Skip to main content

Skip to main content

Philippines: The Archipelago of Invisible Brands

The Philippines has 7,641 islands, a food processing sector exceeding $25 billion in retail sales, and a generation of consumer-brand founders forged by the Asian Financial Crisis, three major volcanic eruptions, Typhoon Haiyan, and the world's longest COVID-19 lockdown -- all within a single career. Fewer than 30% of Philippine family businesses survive to the second generation. A constitutional 60/40 foreign ownership cap blocks majority foreign acquisitions, making succession intelligence not merely useful but necessary. The window is open.

Philippines' Founder-Owned Brand Geography

Transformation Arc

The Philippines has 7,641 islands, and its most valuable consumer brands are hiding on nearly all of them – in food processing plants in the volcanic ash belt of Pampanga, in furniture workshops along the export docks of Cebu, in the personal care laboratories of Mandaluyong, and in the QSR chains that line every provincial highway from Luzon to Mindanao. The founders who built these brands emerged from a specific historical moment – the post-EDSA economic opening of 1986 to 2000 – and are now entering the succession window simultaneously, without succession plans, without institutional buyers equipped to act, and protected by a constitutional foreign ownership cap that makes the intelligence gap not merely inconvenient but commercially decisive.

Whitepaper No 1 documents the synchronized transition wave unfolding across emerging markets: reform-era founders ageing out together, institutional investors unprepared. The Philippines is one of the wave’s sharpest expressions. An estimated 80% of Philippine businesses are family-owned. Only 30% survive to the second generation. The founders who built the country’s mid-market consumer brands – the $5 million to $100 million range invisible to Bloomberg, known to every Filipino consumer – are now 55 to 75 years old. And the Philippine Constitution’s 60/40 foreign ownership requirement means that any foreign institutional investor who wants access to these brands must find a local partner before the transition forces a distressed sale.

The intelligence to identify those brands, those founders, and those succession timelines does not exist in any database. It exists in three decades of Philippine business press – BusinessWorld, the Inquirer, PhilStar, Rappler, BusinessMirror – in the three volumes of Go Negosyo founder interviews, and in the archives of the Federation of Filipino-Chinese Chambers of Commerce. What does not exist is a synthesis. That synthesis is what follows.

The wave and its shape

Only 30% of Philippine family businesses survive to the second generation.

The Philippine succession wave was created by two reform events working in sequence. The first was political: the 1986 EDSA People Power Revolution that ended Ferdinand Marcos Sr.’s dictatorship and restored democracy under Corazon Aquino. The second was economic: the Ramos-era deregulation between 1992 and 1998 that liberalised banking, telecommunications, power, water, airlines, and retail – transforming the Philippines from a closed Marcos economy into one of Southeast Asia’s most dynamic consumer markets.

The founders who moved fastest in this window were overwhelmingly Chinese-Filipino (Tsinoy) families. The Tsinoy community – approximately 1.5% of the Philippine population but controlling an estimated 50 to 60% of the country’s private corporate wealth – had maintained commercial networks through the Marcos years, often operating below the radar of the nationalisation policies that targeted foreign businesses. When deregulation arrived, they had capital, supplier relationships, and commercial infrastructure that purely Filipino-origin entrepreneurs lacked. The result is a specific ownership pattern: many of the Philippines’ most successful mid-market consumer brands are Chinese-Filipino family businesses in their second or third generation, facing the internal succession pressures that arise when multiple heirs compete without governance structures.

Below this Tsinoy layer sits a different founder type: first-generation entrepreneurs who emerged from the OFW (overseas Filipino worker) remittance economy, from provincial manufacturing clusters, from the Marcos-era informal sector, or from the post-crisis reconstruction period after the 1997 Asian Financial Crisis. These founders are typically less wealthy, less connected to the institutional infrastructure, and more dependent on personal relationships and founder charisma to maintain their businesses. They are also more fragile succession candidates.

What makes the Philippine wave shape distinctive is the layering of crises on top of this founder cohort. The Asian Financial Crisis of 1997–1998 – the peso crashed from ₱26 to ₱55 per dollar – is the primary NDD anchor event. But it sits on top of the 1991 Mount Pinatubo eruption (which devastated the Pampanga food processing cluster), and beneath the 2013 Typhoon Haiyan catastrophe (which destroyed the Eastern Visayas supply chain) and the 2020–2022 COVID lockdowns (the world’s longest, running through multiple waves for nearly two years). A Philippine consumer brand founder with a thirty-year career has navigated a volcanic eruption, a currency crash, a super-typhoon, and a pandemic. The crisis documentation is cumulative – and it is concentrated in exactly the $5 million to $100 million revenue range that institutional investors have never been equipped to access.

Where the transition pressure is highest

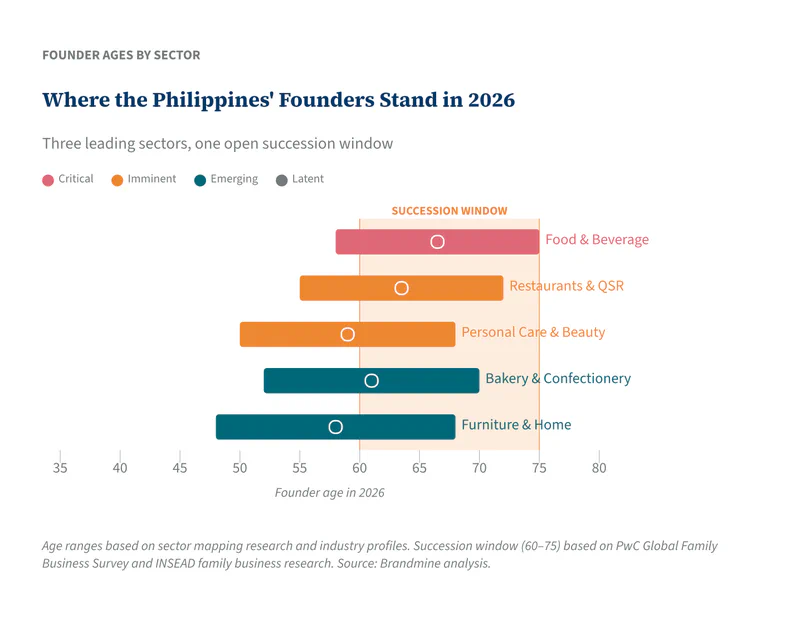

Brandmine’s sector mapping identified twelve candidate consumer sectors in the Philippines. Nine show meaningful founder-owned brand activity at commercial scale. Three stand at the front of the transition wave.

The sector with the richest crisis documentation

The Philippine food and beverage manufacturing sector – condiments, processed meats, packaged foods, beverages, and food ingredients – is the country’s most concentrated repository of succession-eligible founder-owned brands. An estimated 25 to 35 brands operate at commercial scale with founders in the succession window, representing a conservative floor estimate likely to be 5 to 10 times higher when fully researched.

The anchor stories are well-documented. Alfredo Yao, founder of Zest-O Corporation (born 1943), controls approximately 80% of the Philippine juice market and has diversified into RC Cola Philippines – at age 82, with succession details described by Forbes Asia as “extremely opaque despite three children.” King Sue Ham & Sausage, founded by Fujian immigrant Cu Un Kay in the 1930s, is a multi-generational Tsinoy family processing brand with near-universal consumer recognition and a public profile of near-zero. NutriAsia – controlling UFC, Datu Puti, Silver Swan, and Mang Tomas – represents the outcome of a succession event: Silver Swan, founded in the 1940s by the Sy Bun Suan family, failed internal succession and was acquired by NutriAsia in 2014. The brand name itself is phonetically derived from the founder’s name. Mekeni Food Corp, built from a backyard operation by Felix and Medicia Garcia in 1986, survived the Pinatubo eruption, rebuilt as the first ISO 22000-certified meat plant in Asia, and now exports to 23 countries – the fullest documented crisis arc in the sector.

The Tsinoy pattern is the defining structural feature: Chinese-Filipino family businesses in their second or third generation, with founding patriarchs who are 70 to 85 years old, managed by second-generation family members who may or may not want to carry the business forward. The FFCCCII (Federation of Filipino-Chinese Chambers of Commerce and Industry, with 170-plus member organisations) is the single most valuable access point for the “invisible middle” of this sector – brands that are known to every Filipino consumer but have never appeared in a business profile.

The sector with the clearest exit precedent

The Philippine restaurant and QSR chain sector – fast food, casual dining, and specialty restaurant chains – has the richest narrative documentation of any sector in Brandmine’s Southeast Asia coverage, anchored by the Jollibee story. Tony Tan Caktiong chose to fight McDonald’s entry in 1981 rather than sell his five-store chain, doubled down on Filipino flavours (Chickenjoy, sweet spaghetti, palabok), and built Jollibee into the country’s most powerful consumer brand with 10,304 stores across 17 countries. The Jollibee origin story is the most documented Philippine brand crisis narrative in existence – and Jollibee Foods Corporation has become the sector’s dominant strategic acquirer, creating a clear exit pathway for every founder-owned chain that follows.

The proof-of-concept transaction for that exit pathway is the Mang Inasal acquisition. Edgar Sia founded Mang Inasal in Iloilo City in 2003 with a grilled chicken concept targeting the mass market. Jollibee acquired 70% of the company in 2010 for ₱3 billion, and the remaining 30% in 2016 for ₱2 billion – a total of ₱5 billion for a concept that was seven years old at the first transaction. An estimated 20 to 35 founder-owned restaurant chains operate at commercial scale with founders in the succession window, many watching the Mang Inasal precedent and considering whether to build for acquisition or attempt independent succession.

Potato Corner, founded in 1992 by Jose Magsaysay Jr. and three partners as a flavoured fries cart in a Mandaluyong mall, now operates more than 1,100 stores in the Philippines and 200-plus overseas across 11 countries – one of the most successful Philippine franchise exports in the sector. Magsaysay remains active as President, a founder now in his late 50s with an international footprint that represents exactly the export-ready profile that Asian family office investors are seeking.

The sector with the proof-of-concept acquisition

The Philippine personal care and beauty sector has the clearest evidence that cross-border acquisition of Philippine consumer brands is possible, priced, and precedented. The Splash Corporation transaction – Rolando Hortaleza sold his personal care company (Maxi-Peel exfoliants, SkinWhite glutathione products, Extraderm skincare) to India’s Wipro Consumer Care in 2019 for approximately $80 million in revenue – established the sector’s benchmark. Hortaleza built Splash from a basement laboratory in Mandaluyong into the Philippines’ largest homegrown personal care company over three decades. The Wipro acquisition was the first significant cross-border consumer brand acquisition in Philippine personal care history, and it sent a signal through every founder-owned brand in the sector.

The sector’s founder cohort is split between two waves. The first wave (post-EDSA, 1986–2000) includes founders now aged 55 to 70, with Splash as the archetype. Dr. Cecilio Kwok Pedro, founder of Lamoiyan Corporation (Hapee Toothpaste), is approximately 73 years old and represents one of the few transparent successions in the market: his son Joel Pedro is now CEO, driving digital strategy with documented 50% annual online growth as of 2023. Pedro is simultaneously current president of the FFCCCII, giving him structural access to the Tsinoy network that no outside researcher can replicate.

The second wave is digital-native: brands built on Shopee, Lazada, and OFW reseller networks in the 2010s, targeting the glutathione/whitening category that is uniquely large in the Philippine market. Anna Meloto-Wilk’s Human Nature – natural personal care targeting the OFW consumer and social enterprise model – survived the COVID lockdowns with a documented pay-cuts-not-layoffs response and candid founder interviews that constitute some of the richest crisis documentation in the sector. Brilliant Skin Essentials (Glenda Victorio), a Go Negosyo awardee, built its distribution entirely through reseller armies reaching OFW communities globally – an archetype of the Philippine beauty brand that never appears in traditional retail databases but commands a market of 12 million overseas Filipinos.

The sectors still forming

Two additional sectors warrant monitoring. Bakery and confectionery (estimated 15 to 20 founder-owned brands, founders aged 50 to 70) contains Goldilocks, the country’s most recognised Filipino bakery chain – now 34% owned by SM Investments – alongside a network of regional brands and heritage bakeries that have never faced institutional attention. Furniture and home furnishings (estimated 15 to 25 brands, founders aged 48 to 68) anchors the Cebu export manufacturing cluster, where Filipino-made pieces reach Europe, North America, and Japan, and where founder-designed brands are beginning to separate themselves from pure contract manufacturing.

Why this wave breaks differently

The Philippine succession wave has a specific character that distinguishes it from every other market in Brandmine’s Global South coverage. The constitutional constraint changes everything.

Most succession wave analysis assumes that when a founder exits, institutional capital can enter through a majority stake, restructure governance, and either build or sell. In the Philippines, the Constitution’s Article XII limits foreign ownership to 40% in most sectors. A foreign private equity firm, family office, or strategic acquirer cannot buy majority control of a Philippine consumer brand without a Filipino partner holding at least 60%. This is not a regulatory risk – it is the structural condition. Every succession event in the Philippine mid-market resolves through one of three pathways: family inheritance (often contested, rarely planned), domestic strategic acquisition (JFC, SM Investments, Monde Nissin), or local partnership with a minority foreign stake. The fourth pathway – majority foreign acquisition – is constitutionally blocked.

The implication for intelligence is precise: the investor who identifies a Philippine founder-owned brand in the succession window, and who understands the specific succession dynamics, can structure a 40% stake with governance rights before the transition forces the brand into a distressed domestic sale. The investor who arrives after the transition, when the brand has already passed to the next generation or been acquired by JFC at a distressed price, has missed the window. The intelligence gap is not informational – it is temporal. The value is in identifying the brands before the wave breaks.

The cultural dimension compounds the structural one. Utang na loob – the Filipino concept of debt of gratitude, which creates obligations to family and community that outlast commercial logic – means that succession discussions are taboo, succession decisions are often driven by eldest-child primogeniture rather than management competence, and founders frequently prefer to die in office rather than acknowledge that the transition is inevitable. The Go Negosyo archive – three published volumes, 150 founder stories – is the richest available source of documented Philippine founder crisis narratives, but it does not contain a single honest discussion of succession planning. The founders who survived typhoons and currency crashes and volcanic eruptions are not, as a cohort, making plans to let go.

The window and who is already inside it

Two domestic strategic acquirers have understood this landscape for years. Jollibee Foods Corporation’s serial M&A programme – acquiring Mang Inasal, Red Ribbon, Chowking, Greenwich, and a series of international brands – is the most active buyer in the QSR sector. SM Investments, through its 34% stake in Goldilocks and its investment arm, is the most patient domestic capital in the bakery and consumer goods space. Monde Nissin, which went public in 2021 in what was then the largest IPO in Philippine history, has signalled appetite for consumer brand acquisitions in food processing.

The international buyers who have moved are limited in number and recent in arrival. Wipro Consumer Care’s 2019 Splash acquisition remains the reference transaction. The constitutional 60/40 constraint means that every international buyer is structurally a minority partner – which makes the quality of local intelligence about who owns what, who is planning to transition, and which brands are available at what valuation not merely useful but constitutionally necessary.

What disappears when a Philippine founder exits without a plan is not just a brand. It is the OFW distribution network built through thirty years of personal relationships with sari-sari store owners in the Middle East and Hong Kong. It is the supplier credit terms negotiated through the Asian Financial Crisis. It is the formulation knowledge that survived the Pinatubo ash fall. It is the local government relationships that kept a Pampanga food plant operating when the provincial roads were impassable. None of this transfers through an org chart. By the time these brands appear in any database that foreign investors monitor, the founder who carried this knowledge will have retired, sold at a distressed price, or simply handed the business to a child who may or may not want it.

The Philippines’ founder-owned brands have been hiding in a country with one of Southeast Asia’s most extensive English-language business press traditions, in sectors that the global consumer already knows and values, behind a constitutional barrier that makes local intelligence not a competitive advantage but a structural requirement. The intelligence to find them is being assembled. The window to act as a structured minority partner – before the wave breaks and the forced transitions begin – is open. The 60/40 rule does not close the window. It narrows it to those who understand what they are looking for.