 2030” strategy explicitly targets “regionally rooted brands” in emerging markets. Rohto selected THANN from a field of more than 500 candidates based on documented crisis resilience, export reach, and brand philosophy. Both Divana and Karmakamet satisfy the same criteria that Tokyo has already paid for twice. The difference is that neither brand has an English-language presence in any database that would surface them to the analysts running that screen.

Two Japanese conglomerates arrived on this corridor within thirty days of each other, in December 2024 and January 2026. That is the documented pace of the acquisition wave so far — two conglomerates, one corridor, one month.

What the corridor now shows

Five premium Thai wellness brands — HARNN, Pañpuri, THANN, Divana, and Karmakamet — built their primary operations within Bangkok’s Sukhumvit corridor. The corridor has not changed. The ownership has. The brands that sold are now controlled from Tokyo. The two that didn’t are still where they started, still operating the same crisis-forged discipline that made the acquired brands attractive in the first place.

PitchBook documents the acquisition wave. It does not document what remains.

What remains is two founder-owned luxury wellness brands at the export and scale inflection point, embedded in the same geography where Japan just paid to acquire their peers, documented exclusively in Thai-language press that has never been assembled in English.

Crisis discipline held Thailand’s luxury wellness sector together for twenty-five years. The brands that outlasted the acquisition wave — by refusing it — are now built on the same corridor, in the same Thai-language record, that Japan has already read twice.