Skip to main content

Skip to main content

Serbia: the brands that sanctions couldn't reach

Serbia has more than 1,100 registered distilleries. Most of the founders who built them during the post-2000 liberalisation wave are now in their fifties and sixties. No investment database has mapped what they built. No PE firm is watching. And the EU accession process — which will reshape trade terms for every one of them — is already underway.

Five sectors, one generation: Serbia's succession clusters

The post-Milošević generation, 2000–2026

Serbia has more than 1,100 registered distilleries. This is not a heritage statistic from an era of mass production — it is a present-day count of private, primarily founder-owned operations, almost all of them built after the year 2000. Most of the founders who built them are now in their fifties and sixties. Not one of these distilleries appears in PitchBook. Not one has been assessed in any institutional investor database. And the EU accession process — which will reshape the trade terms for every one of them — is already well underway.

This is the succession intelligence gap that defines Serbia in 2026. Not a market obscured by political opacity, like the DPRK, or by language barriers alone, like much of Francophone West Africa. Serbia is a documented market — EBRD annual reports, USAID agri-food programme records, PKS sector studies, and a dense Serbian-language business press together constitute one of the richer regional archives in the Balkans. The intelligence exists. What doesn’t exist is a synthesis of that intelligence for the international investor audience that would act on it.

Whitepaper No 1 documents the mechanics of why this gap is predictable: reform-era founding waves create tightly bounded cohorts that exit simultaneously, and the analytical infrastructure that would map these exits is systematically absent in markets that developed outside the Anglo-American venture capital ecosystem. Serbia fits the thesis precisely. The 1990s — a decade of UN sanctions, hyperinflation, and wartime dislocation — erased the prior cohort. Everything researchable was built after October 2000. And the founders who built it are all entering the succession window in the same narrow timeframe.

The compressed wave and what it produced

Serbia has never had a real succession culture. The founders simply assumed the children would take over, and the children assumed they would find their own way.

Serbia’s succession dynamic differs structurally from almost every other market Brandmine maps. In Russia, the founding wave spans roughly two decades — from Perestroika in 1988 through the late Putin-era consolidation of the 2000s. In China, the wave splits into two overlapping phases: Deng’s 1978 reforms and the post-Southern-Tour acceleration from 1992 onward. In India, the 1991 liberalisation cohort spans fifteen years of progressive opening.

Serbia has almost no analogous span. The UN sanctions of 1992–1995 and 1998–2001, combined with hyperinflation that peaked at a monthly rate of 313 million percent in January 1994 — the second-longest sustained hyperinflation in recorded history after Soviet Russia in the early 1920s — created what amounts to a research blackout. The formal consumer economy of the 1980s Yugoslav period was dismantled. What emerged in the 1990s was largely informal, parallel, and undocumentable. When Slobodan Milošević fell on October 5, 2000, and the DOS government began macroeconomic stabilisation, the founding window opened not gradually but abruptly. Founders who started businesses in the 2001–2010 window — at ages 25 to 42 — are now 50 to 68. The wave is not scattered across two decades. It is concentrated in a single compressed cohort.

The five sectors that matter most for succession intelligence reflect this compression directly.

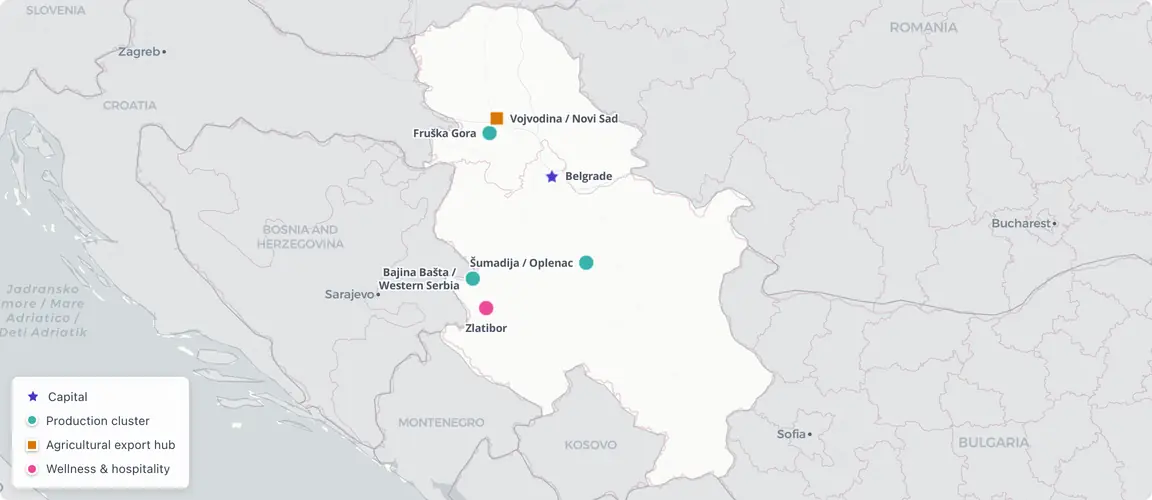

Wine: The registered winery count rose from 289 to approximately 500–529 over the decade ending in 2024, per Serbia’s Ministry of Agriculture — a doubling that almost entirely reflects post-2000 private founders entering viticulture. Clusters in Fruška Gora (150+ cellars near Sremski Karlovci), Šumadija and Oplenac (including Aleksandrović Winery, founded 2000, 250+ international awards, wines now in the Cité du Vin Bordeaux and Tokyo), and the under-developed Negotin region in eastern Serbia constitute a founder-owned wine industry that has been thoroughly mapped in the Serbian press and almost entirely absent from international investor reporting. Succession urgency: Imminent. Founders aged 52–68.

Rakija (fruit spirits): More than 1,100 registered distilleries nationwide. Of these, trade press estimates that approximately 110 — roughly 10 percent — operate at premium commercial scale, and the genuine institutional tier is 30 to 40 operations. The most prominent, Stara Sokolova (Bogdanović family, founded commercially in 1994 from Bajina Bašta in western Serbia), now exports to 30+ countries on four continents and carries its flagship 12 LUX product into premium spirits retail. The GI protection of Serbian Plum Brandy (šljivovica) — with Zarić’s Kraljica brand holding the only individual Protected Geographical Indication — has established a credentialed export category. The screening challenge is privatization: several marquee rakija names (including Podrum Palić, founded 1896, privatized 2002–04, bankrupted 2008–10, re-founded as a DOO in 2018) are revived state enterprises rather than genuine first-generation founding stories. Succession urgency: Imminent. Founders aged 50–70.

Specialty and organic food: Serbia is the world’s largest exporter of frozen raspberries and blackberries — approximately one-third of global trade at $527.7 million and 130,800 tonnes in 2021, per World Bank WITS data, ahead of Poland and Chile. This position was built by founder-owned SMEs, not by state enterprises or multinationals. The 6,300+ organic certificate holders operating on 21,000+ hectares represent a BIOFACH/SIPPO export pipeline that EBRD and USAID have extensively documented. Named founders — Marina Milović at Maja Promet honey, Darko Mandić at Happy Honey (the first Serbian food brand sold in Cost Plus World Market USA), the team at Master Food in Užice — have institutional relationships and documented succession questions. Succession urgency: Emerging, moving toward Imminent. Founders aged 50–68.

Natural beauty and personal care: A younger sector, with most artisan founder brands (Nina Natural, Slađana Obradović; Stella; Magaza; KOOZMETIK) founded after 2010. Founders skew younger — 45 to 62 — so near-term succession is less acute. Commercial fit is strong: clean-label, export-curious, Belgrade-centric brands that would interest European specialty retail buyers. The sector requires careful screening to exclude foreign brands distributed in Serbia (Alverde is German; Afrodita is Slovenian). Succession urgency: Emerging.

Honey and functional food: A distinct cluster that overlaps with specialty food but warrants separate treatment. Medino, headquartered in Krnjevac, accounts for an estimated 57 percent of Serbia’s national honey export — an extraordinary concentration for a founder-owned SME. EU certification and GI potential are both present. EBRD and USAID have documented this sector more thoroughly than almost any other in Serbian agri-food. Succession urgency: Imminent.

What the EU accession clock means

The succession urgency in Serbian consumer brands is not driven by founder age alone. It is shaped by the intersection of founder age with a second forcing function: EU accession and the transformation of trade terms it will produce.

Serbia has been an EU candidate since 2012. The accession process has moved slowly — EU candidate status does not confer membership, and negotiations have stalled repeatedly on Kosovo recognition and rule-of-law concerns. But the direction is clear, and its commercial effects are already being felt. GI certification for Serbian products has accelerated as brands pursue pre-accession EU market credentials. The BIOFACH pipeline for organic food exporters is an accession-adjacent infrastructure. The EBRD and USAID programme investment in Serbian agri-food SMEs anticipates the trade liberalisation that accession will eventually formalise.

For founder-owned brands, the accession trajectory is a double-edged forcing function. On one hand, it creates export-ready credentials and institutional visibility that make succession transactions more legible to Western buyers. On the other hand, it opens the market to scale competitors from EU member states that will intensify domestic competitive pressure. A founder who successfully navigated the 2001–2010 building phase and the 2008–2012 financial crisis and the 2020–2022 COVID disruption may face the most complex operating environment of their tenure precisely as they approach the succession question.

The succession infrastructure available to these founders is almost non-existent. The John Ward “30/13/3” study — roughly 30 percent of family firms survive into the second generation, 12 percent to the third, 3 percent to the fourth — describes the global baseline. Serbia layers several aggravating factors on top of that baseline: weak formal-governance traditions for privately held businesses, where succession planning is rarely formalised before a transaction becomes necessary; a diaspora with significant representation in Germany, Austria, and Switzerland (children raised abroad may not return); and a PE sector that, until Milenijum Tim’s 2022 entry into wine, had not specifically targeted founder-owned consumer brands. The Milenijum Tim transaction is the only one that has produced a public record — every other family negotiation, every founder who sells quietly to a local distributor rather than a strategic buyer, remains undocumented in any international capital-markets database.

The structure of the gap

The intelligence gap that defines Serbia is not a documentation gap in the conventional sense. The Serbian business press — Biznis.rs, Ekonomist, Blic Biznis, NIN, Politika — has covered founder-owned consumer brands in depth. EBRD and USAID programme reports have documented individual brands and sectors at a level of detail unavailable for most comparable markets. The corporate registry (Agencija za privredne registre) maintains public filings. The problem is structural: the documentation exists in Serbian (in both Cyrillic and Latin scripts — a digraphia that halves the effective coverage of single-script searches), in a country that dropped from international investor attention during the 1990s and never fully re-entered it after 2000.

An investor working only in English will find the EBRD reports and the international wine press coverage of Fruška Gora. An investor working only in Latin-script Serbian will find half the business press. An investor working in both scripts, in both Serbian and English, drawing on PKS sector reports, USAID agri-food assessments, Biznis.rs company coverage, and distillery/winery association records, will find a founder-owned brand landscape of 130 to 250 qualifying operations that has been systematically invisible to the global capital markets.

That is the Brandmine synthesis. The brands exist. The founders are aging. The EU accession clock is running. And the institutional intelligence needed to assess the succession readiness of these founders does not yet exist in any form accessible to international investors.

The Milenijum Tim signal

The 2022 acquisition of Vinarija Šapat by Milenijum Tim private equity is not merely an interesting data point. It is a structural indicator that the succession wave Brandmine maps has begun to produce institutional transactions.

Vinarija Šapat was not the most prominent Serbian winery. It was not the brand most visible in international wine press. It was a mid-tier Fruška Gora operation with a documented founder, a regional reputation, and a succession question that made it actionable. The PE firm found it and moved. The 40 to 60 similarly positioned founder-owned Serbian wine operations — and the comparable set in rakija, organic food, and honey — remain undocumented by any institutional investor database, in a Serbian-language business press that has covered them for two decades.

That is the loss this article is naming, with precision. Not a vague opportunity cost. A specific price paid by a specific founder for the specific absence of organised intelligence — intelligence that exists in the Serbian press, in both scripts, and has simply not been assembled.

The Serbian business press has covered them in two scripts. No one has assembled the map.