Skip to main content

Skip to main content

How Beast Became the Hermès of Flowers

Amber Xiang refused a price list, a catalogue, and conventional orders. She asked strangers to tell her their stories — and built bouquets around them. That 2011 thesis turned Beast into China's fragrance category leader with RMB 418M in sales. The story is worth more than the product. Here is why that ceiling is impossible to cross from below.

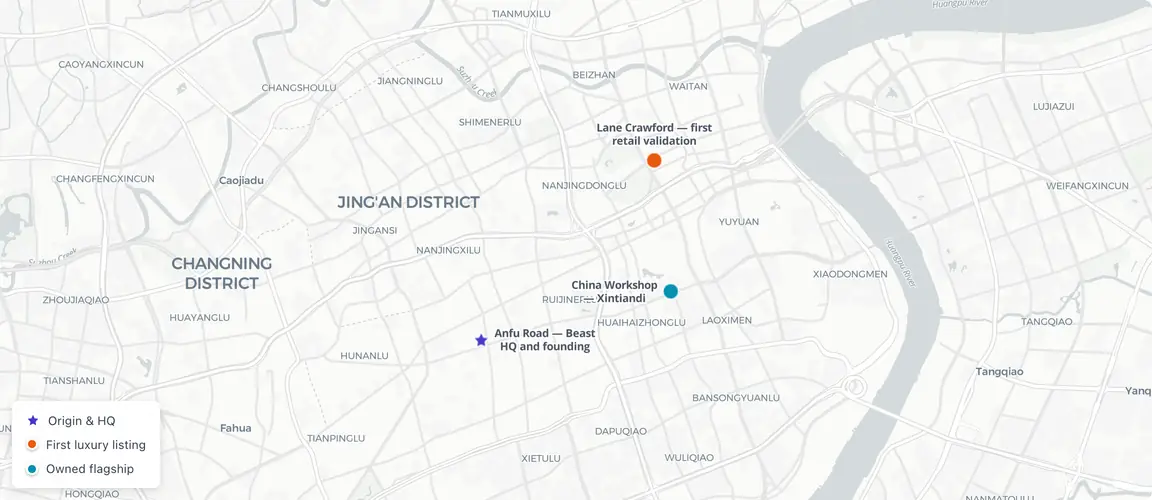

Beast's Story-Ordering Geography: Shanghai's Premium Corridor

The model that made price comparison impossible

The florist who refused to show you the flowers

On 29 November 2011, Amber Xiang opened a Weibo account and posted something the Chinese flower market had no framework for: a request. Tell me your story, she wrote. Tell me who you are buying for, what happened between you, what feeling you cannot say in words — and she would compose an arrangement around it.

There was no catalogue. No price list. No precedent.

Xiang had spent years as marketing director at Dragon TV (东方卫视), producing talent shows and building audience loyalty. She understood something that China’s flower vendors — still operating, as she later put it, at “the stage of selling vegetables” — had not yet grasped: that Chinese consumers at a certain income level were not buying a product. They were buying a story about who they were, who they loved, and what they believed beauty could mean. The flower was merely the vehicle. The story was the margin.

Within six months, 100,000 people were following a florist who had never shown them a single arrangement. By year’s end, Beast (野兽派, “Fauvism”) had 180,000 followers and had been named one of Weibo’s Top 10 Most Popular Users of 2012. The story-ordering model — 故事订花, “ordering flowers by story” — had been validated at scale before a single physical store opened.

What Xiang had discovered was not a marketing tactic. It was a business architecture. And it would take thirteen years, two existential crises, and RMB 418 million in annual fragrance sales to fully reveal what it could do.

What story-ordering actually is

We are not selling flowers, but stories.

The mechanism is precise, and understanding it is the insight.

Conventional premium brands charge more for the same physical good by attaching prestige signifiers — heritage, scarcity, endorsement, cultural positioning — that are generic and transferable. A Chanel perfume commands a premium because Chanel is Chanel: an institutional story owned by the brand and applied uniformly to every bottle. The consumer buys into the brand’s story.

Story-ordering inverts this. The premium does not come from the brand’s story applied to the product. It comes from the customer’s story built into the product. Each bouquet Xiang composed was, in effect, a unique object — a specific arrangement tied to a specific human narrative that no one else’s purchase could replicate. The story was not decorative; it was structural. It was why the product existed in its particular form, and why no commodity competitor could manufacture an equivalent.

This creates a pricing structure that is philosophically different from standard premiumisation. A competitor can undercut a heritage premium by offering similar provenance at a lower price. A competitor cannot undercut a story premium because the story is not transferable. The customer’s narrative — the apology, the late-night comfort, the first anniversary, the grief that has no name — is the irreplaceable component. The bouquet is custom by construction.

Xiang articulated the thesis in a 2022 interview: “We are not selling flowers, but stories.” The line is casual, but the architecture it describes is structural. It explains why Beast could charge what it charged, why Lane Crawford admitted a Chinese start-up to its luxury floor in 2013, and — most importantly — why the same logic migrated intact when Beast moved from flowers to fragrance.

The platform that made it possible

Story-ordering required a specific infrastructure: a medium where a brand could engage in one-to-one narrative exchange at scale. In 2011, that medium was Weibo.

The platform’s architecture in its early years was genuinely different from what followed. Weibo operated as an open social graph — content was public, discovery was algorithmic, and a single compelling post could reach millions of strangers. A brand that could build on Weibo’s open reach had an audience-development capability that no physical store could replicate. Beast was Weibo-native before that phrase described a category.

The critical point is timing. WeChat — the platform that would migrate Chinese social commerce to private channels — had launched in January 2011 and would not dominate until 2013 and beyond. The window in which a brand could discover 100,000 followers in six months through open-graph content was narrow. Xiang entered that window in November 2011 and spent the next two years converting open-graph reach into a brand with genuine luxury credentials.

The proof point arrived on 10 October 2013, when The BEAST House opened at Lane Crawford Shanghai. Lane Crawford’s buyers are editors. They assess brands not on revenue or distribution metrics, but on whether the story carries enough cultural authority to occupy the same floor as international luxury. The decision to grant Beast dedicated space was, in effect, the most credible external validation the story-ordering model had received: a purchasing judgment by professionals whose job is to decide what stories are worth premium proximity.

When the story migrates to fragrance

The fragrance pivot began before COVID. But the pandemic gave it a name.

In early 2020, lockdowns sealed Beast’s warehouse and emptied its boutiques. Perishable floristry inventory had no buyers and no path to market. The category on which the brand had been built — story-ordered fresh flowers — was structurally immune to the crisis. The brand was not.

What Xiang did next was not a category pivot. It was a proof of architecture. If the story-ordering model was real — if consumers genuinely paid for the narrative around a product rather than the product itself — then the same model should transfer to any category whose products could carry names and emotional frames. Fragrance was the obvious vehicle: a perfume is, almost by definition, a story you tell with your body, invisible until someone asks about it.

Golden Teardrop (金色眼泪) launched in December 2020, named for the resin that heals a wounded tree. The naming logic was identical to story-ordering: attach a precise emotional narrative to a sensory object, and let the narrative justify the price. The quarantine anxiety of 2020 — the grief of a locked country — had a product designed around it, not to escape it but to acknowledge it.

The confirmation of transfer came on 29 November 2021 — Beast’s tenth anniversary. The Unrequited Love (单恋) fragrance launched and generated RMB 10 million in sales in its first hour. The story-ordering model, which had needed six months to accumulate 100,000 Weibo followers, now needed sixty minutes to produce a revenue figure that the floristry business had taken years to approach. The model had not merely transferred. It had accelerated.

By 2024, Mirror Insight data cited by Jiemian confirmed Beast’s fragrance sales at RMB 418 million on Taobao and Tmall — the only domestic Chinese brand above approximately 3.5% category share. International luxury fragrance houses — Chanel, Dior, Jo Malone, Diptyque — held the category’s upper tier. Beast held the domestic layer below them, alone, on the strength of an architecture that those maisons could not easily replicate in China: a story-ordering model tuned specifically to Chinese emotional registers, Chinese cultural references, and Chinese consumers who did not experience luxury through a Western-filtered lens.

The stress test that clarified the model

In September 2022, investigative reporting revealed that Beast’s Osmanthus Oolong perfume — retailing at approximately RMB 420 per 30ml — was produced at the same contract factory (湖州御梵化妆品科技有限公司) as a Miniso fragrance retailing at RMB 29.9. The price gap was roughly fourteen to one. The hashtag “#Beast and Miniso share the same factory#” accumulated more than 360 million views on Weibo.

The scandal is worth examining as a structural event rather than a reputational one, because it clarifies something important about how the story-ordering model actually works — and where its vulnerability lies.

The charge was not about product safety or mislabelling. It was about whether the story justified the price when the physical basis of the product was demonstrably shared with a brand at one-fourteenth the price point. This is the question that every premium brand built on narrative rather than proprietary manufacturing must eventually answer.

The answer, which Beast’s subsequent performance provided, is more nuanced than either the scandal’s critics or the brand’s defenders acknowledged. OEM manufacturing — producing goods at contract factories that serve multiple clients — is standard practice across the global fragrance and lifestyle industry. LVMH subsidiaries, independent perfumers, and mass-market retailers all draw from overlapping manufacturing ecosystems. The Beast premium was not allocated to the factory floor. It was allocated to the design, curation, and narrative construction that surrounded the factory floor. A fragrance is approximately eighty percent raw materials and twenty percent editorial decision: what to name it, how to frame it, which emotional register it occupies, whose cultural reference system it speaks to. The fourteen-to-one price gap was not paying for a different factory. It was paying for the naming of grief.

Whether Chinese consumers would continue to pay that price after the manufacturing reality was public was the genuine question. By 2024, the answer was measurable: RMB 418 million in fragrance sales. The story model had survived its hardest factual test, though not unscathed — store count contracted from 47 to 41 in the same period. The market’s verdict was conditional: the story was worth the premium, but only if the story continued to evolve. A story that could be exposed was a story that needed a better answer than denial.

An architecture, not a one-off tactic

Story-ordering was not a tactic unique to Xiang. It is an architectural decision — a choice about where in the value chain a premium is installed — visible in how Beast’s model was structured from the outset.

The conventional path to premium runs through product authenticity: rare ingredients, proprietary technique, heritage certification, geographic indication. These are durable when genuine — a Yunnan pu’er from a registered old-tree grove, a Jingdezhen porcelain from a documented imperial kiln lineage — but they are slow to build and require the product to carry its own credential. A 300-year heritage is not something most artisan-lifestyle brands in China possess.

Story-ordering is structured differently: the premium is installed not in the product’s physical origin but in the narrative layer that surrounds it. Three elements make the architecture work in Beast’s case. First, an editorial instinct at the founding — Xiang thought in terms of narrative, frame, and audience, not just product specification. Second, a platform or channel enabling one-to-one emotional exchange at the volume required to make it a business. Third, the customer’s story becoming part of the product’s identity, not merely decorating it.

The third element is the structural inversion. Most luxury brands are built on the founder’s story applied to customers (this is who we are; by buying this, you share our identity). Story-ordering reverses that: the customer’s story is applied to the product (tell me who you are; I will build this around you). The reversal looks like it surrenders the brand’s narrative control. In practice, it does the opposite: a product built around a customer’s story is, by construction, worth more to that customer than a generic luxury alternative — not because the brand is stronger, but because the customer’s own investment in the narrative makes substitution psychologically difficult.

Beast built this architecture at the moment when Weibo gave a single compelling voice access to millions of strangers simultaneously. The platform conditions that made that speed possible closed after 2013; no Chinese social media environment in 2026 replicates the open-graph discovery dynamics of Weibo in 2011–2013. The model’s underlying logic, though, did not depend on that specific platform — it depended on a question asked of the customer instead of a product shown to them.

Xiang’s read — that Chinese consumers at a premium income level were aesthetically underfed and emotionally under-served by a flower market still operating at the vegetable-selling stage — was specific to China in 2011. What followed from it — that a brand built on the customer’s story is structurally harder to compete with than a brand built on the founder’s story — describes a mechanism, not a circumstance bound to China, to 2011, or to flowers.

The mechanism is visible applied to a different artisan-lifestyle category: Chinese tea. The conventional premium path there is geographic — Pu’er from a registered ancient grove in Yunnan, Longjing from a certified West Lake plot, Tieguanyin from a named Anxi village. Each credential is real, but each requires the product to carry its own provenance, and each is ultimately bounded by geography: there are only so many ancient Yunnan groves, and the premium they command is capped by supply constraints that keep the conversation anchored to scarcity rather than story.

A story-ordering architecture applied to tea would look structurally different: compositions built around a specific emotional occasion — the first cup after a father’s funeral, the last cup before a move overseas, a shared ritual between two people who rarely find words for each other — sold through a narrative exchange that makes each tin, in some sense, a commissioned object. The geographic credential might still be present, but it would not be carrying the structural weight. The story would.

The fragrance category in China already shows this bifurcation in practice: on one side, international luxury maisons applying institutional stories generically; on the other, domestic brands whose story-ordering logic produces goods that French heritage does not replicate. Beast holds the domestic layer of Taobao and Tmall with RMB 418M in annual sales. To Summer (观夏), founded in 2019 around Chinese botanical ingredients and seasonal scent narratives, grew on a comparable architecture — the emotional register of a Beijing hutong autumn, not the prestige of Grasse. Neither brand’s output has been replicated by a maison whose emotional vocabulary developed for a different market.

The price ceiling Beast installed was not a product premium. It was a story premium — the outcome of an architecture that produced RMB 418 million in annual fragrance sales from a Weibo account that refused to show anyone a price list, scaled and stress-tested across thirteen years.