Skip to main content

Skip to main content

Tanzania: The Generation Three Shocks Made

Tanzania's first-generation consumer brand founders survived three back-to-back crises in five years. Those who made it through — cashew processors, packaged food producers, safari operators — carry documented crisis histories that no investor database contains. One founder died in 2023. The succession window is already moving.

Three corridors: Tanzania's founder-owned brand geography

The off-the-record generation, 2015–2021

In May 2023, Abbas Moledina died in Canada. He had spent 46 years building Ranger Safaris into one of Tanzania’s oldest and largest independent safari operators — a company with a fleet of more than 120 vehicles, a reputation built on relationships with East African parks and communities, and no publicly known plan for what came next. Tanzania had no institutional infrastructure to manage the succession. The company’s transition is still unresolved.

Moledina was not the only one approaching that threshold. He was the first in a cohort — the founders who built Tanzania’s consumer brand mid-tier during the liberalisation waves of 1995 to 2015 — whose succession window is now open across three sectors simultaneously. The intelligence about these brands exists in Tanzania’s business press, the World Bank’s crisis documentation, and the records of the Tanzania Coffee Board and the cashew processors’ association. It has never been assembled for an investor audience.

The pattern is not unique to Tanzania. Across emerging markets, the generation that built founder-owned consumer brands during economic opening is entering a succession decade with no advisory infrastructure and no institutional coverage. What distinguishes Tanzania from comparable markets is not the window — it is the depth of the crisis documentation that preceded it.

Three shocks in five years

The 72% drop in the sector's revenues in 2020 closed businesses and caused layoffs.

Tanzania’s Wave 2 founders — those who established businesses during the Mkapa era of 1995 to 2005 — are now between 58 and 75 years old. Wave 3 founders, who built through the Kikwete high-growth decade of 2005 to 2015, are 45 to 65. Both cohorts were put through the same three existential tests within five years, and the tests are unusually well-documented.

The first shock was political. President Magufuli’s 2015 election launched unexpected tax enforcement: backdated VAT claims on goods already cleared through customs, port seizures of containers belonging to importers who had paid duties, and anti-corruption sweeps that targeted business practices that had operated openly for years. There was no appeal process that worked within commercial timescales. Businesses that survived did so by restructuring rapidly and, in some cases, by absorbing losses that would have bankrupted a less resilient operation.

The second shock arrived in 2018. The government bought the entire national cashew harvest at a fixed price, then defaulted on payments to farmers and processors. The export market froze. Processing facilities in Mtwara and the Southern Highlands sat idle for months while founders waited for payments that did not come. The documentation of this crisis — in the business press, in the cashew processors’ association records, in the seed-round filings of companies that survived — is among the cleanest crisis archives on the African continent.

The third shock was the one that produced the most distinctive documentation. Tanzania officially denied the existence of COVID-19. No lockdowns. No government support. No emergency credit lines. For hospitality operators and tour guides, that meant a 72% drop in sector revenues between 2019 and 2020 — with every business paying rent, wages, and loan instalments against zero income. The World Bank’s 16th Tanzania Economic Update documented the scale directly. An estimated 437,000 jobs were lost. The operators who stayed open and paid their staff did so on reserves, personal guarantees, and creditor relationships — and the decisions they made in those two years are all on the record.

No other sub-Saharan African market below the billion-dollar threshold has a founder cohort with three back-to-back crises documented across this range of sources in both English and Swahili. In Kenya, the 2007–2008 post-election violence produced documented crisis material — but it was concentrated in one sector and one region. In Uganda, the economic volatility of the 1990s and early 2000s predates the digital press archive. Tanzania’s three shocks arrived between 2015 and 2021, which means the coverage — press reports, seed-round filings, World Bank updates, trade association records — is both accessible and recent.

Three sectors, one open window

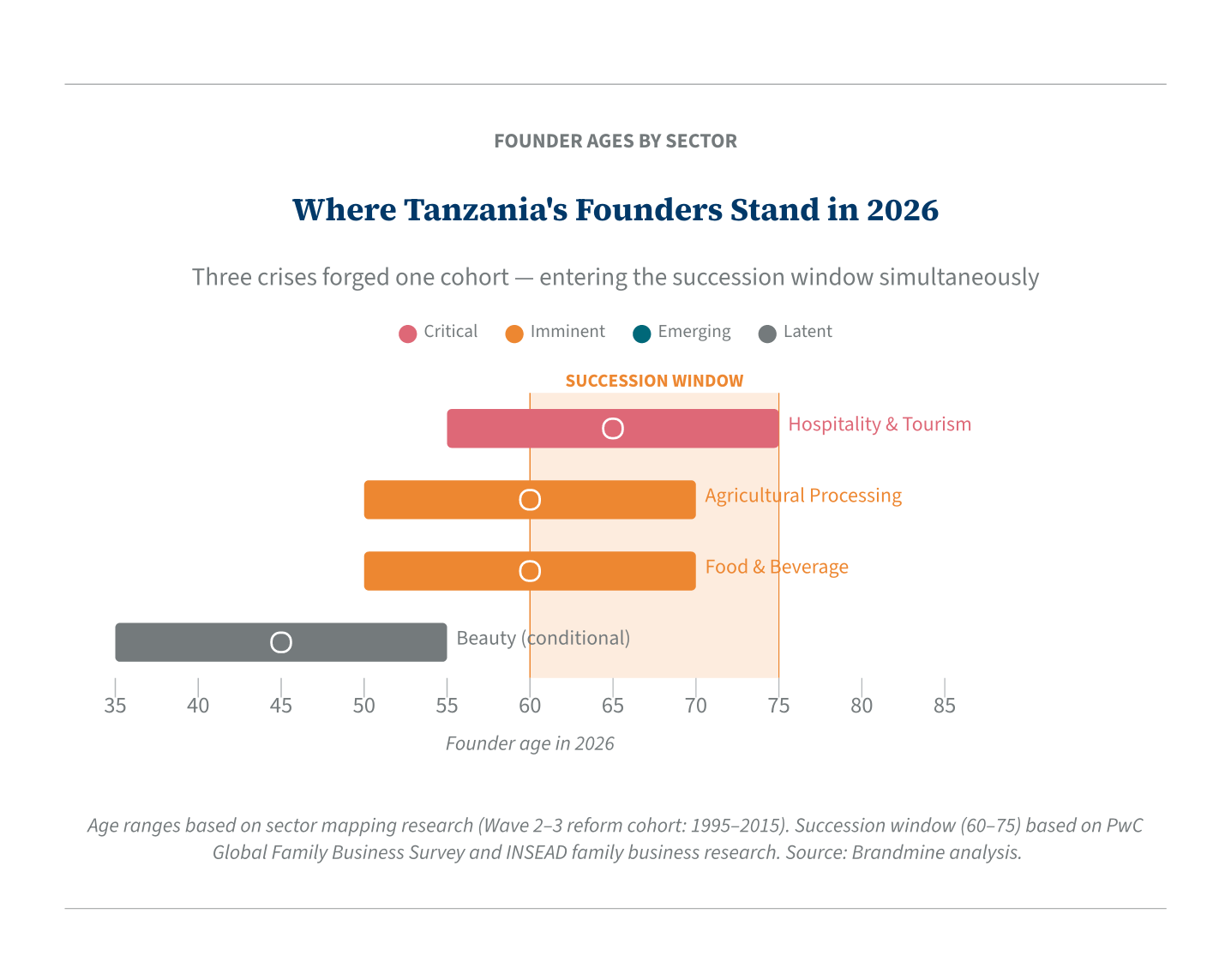

Three sectors carry the qualifying combination: a founder-owned mid-tier above the $5M commercial floor, documented crisis resilience, and succession pressure visible enough to be acted on now.

Agricultural processing with a brand layer is the highest-priority sector in Tanzania. It spans coffee roasting, cashew processing, packaged tea, honey aggregation, and spice exports — and the pool sits at 20 to 35 qualifying brands at commercial scale, making it one of the larger founding cohorts in East Africa. The NDD library for this sector is the deepest in the country: the 2018 cashew crisis is a documented event with paper trails through seed-round filings and press coverage; the COVID export logistics shock broke specialty coffee and tea routes to Japan and Europe and is well-attested in trade press. Tanzania’s coffee sector alone produces 70,000 to 80,000 tonnes of green beans annually, of which 93% leave the country before a Tanzanian brand can be put on them — the domestic roasting layer is small, founder-led, and invisible to every investment database. The succession urgency is Imminent across the sector, with the Wave 2 founders now in their late 50s to mid-70s. The commercial fit with Gulf and Singapore family-office mandates — which increasingly seek traceable-origin agricultural narratives — is strong and documented.

Processed food and beverage is the second priority, but this sector requires deliberate segmentation. The pool is barbell-shaped: at the top sit two conglomerates — Bakhresa Group, whose patriarch Said Salim Bakhresa was born in 1949 on Zanzibar, and MeTL Group — that dominate market visibility but are too large and too deeply held to represent succession opportunities in the conventional sense. The qualifying tier for Brandmine sits in the independent mid-range: roughly 20 to 35 packaged food and beverage brands at or approaching the $5M floor, many of them Indian-Tanzanian family enterprises with second-generation successors in place and succession frameworks that are more structured than the Bantu-Tanzanian tier. The ownership verification requirement is more complex in this sector than in agricultural processing: disentangling holding-company structures, confirming Tanzanian-citizen founding, and identifying whether a second generation is in place or whether the founder remains the sole operational authority is non-trivial research. The NDD documentation for this sector is centred on the Magufuli era: backdated tax claims, port seizures, and VAT disputes that hit every importer. Succession urgency across the mid-tier is Imminent.

Tanzanian-founded hospitality and tourism is the smallest qualifying pool — 12 to 19 brands — but it carries the highest individual NDD density in the country and the only live succession event already on the record. The pool is narrow for a specific reason: most of Tanzania’s boutique safari lodges and Zanzibar hotels were founded by expat operators — British, Dutch, American, German, Spanish — who arrived in the 1980s and 1990s and built properties that are visually iconic but fail the Tanzanian-citizen-founder filter that governs Brandmine’s core methodology. The qualifying subset is smaller and less visible: Tanzanian-citizen safari operators, lodge owners, and aviation founders who built through the same three shocks and, unlike their expat counterparts, had no European exit structure to fall back on. Succession urgency across this subset is Critical — Ranger Safaris is the first visible case, but the cohort includes several operators now in their 60s and 70s with no documented succession plan and no advisory infrastructure in Tanzania to help them build one.

Zanzibar warrants a note of its own. The semi-autonomous archipelago operates under separate ZIPA jurisdiction and presents a distinct mini-queue: spice value-add brands with resident-Zanzibari founders, and a halal wellness sub-sector that has grown since 2007. The archipelago is the world’s largest clove producer, and the spice value-add layer — resident-Zanzibari founders blending, processing, and certifying cloves, black pepper, and vanilla for export — is an early-stage but coherent cluster that warrants its own assessment, separate from the mainland Tanzania queue in both regulatory and founder-profile terms. Diaspora-founded “Zanzibari heritage” brands operating from the UK or United States — even those with local supply chains — are excluded; the filter is founder nationality at the time of founding, not supply chain geography.

What $63 billion conceals

Tanzania’s $63 billion GDP suggests a mid-income consumer economy with a broad founder tier. The reality is more concentrated. Two family conglomerates account for revenues in the range of $2.8 to $3 billion between them, and several of the country’s most visible consumer brands — Tanzania Breweries (AB InBev), Coca-Cola Kwanza, Serena Hotels (Aga Khan Fund) — are foreign-owned. Below them, the founder-owned tier at $5M and above thins sharply and concentrates into the three sectors described above.

The further complication is the expat-founded trap. Tanzania’s most photogenic consumer brands — its boutique safari lodges, its Zanzibar stone-town hotels, its specialty coffee estates — are disproportionately expat-founded. The Fox family, the Raguž family, the Asilia founders, Emerson Skeens: all of them arrived from Europe or North America, built recognisable brands, and constitute a hospitality sector that is internationally visible but irrelevant to the founder-transition thesis. A first-look assessment that conflates expat-founded and Tanzanian-citizen-founded brands will overstate the qualifying pool significantly. The sorting has never been done systematically.

The sorting also applies to the East African Asian tier. A third structural feature distinguishes Tanzania from other East African markets: the succession readiness divide between East African Asian families and first-generation Bantu Tanzanian founders. Families like the Bakhresans and the Dewjis have operated across multiple generations and have already moved second-generation members into senior operating roles — the transition is managed, if not complete. First-generation Bantu Tanzanian founders who built during the Kikwete era have no comparable succession tradition, no family business advisory infrastructure to draw on, and no institutional investor community focused on their sector. The succession dynamics of the two cohorts — and the documentation available for each — differ substantially, and conflating them produces a distorted picture of the qualifying universe.

The forge and what it left behind

There are no PE firms in Tanzania systematically targeting consumer brand transitions at the mid-tier. The advisory infrastructure — family business consultants, M&A intermediaries, succession planning specialists — does not exist for the $5M to $50M segment in Dar es Salaam or Arusha. Kenya and South Africa have developed family business advisory sectors; Tanzania has not. The Wave 2 cohort’s exits have no advisory structure to move through, and the terms of any transaction are set by whoever shows up with an offer. When succession is forced by a founder’s death — as it was for Moledina in 2023 — no institutional mechanism exists to respond quickly or to preserve the brand’s documented history.

The crisis documentation from 2015 to 2021 is a record of which founders were capable of surviving institutional pressure without institutional support. That is, in its own way, a due diligence filter more valuable than three years of audited financials — and it is sitting in the Tanzania Coffee Board’s press archive, the World Bank’s Tanzania Economic Updates, the cashew processors’ association records, and two years of English and Swahili business press that no one has assembled into an investor-ready format.

The argument for documenting these founders is not sentimental. It is structural. When a founder-owned brand transitions without institutional preparation — whether through death, retirement, or a forced sale under financial pressure — the brand loses the one thing that makes it worth acquiring: the founder’s documented relationship with crisis. That is what Narrative Due Diligence captures. And in Tanzania, across three sectors that were simultaneously stress-tested by the same sequence of government crackdowns, it is unusually available, unusually specific, and unusually verifiable.

The crisis documentation is already assembled. Three World Bank updates, a cashew nationalization that made international business press, two years of COVID denial that the African Journal of Hospitality put on the record — Tanzania’s Wave 2–3 founder cohort is the most crisis-documented group in sub-Saharan Africa below the billion-dollar threshold. What does not exist is the succession intelligence. Said Salim Bakhresa is 77. Tanzania has not yet appeared on a Bloomberg terminal.