Skip to main content

Skip to main content

Senegal: The Founders the CFA Franc Made

A textile factory in Rufisque supplies Hermès, Fendi, and Christian Liaigre. Its founder built over three decades without venture capital, without a succession plan, and without appearing in a single institutional investment database. Senegal has roughly a hundred brands like this.

Senegal's brand geography in 2026

The CFA franc generation, 1985–2023

A factory in Rufisque, twelve kilometres east of Dakar’s financial district, supplies textiles to Hermès, Fendi, and interior designer Christian Liaigre. The founder who built it, Aïssa Dione, has been weaving bazin riche and raw cotton with a team of a hundred Senegalese artisans since 1992 — reversing, one loom at a time, a collapse that had destroyed 70,000 textile jobs in the three decades before she started. She has never raised institutional capital, never appeared in PitchBook, and never been profiled in the investment intelligence reports that asset managers in London, Dubai, or Hong Kong use to scout West African opportunities. The factory exists. The intelligence does not.

This is not unusual in Senegal. Across five consumer sectors — fashion and textiles, food processing, agro-export, beverages, and natural beauty — there are an estimated 95–145 founder-owned brands at commercial scale in West Africa’s most stable democracy. Their founders, most of them built during the post-1994 liberalisation wave, are entering the succession window simultaneously. The institutional infrastructure to find them, assess them, or support their transitions barely exists.

The generation the CFA franc made

SMEs represent 99.8% of Senegal's economic fabric, generate 80% of employment, and contribute 36% of GDP. Yet barely 9% of bank credit reaches them.

Every country’s founder cohort has a founding moment — a reform wave, a crisis, a market opening that concentrates new business formation in a compressed period. In Senegal, that moment arrived on the morning of January 12, 1994.

The CFA franc lost half its value overnight. The peg shifted from 50 to 100 CFA per French franc in a single announcement coordinated with France and the IMF. For Senegalese businesses that had built their supply chains around imported inputs — French chocolates, European fabrics, processed foods from the Métropole — the devaluation was a forced exit. Many did not survive the week. For the founders who had been quietly building with local materials, the same shock was an unplanned acceleration: their goods were suddenly 50% cheaper relative to imports, their local markets were suddenly uncontested, and their years of patient craft-building had become a structural advantage.

Senegal had already been through a decade of IMF-mandated Structural Adjustment Programs between 1985 and 1993. State monopolies in groundnuts and agricultural trade had been dismantled. Import barriers had eroded. The 1994 devaluation compressed what remained of the adjustment into a single morning and handed a permanent premium to local production. The companies that emerged from those years — and the new companies that formed in the decade following — constitute Senegal’s current founder cohort.

The wave shape is compressed in a way that distinguishes it from larger economies. China’s founding wave spans 1978 to 2001. India’s liberalisation extended across fifteen years. In Senegal, the decisive moment was a single date, and the founding surge it triggered lasted roughly a decade — from the pre-devaluation survivors of 1985–1993 to the post-devaluation processors of 1994–2003. Today, those founders are between 55 and 78 years old, and they are entering the succession window at the same time.

This compression has a consequence that is not widely understood. When an economy’s founding wave is distributed across two or three decades, as it was in India or Russia, succession events are staggered. Some companies transition early, creating precedents and institutional frameworks that later transitions can follow. In Senegal, the wave is so compressed that the succession pressure is arriving almost simultaneously across sectors — fashion, food processing, agro-export, beverages, and cosmetics — with no precedent, no advisory infrastructure, and no institutional memory of how a founder-owned Senegalese brand is supposed to transfer.

The fashion cohort makes the urgency vivid. Diouma Dieng Diakhaté — who founded Shalimar Couture in 1981, who has dressed West African heads of state for four decades — is 78. Oumou Sy opened her first atelier at the age of 13 and has been at the centre of Dakar’s fashion ecosystem for sixty years; she is 73–74. Aïssa Dione, who built the only Senegalese-owned high-end textile mill, is 73–74. Collé Sow Ardo, whose brand has been synonymous with Dakar fashion since 1983, is approximately 67. These four women have built institutions. None has a documented succession plan.

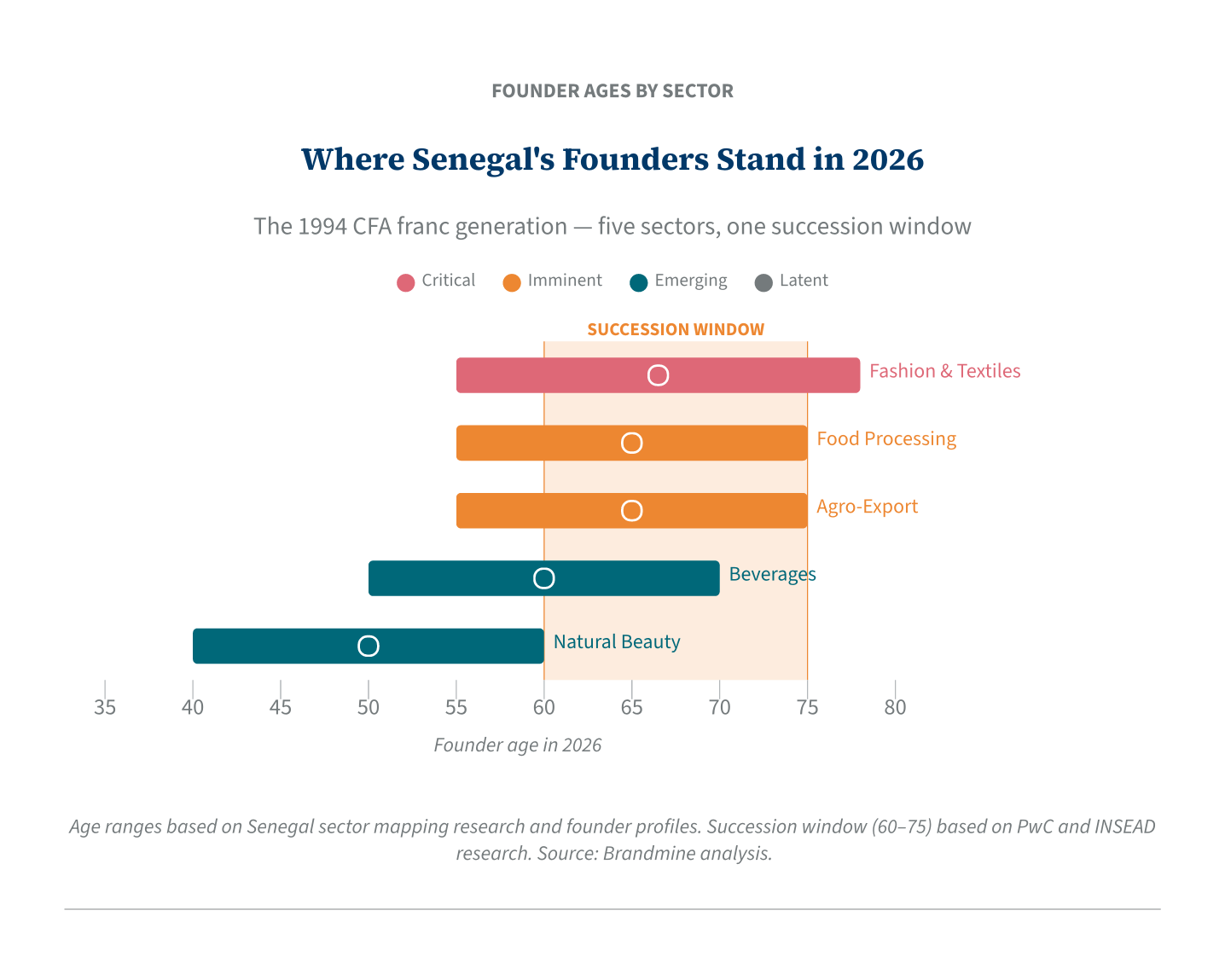

Five sectors approaching the window simultaneously

Fashion and textiles is the most urgent cluster, succession-readiness at the critical threshold for any West African market. Dakar alone has approximately 61,000 registered tailor workshops — a density that reflects a century of craft tradition and a generation of professional fashion-building that no institutional database has attempted to map. Among the scaled, formal brands, the four-founder cohort above represents an acute concentration of institutional knowledge and brand equity with no clear transfer mechanism. The Faye/Sonko government’s “consommer local” doctrine — which includes a proposed ban on second-hand clothing imports and the July 2024 relaunch of a state-supported Kaolack textile factory — has created a structural tailwind precisely when the cohort that built the sector is running out of time.

Food processing and specialty foods is the largest cluster, estimated at 25–45 founder-owned brands at commercial scale. The post-devaluation processing surge created an entire ecosystem of bouillon cube manufacturers, millet and fonio processors, specialty food companies, and catering operators who built import-substitution businesses between 1994 and 2005. The evidence that this ecosystem already attracts institutional attention is unambiguous: the July 2023 announcement of Al Mada’s majority stake acquisition in Patisen — via a Teralys vehicle — is West Africa’s largest recent FMCG succession event. Youssef Omaïs, who built Patisen from a single plant to a $200 million FMCG conglomerate with 7,000 employees and 50+ food product brands across 40 countries, is approximately 71. The acquisition proves that institutional buyers will pay meaningful prices for Senegalese food processing at scale. The intelligence on who the other forty-plus founders in this sector are does not exist.

Agro-export chains — an estimated 15–25 founder-owned exporters in mango, cashew, sesame, groundnut, and baobab processing — represent a type that no African investment database has systematically catalogued. The post-1994 export-substitution thesis maps directly: founders who pivoted from domestic sales to export certification created businesses that now supply European and North American retail chains, often under EU-certified organic or fair-trade standards. Vision Plus Afrique (Hamady Sow, baobab processing from Tambacounda, founded 2009), Acasen (cashew and peanut exports, founded 1992), and Délices Casamançaises (Mariama Dia, Casamance mango and palm oil) represent this archetype. Founder age bands cluster at 55–75. An important disambiguation applies: several agro-export businesses in this sector have Lebanese-Senegalese founding structures that require ownership verification before the investable pool can be sized.

Beverages (non-alcoholic) — an estimated 15–25 brands producing hibiscus (bissap), baobab (bouye), ginger, and tamarind drinks — sits at the intersection of three structural advantages: Senegal’s 95% Muslim consumer base (halal compliance is not a certification story, it is a baseline product characteristic), its diaspora export channel to France and the United States, and a global functional beverages market that is only beginning to discover West African botanical ingredients. French supermarket chains carry several Senegalese beverage brands — Fruitales among them — that have no institutional coverage in any investment database. Founders in this sector are generally 50–70, with emerging succession pressure.

Natural beauty and cosmetics is the largest estimated future market — approximately FCFA 1,300 billion by 2025 according to La Revue de Dakar — and carries the highest women-founder density of any Senegalese consumer sector. Bioessence Laboratories (Mame Khary Diène, founded 2005 after seven years at Capgemini France, winner of the 2008 Cartier Women’s Initiative Award), Afro & Nature (Ramatoulaye and Thiané Sarr, 2015, approaching nine-figure annual CFA revenue with four locations), and Sky Cosmetics International (Katim Touré, 2009, from street seller to parfumerie manufacturer) represent three distinct archetypes: the diaspora-return formulator, the local retail chain builder, and the artisanal-to-industrial arc. A critical caveat applies to succession timing: most cosmetics founders cluster at 40–55, below the acute succession floor, though the 2005–2010 diaspora-return cohort is approaching the window. Export reach to France and the United States creates a direct line between Senegalese founder intelligence and the European institutional audiences who can act on it.

Two ownership questions that keep capital out

What makes Senegal structurally harder to research — and therefore more valuable as an intelligence target — is the compounding effect of two disambiguation requirements that no investment database has resolved.

The first is the Lebanese-Senegalese family trust question. Several of Senegal’s largest food and agro-export brands were founded by Lebanese-origin families who arrived in Senegal generations ago and embedded deeply in the national economy. Patisen (Omaïs family), Zena Exotic Fruits (Filfili family), Kirene mineral water (Fares brothers), and Advens agricultural business (Jaber family) all require controlling-founder verification under family trust structures before they can be assessed as founder-owned targets. The distinction matters: a Lebanese-Senegalese founder who built a business from scratch and retains operational control is a Brandmine target. A family-office vehicle in which controlling interest is distributed across trusts and branches is not. The database-level answer is always ambiguous; the NDD answer requires direct research.

The second is the Mouride Brotherhood affiliation question. Senegal’s Mouride Brotherhood — one of West Africa’s most economically powerful Islamic networks — has channelled significant capital into consumer brands through marabout-affiliated structures. The Mboup family’s CCBM Group (Baralait dairy, Soklin, Santex food brands) and Serigne Cheikh Amar’s TSE conglomerate require the same disambiguation: does individual equity sit with a founder who built the brand, or is control distributed through a religious financial network? Baralait dairy is the cleanest consumer-brand entry point — a Senegalese-founded dairy with documented NDD material. Most Mouride-affiliated businesses require case-by-case verification.

These are not dealbreakers. They are the reason no PE firm has yet mapped this ecosystem systematically.

What the second buyer won’t find

Al Mada found Patisen in July 2023 and paid for it. The acquisition is the clearest documented signal that West African institutional buyers are already entering Senegalese FMCG, and that the 1994 devaluation cohort is ready to transact.

What Al Mada found was a brand with press coverage in Jeune Afrique, Financial Afrik, and Billionaires Africa — a founder who had given recorded interviews, whose company had audited financials through its Proparco relationship, and whose succession intention was legible from a distance. What Al Mada did not find — because the documentation does not exist — is the intelligence on the forty-plus food processing founders who survived the same devaluation, built in the same press-inaccessible environment, and are entering the same succession window without Omaïs’s institutional relationships.

The IFC’s record $615 million investment in Senegal in FY2024 confirms the institutional conviction. FONSIS’s WE! Fund invested FCFA 750 million in two women-led agro-food businesses in 2024. Teranga Capital and I&P-sponsored structures are active across the Dakar investment ecosystem. The capital has arrived. The intelligence to direct it toward the 95–145 founder-owned brands that sector mapping has identified has not been assembled.

Aïssa Dione has been weaving fabric for Hermès from a factory in Rufisque for thirty years. The intelligence brief that would tell a European asset manager who she is, what she built, how she survived the 1994 crisis, and whether she is preparing to transfer the business does not yet exist. Diouma Dieng Diakhaté is 78 and has dressed West African first ladies for four decades. Oumou Sy opened her first atelier as a teenager and has been building for sixty years. Both are in the pages of French-language press that no institutional analyst based in London or Singapore reads.

The founder’s own account of how it was built, what it survived, and what it is worth exists nowhere in any database. That account — the Narrative Due Diligence that can only be assembled while the founder is still in the room — sits instead in thirty years of French-language press coverage, in industry association records, and in the memory of founders who have never been asked the right questions by someone who understood what they were looking at.