Skip to main content

Skip to main content

Saudi Perfumery: A Sector Outside UAE Headlines

Saudi Arabia is the world's largest Arabic perfumery market — SAR 7.8 billion in 2022 — yet the houses dominating global discourse are all from the UAE: Ajmal, Rasasi, Lattafa, Swiss Arabian. The four Saudi-owned houses that hold a third of the home market operate under inheritance arcs the databases never reached. October 2024 was the inflection.

Saudi perfumery's four-cluster economy

Four ways to inherit a house

In international fragrance markets, the names that define Arabic perfumery — Ajmal, Rasasi, Swiss Arabian, Lattafa — are all houses from the UAE. The world’s largest Arabic perfumery market is Saudi Arabia, where Saudi-owned houses hold roughly one-third of a SAR 7.8 billion (2022) sector projected to reach SAR 13.4 billion by 2027, according to Euromonitor filings made public in Al Majed for Oud’s October 2024 Tadawul prospectus. The other two-thirds is a fragmented tail of family-owned distillers, retail chains, and niche oud specialists who collectively do not appear in any global database.

The four Saudi houses that anchor the sector — Arabian Oud, Abdul Samad Al Qurashi, Deraah, and Al Majed for Oud — operate under three different inheritance arcs and across four different geographic specializations. On 7 October 2024 one of them did something none had done before. Al Majed filed audited financials. The institutional book closed 156.5 times oversubscribed.

From two Makkah lanes to a national chain wave

We hold eleven percent of the Saudi fragrance market.

The oldest names sit in the Hijaz. Al Kamal began distilling Taif rose in 1831, four generations before the founding of the Saudi state. Abdul Samad Al-Qurashi began trading oud and amber in Makkah in 1852, opening his first formal retail store in 1932 in a lane near Dar al-Arqam beside the Grand Mosque. Ibrahim Al-Qurashi opened a perfumery near the Holy Mosque in 1929. Al Rehab established its Jeddah factory in 1975. These are the merchant-perfumer dynasties built on pilgrim traffic — small inventories, oil-based formulations, intergenerational customer relationships.

Riyadh’s retail aristocracy was assembled later, in the six years between 1976 and 1982. Ali Al-Hadi founded Deraah in 1976. Ali bin Othman Al-Majed, who had begun wholesaling oud and saffron in 1956, formally incorporated Al Majed for Oud in 1982. The same year, Sheikh Abdul Aziz Al-Jasser opened the first Arabian Oud kiosk in Riyadh’s Alzal souk with $1,360 of friends-and-family capital. Within a generation Arabian Oud held 1,200 stores in 37 countries. Within two generations it filed for a Tadawul listing.

The pattern that links the two eras is the absence of external capital. None of the four anchor houses was funded by venture capital, private equity, or a sovereign vehicle. Each was built on retained earnings, family balance sheets, and — in Arabian Oud’s case — a SAR 5,100 (~$1,360) cheque from a relative.

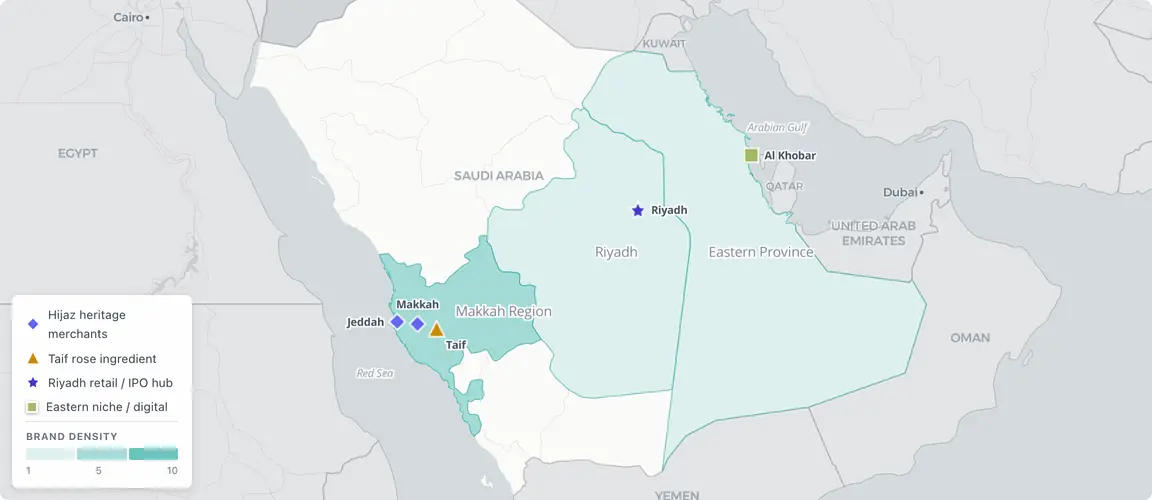

Three provinces, four roles

The sector concentrates in three Saudi provinces but plays four distinct roles. The Hijaz corridor (Makkah and Jeddah cities in Makkah Region) holds the heritage merchant dynasties: ASQ, IBRAQ, Surrati, Al Rehab, and the original Makkah workshop from which Al Haramain departed for the UAE in 1982. The Taif Rose Valley — also within Makkah Region administratively, but a thousand metres higher in the Hijaz mountains — supplies the ingredient layer. Al Kamal, Al Gadhi (documented since 1887), Al Qadi, Al Ghuraybi, Al Solhi and Bin Salman Farm operate 910 farms with 1.14 million bushes producing 550 million flowers per year. Bin Salman supplies Givenchy, Chanel, Hermès and Jimmy Choo at roughly $430 per 12-gram tolah of pure attar — 12,000 to 15,000 hand-picked roses per tolah, one of the most expensive natural luxury ingredients globally.

Riyadh is the national retail chain hub: Arabian Oud, Deraah, Al Majed, and Sokkat Alteeb all run their commercial operations from the capital, and only Riyadh has produced a perfumery brand structured to clear the CMA’s listing requirements. The Eastern Province (Dammam, Al Khobar, Hofuf) is the niche-and-digital fringe. Zohoor Alreef, founded in 1991 by brothers Waleed and Faisal AlKhaldi in an Al Khobar kitchen, runs the only Saudi mixology-fragrance chain. Sokkat Alteeb, founded in 1999 by Abdulaziz Al-Matroudi, transitioned its nine physical stores to an online niche-oud marketplace.

What the geography rewards is specialization. The Hijaz heritage houses sell to a daily-ritual customer base inherited from the pilgrim economy. The Taif rose families sell into global B2B luxury at margins the consumer-brand houses cannot reach — Bin Salman Farm has built a vertical model that pairs cultivation with on-site distillation, an agritourism café and a factory store, and the Chanel and Givenchy supply contracts that justify the elevation of its prices. The Riyadh chains sell scale and standardized formulations to a national retail customer; Arabian Oud’s 1,200-store operation is the only Saudi-owned consumer-brand business at that level. The Eastern Province is the experimental layer, where French-Arabian mixology (Zohoor Alreef) and online niche-oud commerce (Sokkat Alteeb) have prototyped formats the Tier-1 houses now study but have not yet adopted at scale.

What the databases miss

International fragrance research treats Arabic perfumery as a UAE category. IMARC, Mordor Intelligence, and Expert Market Research routinely list Ajmal, Rasasi, Lattafa, Nabeel and Anfasic Dokhoon alongside Arabian Oud and Al Majed as a single “Saudi competitive set.” This is a categorical error, not a research one. Ajmal is Indian-founded, headquartered in Dubai. Rasasi is UAE-based. Lattafa is UAE-based. Al Haramain — founded by Bangladeshi entrepreneur Kazi Abdul Haque in Makkah in 1970 — moved its headquarters to Ajman in 1982 and now operates a 550,000-square-foot factory there.

This is the WP2 thesis at work. Saudi-owned brands are hiding in plain sight in the world’s largest Arabic perfumery market, while the global discourse documents the UAE distributors who reach Western retail shelves more efficiently. The intelligence gap has structural causes. The most-quoted financial figures for Saudi houses are unreliable — RocketReach lists ASQ’s 2025 revenue at $51.2 million; LeadIQ lists the same firm at $750 million, a 15× spread. D&B’s Deraah revenue figure of $127 million is explicitly modelled rather than disclosed. Only Al Majed has audited figures, and only since 18 September 2024.

The second cause is language. Roughly 35% of the verifiable source material on these brands is Arabic-language only. The 2009 Al-Eqtisadiah interview in which Sheikh Ali Al-Hadi confirmed Deraah had completed 60% of CMA listing requirements — and then walked away — was never republished in English. The 4 January 2025 Argaam interview in which Omar Al-Jasser claimed 11% market share for Arabian Oud is in Arabic; the 9% figure that contradicts him appears in an English Arab News article based on a separate Euromonitor cut.

The third cause is the share of the market that sits in the fragmented tail. The four anchor houses hold roughly 33% of the sector. The other ~67% is hundreds of family-owned regional houses, Taif rose distillers, and specialist oud retailers with no English-language documentation. They are unreachable through conventional desk research.

Who survived the merger, the abandonment, the listing

Four founder decisions tell the sector’s story.

In 1988 Sheikh Abdul Samad Al-Qurashi died. His estate had already been distributed across his four sons as 21 separate single-store branches — Ihsan held six stores, Zuheir held three, Mohammed and Anas held five jointly, Anas held two more, and his sister Najla one. The structure was on a path to dissolving the brand. Within the same year, per their father’s deathbed instruction, the four brothers and Najla merged all 21 branches into a single corporate entity in Makkah. Ihsan took the chair, Zuheir vice-chair, Mohammed CEO, Anas vice-president. ASQ subsequently scaled from 21 stores to more than 500 over 35 years and held 9.4% market share by 2022.

In January 2009 Sheikh Ali bin Awad Al-Hadi told Al-Eqtisadiah that Deraah had completed more than 60% of its Capital Market Authority listing requirements. Sales had grown 33% through 2008 — through, not despite, the global financial crisis. He then withdrew from the IPO process and kept the firm private. The choice was strategic, not contingent: completing the listing would have priced Deraah into the post-Lehman trough and bound the family to public-market disclosure and quarterly-earnings cycles; staying private preserved both the balance sheet and the inheritance structure. Sixteen years later Deraah still operates 850 stores under family control, with succession running through Al-Hadi’s son Ebrahim. The 2009 decision is the canonical “could have IPO’d, chose family control” case in the Saudi private sector.

In 1982 Sheikh Abdul Aziz Al-Jasser entered Riyadh’s Alzal souk against the established Hijazi dynasties with $1,360 of friends-and-family capital and no commercial network. The sector at that moment was a heritage merchant business. Within a single generation Arabian Oud became the market leader. The leader’s share peaked at 12.7% in 2022 and has compressed to 9% by 2024 — a competitive-landscape signal as significant as the absolute share itself. The IPO mandate that Al-Jasser’s son Omar named to SNB Capital and Emirates NBD Capital in April 2024 has yet to produce a filed prospectus.

In 2023 the third generation of the Al Majed family — Bader and Mohammed Al-Majed — restructured the wholesale-to-retail operation their grandfather had begun in 1956 into a joint-stock company. On 7 October 2024 it listed on Tadawul. The institutional book closed 156.5 times oversubscribed at SAR 94, and shares jumped the +30% daily price-movement limit to SAR 122.20 on debut. The Al-Majeds retained 70% of the company. They became the first Saudi perfumery family to disclose audited financials: SR 767 million 2023 revenue at 66.6% gross margin, 286 stores, 132 brands, and 49 GCC stores beyond the Kingdom.

Four houses, four decisions, four different answers to the same structural question: institutionalize or stay private?

Oud as hygiene, hospitality, and prayer

In Saudi households, oud is not luxury. Bakhoor — perfumed agarwood chips burned on charcoal — scents homes before guests arrive and again before Friday prayers. Rose water is sprinkled on hands and clothing in greeting. Attar is dabbed multiple times daily, layered rather than chosen-and-applied. The Saudi consumer buys fragrance the way the European consumer buys coffee — frequently, ritually, with strong family-inherited preferences. This is why the sector is structurally built around oil-based, alcohol-free perfumes (attars and dhan al-oud) sold in small high-frequency units rather than the European EDP/EDT model.

Heritage houses have built brand power on this daily-ritual base. The economic shape of the sector follows from the ritual. Inventory turns faster than in Western fragrance, because a Saudi household replenishes attar and bakhoor every few weeks rather than every season; gross margins are higher on the small high-frequency unit; and brand loyalty is intergenerational, since fragrance preference is inherited through the household alongside the house’s other olfactory choices. Mohammed Al-Qurashi has said repeatedly that his father’s instruction was that “production and management must stay in Makkah.” That is a religious and cultural anchor, not a logistical one. Over three million Hajj pilgrims pass through Makkah and Jeddah each year, and the heritage houses sit on the corridors they walk. The Hijazi merchant identity is olfactory in a way that other Gulf merchant identities — pearling, dates, gold — are not.

The 156× and the 16 months

October 2024 was the inflection. April 2024 was the announcement. January 2025 was the confirmation. May 2026 is the gap.

In April 2024 Arabian Oud — the market leader, with roughly twice the store count of Al Majed and four times the share — formally mandated SNB Capital and Emirates NBD Capital to prepare a Tadawul listing. In October 2024 Al Majed listed first, with the institutional book 156.5 times oversubscribed and Bloomberg watching the +30% debut. In January 2025 Omar Al-Jasser told Argaam that Arabian Oud would list in 2025 and that the firm held 11% market share. Sixteen months later no prospectus has been filed.

The Vision 2030 framing makes the timing political as well as commercial. Sundeep Khanna, Partner Consumer and Retail at Arthur D. Little, told Arab News in May 2025 that “Saudi Arabia has identified fragrances — particularly oud — as a key non-oil export to support economic diversification.” The Saudi Export Development Authority lists fragrance among priority non-oil categories. The supply side carries its own clock. All Aquilaria species have been on CITES Appendix II since 2005; the wild population has dropped roughly 80% in a century. Every Saudi oud house depends on Vietnam, Laos, Cambodia and India wild-harvest supply chains that are now permit-bound on every shipment.

The sector is being asked to institutionalize and to globalize at the same time that its raw material is being constrained at the source. Disclosure and supply are the two capacities now separating the four houses from each other. Some have chosen routes that do not pass through Tadawul. IBRAQ’s 2024 rebrand and Neymar Jr. ambassadorship for Brazilian Tobacco is an attempt to acquire European and Latin American consumers through celebrity rather than capital structure. Al Majed has begun GCC franchise expansion — 49 stores beyond the Kingdom at YE2023, per its prospectus — building distribution that compounds whether or not its share-by-share IPO outperforms. The choice each Tier-1 house is making, consciously or by default, is between disclosure-led institutionalization and distribution-led institutionalization. Both are slower than UAE-style export volume.

The compression that compounds itself

The market leader compressed from 12.7% to 9% in two years while the sector grew toward SAR 13.4 billion. The arithmetic is one-directional. Every quarter without institutional capital, succession formalization, or global distribution moves share from the four named Saudi houses to the fragmenting tail — and to the UAE distributors who dominate the global Arabic perfumery conversation by default. Al Majed took seven months from prospectus to listing. Arabian Oud, twice its size, has taken twenty-three and produced no prospectus at all — a mandate renewed in press statements rather than filings, while the smaller house it outsold for decades sets the terms of what a Saudi perfumery IPO now looks like. The Taif rose families made their institutional choice generations ago, inside Chanel and Givenchy bottles, and the margins followed; Arabian Oud is discovering that the same choice, deferred long enough, gets made by someone else’s prospectus instead.