Skip to main content

Skip to main content

Nepal: The First-Generation Reckoning

Nepal's consumer brand founders built their businesses between two catastrophes: a decade-long Maoist insurgency and a 7.8-magnitude earthquake. Now aged 55 to 75, they face succession simultaneously — no advisory infrastructure, no PE capital, and a generation of heirs who chose Gulf employment over inheriting what their parents built.

Kathmandu Valley hub and the Ilam tea corridor: Nepal's two-hub succession map

The unadvised generation, 1996–2024

Between 1996 and 2006, Nepal’s consumer brand founders built their businesses while navigating a Maoist insurgency. The peace agreement came in 2006. Nine years later, a 7.8-magnitude earthquake killed nearly 9,000 people and collapsed tourist arrivals overnight. The founders who survived both — and kept building — are now 55 to 75 years old. They are approaching succession simultaneously. And no one outside Nepal has been paying attention.

Nepal is what the synchronized succession thesis looks like when the founding window is compressed by war. Most emerging markets give their first-generation founders a decade of relative peace to build. Nepal gave its founders a decade of active insurgency — and then, once peace arrived, a 7.8-magnitude earthquake. The founders who held through that sequence are the most crisis-hardened consumer brand builders anywhere in South Asia. They are also, right now, at peak succession urgency.

The intelligence gap is almost total. No PE fund currently targets Nepal’s consumer brands. The country’s business press runs primarily in Nepali, with English-language coverage sparse and concentrated in Kathmandu. Individual brands rarely exceed $5 million in revenue — which places them below every institutional screening threshold. And 85 to 90 percent of Nepali businesses are family-owned, most by first-generation founders who have never thought about succession as a structured problem. What these founders built sits below every institutional screen, undocumented by anyone outside Nepal.

The compressed crisis wave

We're trying to build a Nepali brand that reflects the beauty, variety and depth of our country and culture.

Nepal’s succession wave does not follow the gradual demographic arc visible in larger emerging markets. It is a compression event — with an unusual cause.

Nepal’s founding window is narrower and more violent. The 1990 democratic revolution and the 1992 Industrial Policy deregulation opened private enterprise for the first time. Between 1990 and 1996, the first founder cohort established businesses across pashmina, tea, hospitality, carpets, and herbal wellness — sectors where Nepal had meaningful comparative advantage and which institutional capital had not yet noticed. Then, in February 1996, the Maoist People’s War began.

For a decade, consumer brand founders operated under insurgency conditions. Extortion demands — “donations” to the People’s Liberation Army — were routine across manufacturing, hospitality, and retail. Supply chains into rural production zones were disrupted by blockades. The ability to raise capital, expand operations, or plan more than a season ahead was structurally compromised. Founders who might have been building through their most productive decade were instead spending it on survival.

The Comprehensive Peace Agreement of 2006 ended the insurgency. For the survivor cohort, peace arrived at a specific biographical moment: founders who had started businesses in their late twenties or early thirties in 1990–1992 were now in their mid-to-late forties. They had ten years of insurgency-era operations, and they now had the first sustained opportunity to build without existential pressure.

Nine years later, the earthquake.

The 2015 Gorkha earthquake registered 7.8 on the Richter scale. It killed nearly 9,000 people, destroyed or damaged a third of the country’s infrastructure, and eliminated tourist arrivals for months. For hospitality founders in their fifties, the earthquake was an existential test — damage to physical assets, collapse of bookings, and the complex work of reconstruction while managing ongoing operations. For pashmina and carpet exporters, supply chain disruptions and reputational damage to Nepal as a sourcing country compounded the operational shock.

What makes this double-crisis unusual is that it happened to an entire cohort simultaneously, in a documented sequence, within a geographically concentrated country. The insurgency NDD material alone — founders who navigated People’s Liberation Army extortion demands — has never been systematically compiled.

The founders who built through both crises are now 55 to 75. The succession clock is running at full urgency.

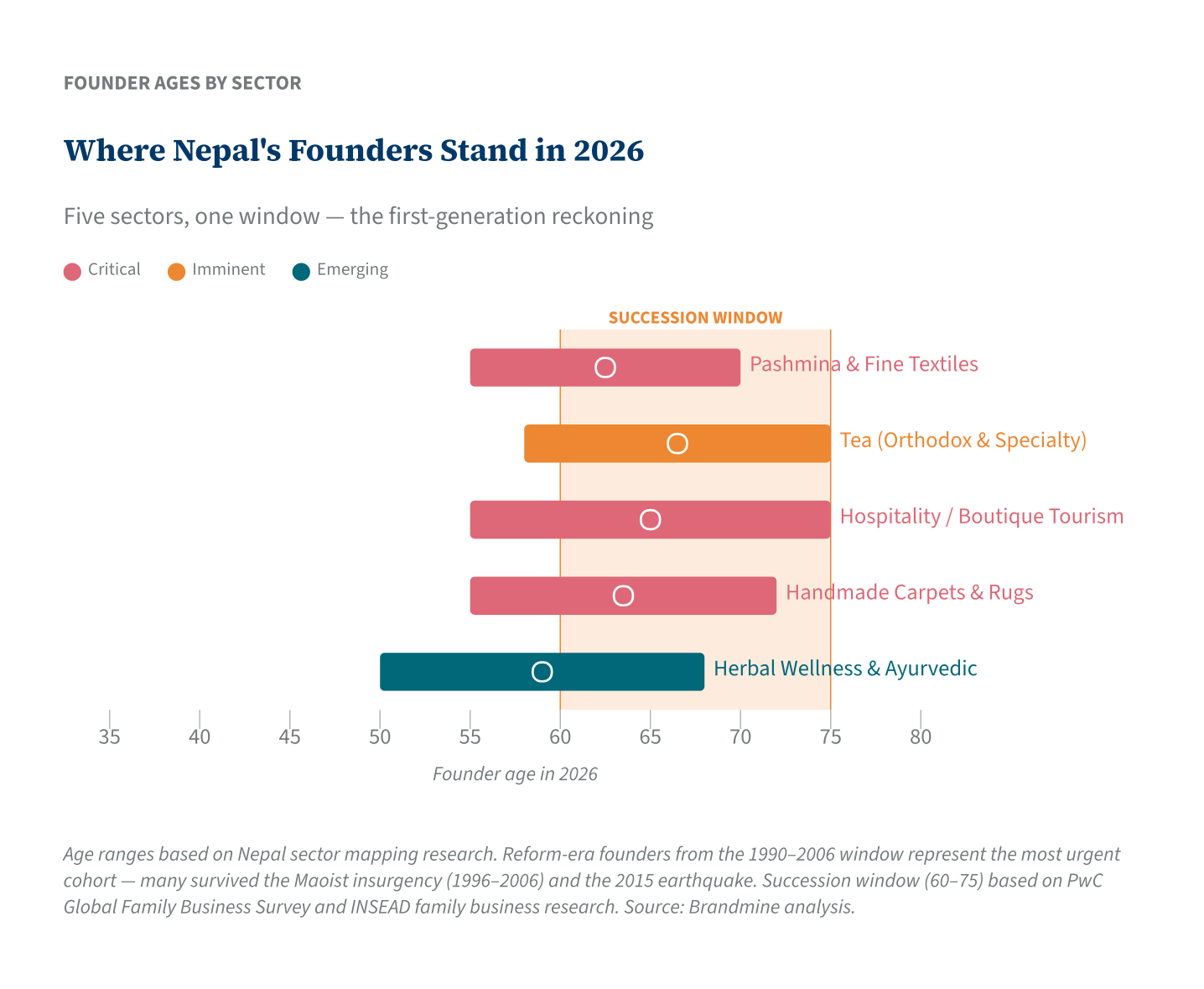

Pashmina, tea, hospitality, carpets, and herbal wellness

Sector mapping for this report identified twelve consumer sectors with founder-owned brand activity in Nepal. Five carry meaningful succession pressure — sectors where established founder-owned brands exist at commercial scale, founders are within or approaching the transition window, and no succession infrastructure has been built.

The sector that fell from $112 million and is approaching succession at its nadir

Nepal’s pashmina sector is the most acute convergence of commercial decline and succession pressure in any Brandmine coverage country. At peak in the late 1990s, pashmina exports exceeded $112 million annually. A combination of market saturation, Chinese competition, and mislabelling controversies collapsed that to under $20 million — a decline of more than 80 percent within a single founder lifetime.

The survivors of that collapse carry narratives of exceptional commercial resilience. An estimated 15–20 founder-owned operations remain at commercial scale, with founders typically aged 55–70 — succession urgency: critical. These are businesses that held through the export collapse, the insurgency, and the earthquake. They are not fragile. But the founders are approaching the transition window in a sector that has never recovered to its peak, where the brands that survive carry decades of export relationships that reside entirely in the founder’s personal networks.

The intelligence opportunity is specific: who survived, how, and what they built from the ruins of a $100-million export sector. That documentation does not exist anywhere outside Nepali trade press.

The sector growing at 27 percent annually — with founders who could exit at the moment of peak value

Nepal’s orthodox and specialty tea sector is the fastest-growing export story in South Asia. Tea exports reached $34 million in the most recent available year, growing at 27 percent annually — a trajectory that is already attracting attention from premium buyers in Germany, France, Canada, Japan, and the United States.

The sector has 12–18 founder-owned operations at commercial scale, with founders aged 58–75 — succession urgency: imminent. Several of the most prominent tea gardens were established in the 1990s or early 2000s, meaning their founders built through the insurgency years and are now approaching the succession window precisely as the sector achieves international recognition.

The structural risk is the timing mismatch. Founders who spent a decade navigating insurgency-era production constraints, who then built international distribution relationships through the 2010s, are now approaching exit at the moment when the brands they built have reached their highest historical value. The relationships that make these tea gardens export-competitive — buyer networks in Germany and Japan that took fifteen years to build — reside personally in each founder, with no documented mechanism for transfer.

The sector where one succession event has already happened — and the wave is just beginning

Nepal’s boutique hospitality and tourism sector carries the clearest succession signal of any Nepal sector. An estimated 20–30 founder-owned operations exist at commercial scale, with founders aged 55–75 — succession urgency: critical.

Several of these founders built the experiential tourism infrastructure that Nepal’s international reputation depends on: trekking lodges above 3,000 metres, heritage hospitality properties that survived earthquake damage, boutique hotels that built their reputations through two decades of international press coverage. The hospitality sector was hit by three successive crises — insurgency, earthquake, pandemic — and the founders who held through all three are the most stress-tested in the category. They also carry the most acute succession pressure.

The Dwarika’s Hotel succession in 2024 is the clearest signal that the wave has already begun. More on that below.

The sector whose founders built through collapse and are now approaching exit with no buyer infrastructure

Nepal’s handmade carpet and rug sector followed the same trajectory as pashmina: a peak export period in the 1990s at over $140 million annually, followed by significant decline as Chinese machine-made alternatives displaced the premium end of the market. The artisan segment that survived is distinguished by export quality and provenance documentation — exactly the attributes that command premium pricing in European and North American markets.

An estimated 12–18 founder-owned operations remain at commercial scale, with founders aged 55–72 — succession urgency: critical. These are businesses that survived the same export collapse as pashmina, often in parallel with the insurgency period, and rebuilt their markets around provenance, artisan authenticity, and fair-trade certification.

The sector that is growing but whose founders have structural dependence on a single market

Nepal’s herbal wellness and Ayurvedic products sector is the youngest of the five, and the least commercially mature. An estimated 8–15 founder-owned brands operate at or near commercial scale, with founders aged 50–68 — succession urgency: emerging. The sector’s export growth is real but structurally concentrated: an estimated 67–81 percent of herbal export revenue runs through India as primary buyer, creating a single-market dependency that limits pricing power and makes international diversification both necessary and difficult.

The double-crisis signature

Nepal’s succession crisis shares structural features with Mongolia, India, and Southeast Asia — first-generation founders ageing out without infrastructure, institutional capital absent, no succession advisory sector. But three features make Nepal’s version distinct.

The double-crisis filter is a self-selecting screen. Consumer brand founders who held through ten years of Maoist insurgency and a 7.8-magnitude earthquake are not average entrepreneurs — they are tested survivors whose businesses carry crisis documentation of unusual depth and whose founders happen to be invisible to conventional capital.

The heir population is leaving. Nepal’s remittance economy is one of the largest in Asia as a share of GDP — approximately 25 percent of the national economy flows from overseas workers, primarily in Gulf states. The demographic dynamic that drives this applies directly to succession: skilled, educated Nepali young people have strong economic incentives to work in Qatar, UAE, or Saudi Arabia rather than return to manage a family business at $2–5 million revenue. The heir who would inherit a founder-built brand and scale it is increasingly choosing a Gulf salary. Founders who built through two catastrophes may find themselves unable to transfer what they built — not because no heir exists, but because the heir has made a different economic calculation.

The $5 million threshold requires recalibration. Nepal’s commercially established brands typically operate at $2–5 million — below the floor most institutional analysis uses as its entry point. This is not a quality signal; it is a market-size signal. The brands are real, the export relationships are documented, and the succession dynamics operate at full force.

The consequence is a wave breaking without observers. No PE fund targets Nepal consumer brands. The advisory infrastructure — family business consultants, M&A intermediaries — does not exist in Kathmandu. When these founders exit, they will exit into a void.

What Dwarika’s signals about the rest

The Dwarika’s Hotel succession is not a warning. It is the opening event of the wave.

Ambica Shrestha built Dwarika’s Hotel from 1991 — using traditional Nepali carved woodwork salvaged from demolished heritage buildings — into the most internationally recognised boutique hospitality property in Nepal. She was the first Nepali woman to secure bank loans for a hotel. During the 2015 earthquake, while the government’s response was slow and fragmented, Dwarika’s established Camp Hope — a relief operation that sheltered hundreds of survivors from Sindhulpalchowk district — and later funded a $5 million project to rebuild homes for 230 families using ecological building practices. A camp resident, quoted at the time: “Everything here is managed by Dwarika. The government has done nothing.” In 2024, the year she died, Spain awarded her the Order of Isabella the Catholic — one of the country’s highest honours for foreign nationals — in recognition of a career that had transformed Nepal’s hospitality sector and produced a working model of crisis-era cultural preservation. She died at 92. Her grandson, Rene Vijay Shrestha Einhaus — who had been based in Germany — returned to manage the property. Forty additional rooms are under construction. He has stated: “We’re trying to build a Nepali brand that reflects the beauty, variety and depth of our country and culture.”

What makes Dwarika’s significant is not the family continuity — it is the mechanism. A third-generation return from Germany is not succession infrastructure. It is a personal decision, made by one family, for one property, in the most documented case in Nepal’s hospitality sector. Across the 20–30 boutique hospitality operations that followed a parallel founder path — through insurgency, earthquake, pandemic, and decades of international relationship-building — no equivalent transition plan is visible. The founders who built those properties are the same age cohort as Ambica Shrestha. Several are already past 70.

The same mechanism — a founder reaching the end of a long arc, a next generation making a voluntary decision to return — is already visible in tea. Deepak Prakash Banskota founded Kanchanjangha Tea Estate in 1984, Nepal’s first certified organic tea estate, after visiting Darjeeling tea gardens in his teens and deciding that Nepal’s eastern hills could produce something comparable. He is now approximately 75. His son, Nishchal, runs US distribution from New Jersey through Nepal Tea Collective — structured deliberately as a public benefit corporation, embedding the estate’s mission into its legal form rather than leaving it dependent on family goodwill. His daughter manages BaskotaGroup and BG Tea Bar in Kathmandu. The estate’s scholarship fund has educated 2,300 students since 2002; 600 farmer-workers hold stakeholder status in its operations. The Banskota succession has been under active construction for years — not improvised at the moment of transition.

What separates Dwarika’s and Kanchanjangha from the rest of the wave is visibility. Ambica’s story was covered internationally; Banskota built an institution — scholarship fund, cooperative ownership — that made succession feel like an obligation. Across the 30–50 founders approaching the same window without that narrative depth, no equivalent decision is obvious. The difference between Kanchanjangha and an equally well-built tea garden whose founder has no internationally visible story is not the quality of the tea — it is the intelligence gap.

The wave is estimated to peak in 2028–2032. The intelligence exists: Nepali trade publications, export directories, Maoist-era crisis documentation — thirty years of recovery that no one has synthesised for an investor audience.

Nepal is not a market to enter. It is a market to document — founder by founder, in Nepali and in English — before the insurgency-and-earthquake generation finishes handing over what they built. Ambica Shrestha’s grandson came back from Germany. Most founders in her cohort do not have a grandson in Germany.