Skip to main content

Skip to main content

Myanmar: The Generation Nobody Documented

Myanmar's founder-owned consumer brands are invisible to institutional capital for three compounding reasons: a language barrier, post-coup geopolitical opacity, and FATF blacklisting. The brands exist at commercial scale — and the founders who built them during the 1990s opening are now 60 to 80, with no succession infrastructure in place.

Four zones, one generation: Myanmar's brand geography

The blacklisted generation, 1988–2022

Dr. Sai Sam Htun is 80 years old. He controls Loi Hein Company — Myanmar’s dominant independent beverage group, with Alpine water as the country’s leading water brand, Shark energy drink in a joint venture with Thailand’s Osotspa, and Asahi soft drinks through a separate JV with the Japanese company. Between 1,000 and 5,000 employees. No publicly identified successor.

This is not a hypothetical risk. It is the succession crisis that Brandmine was built to document — already underway, in a country where no institution is watching, in a sector where the intelligence infrastructure to find the next transaction simply does not exist.

Myanmar is not the most obvious illustration of the synchronized succession thesis. It is, arguably, the most urgent one.

Two documented transactions prove the market exists. In 2017, Thai Beverage acquired Grand Royal Group — Myanmar’s largest spirits company — for approximately $1 billion. In 2019, Colgate-Palmolive acquired Laser toothpaste for approximately $100 million. Both were Myanmar’s founder-owned brands at commercial scale. Both attracted institutional buyers. The intelligence infrastructure that should have been generating a pipeline of similar opportunities built nothing. Four years later, a military coup and FATF blacklisting made the problem dramatically harder to solve.

The brands are still there. The founders are ageing. Almost nobody is documenting them.

The opening that created a generation

The blacklisting is not just an obstacle for illicit money flows — it affects perfectly legitimate businesses run by law-abiding people who simply happen to be in Myanmar.

Myanmar’s private consumer brand economy was not built gradually. It was created in a narrow window of controlled liberalization that opened in 1992 and effectively closed by 2000.

After the military crackdown on the 1988 pro-democracy uprising, the State Law and Order Restoration Council found itself running a country with no functioning private sector. In 1992, under Than Shwe, SLORC initiated a partial economic opening — not democracy, but permission to earn. Import licenses, manufacturing permits, and distribution rights became available to a carefully filtered circle of entrepreneurs. The military maintained ultimate control. But within that constraint, Myanmar’s first private consumer brands were built.

The founders who obtained licenses during this eight-year window were typically in their thirties and forties. They built with limited capital, no foreign partners, and no institutional precedent. In food and beverage manufacturing, they competed against import restrictions that gave them a structural advantage. In tea, they formalized what had been artisanal and regional production into commercial brands. In beauty, they built from domestic supply chains and traditional formulations. The brands that emerged from this window would dominate Myanmar’s independent consumer sector for the next twenty-five years.

By 2000, the window had effectively closed. The political environment constrained new entry, and the existing cohort consolidated. The founders who had obtained their licenses were now settled into their businesses — building distribution networks, developing brand loyalty, and ageing.

A second wave arrived between 2011 and 2021. The quasi-civilian Thein Sein government initiated genuine market reforms. Foreign investment entered for the first time in a generation. A younger cohort — now 35 to 52 — built brands in specialty coffee, premium food, and lifestyle categories during this boom. Their situation today is different: many relocated to Bangkok, Chiang Mai, or Singapore after the 2021 coup, running Myanmar operations from diaspora positions. Their succession pressure is latent, not immediate. But their geographic flexibility makes them easier to reach.

The 1992–2000 cohort is the priority. These founders are now 60 to 80. Their businesses were built before mobile internet, before ASEAN integration, before any institutional investor had a Myanmar strategy. And they are running out of time.

Where the transition pressure is building

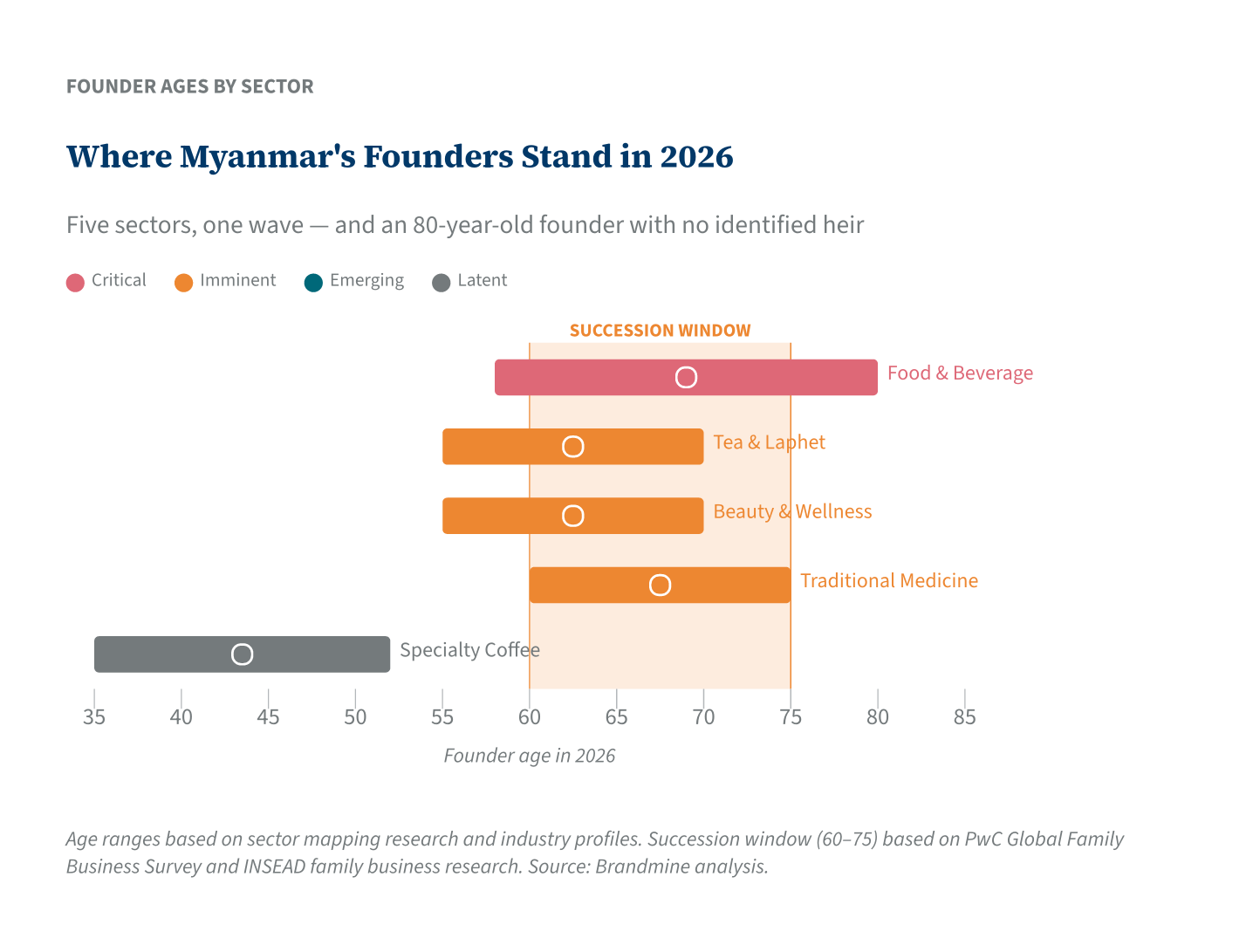

Brandmine’s sector mapping identified twelve consumer sectors with founder-owned brand activity in Myanmar. Five show meaningful succession pressure — sectors where established founder-owned brands exist at commercial scale, founders are within or approaching the transition window, and no succession infrastructure has been built. Here is what the wave looks like at the sector level.

Food and beverage manufacturing — the critical case

The most urgent succession cluster in Brandmine’s Myanmar coverage. An estimated 15–25 founder-owned brands operate at commercial scale in beverages, packaged foods, and dairy — the legacy of the SLORC import-restriction era. Founders are typically 58 to 80, with the upper end of that range already past the standard succession window.

Dr. Sai Sam Htun’s Loi Hein Company is the anchor case: market-leading positions in three beverage categories, no identified heir, and a founder who is 80 years old. But the broader cluster has the same profile — businesses built on founder relationships and personal licensing access, with no formal governance structures and no succession planning.

The sector also has the strongest transaction precedent: Laser toothpaste and Grand Royal both came from this cluster. The transaction infrastructure exists. What doesn’t exist is the intelligence layer to identify the next Laser or Grand Royal before it either transitions without planning or disappears when the founder exits.

Tea and laphet — the cultural anchor under pressure

Myanmar’s tea and laphet sector operates at the intersection of agriculture, processing, and a deeply embedded food culture. Laphet thoke (fermented tea leaf salad) is not a niche product — it is a national staple with regional and artisanal brand variation that creates genuine consumer differentiation. An estimated 12–20 founder-owned brands operate at commercial scale in tea processing and laphet production.

Founders are typically 55 to 70, with succession pressure rated imminent. The sector has managed to produce one international benchmark — Rangoon Tea House, which opened a Bangkok ICONSIAM location in December 2025 — demonstrating that Myanmar tea brands can cross borders. But the broader cluster has no such visibility, and no succession playbook for what comes after the founder. Most laphet brands sell through offline markets and Facebook. No investment database has captured them.

Natural beauty and wellness — the hidden export cluster

Myanmar’s natural beauty sector is the most internationally accessible, for a specific reason: the country’s botanical supply chains — thanaka, rosewood, jasmine, tamarind — are distinctive enough to support genuine product differentiation in export markets. An estimated 8–15 founder-owned beauty brands operate at commercial scale, with founders typically aged 55 to 70.

Yathar Wathi — distributing on Amazon and Etsy — is the clearest example of what export-readiness looks like from a Yangon base. Shwe Pyi Nann’s Thailand subsidiary and Amazon India presence demonstrate a parallel distribution logic. Thanaka as an export product already meets the Western consumer on familiar terms: natural cosmetics, traditional ingredient, minimal-intervention skincare. The Amazon channel works without a translator. The sector found its export path before anyone documented it systematically. The gap on the map remains — but brands with live sales are already standing on it.

Wellness and traditional medicine — the least visible cluster

Myanmar’s traditional medicine sector is simultaneously the most culturally entrenched and the least documented. FAME Pharmaceuticals — WHO GMP certified, ISO certified, with a Singapore distribution hub — represents the sector’s ceiling: a founder-owned company that has achieved international quality credentials without institutional capital. Founders in this sector are typically 60 to 75, with succession pressure rated imminent.

The sector’s challenge is documentation. Traditional medicine brands operate through distribution networks that are invisible to any standard commercial database. The intelligence gap here is not just about succession — it is about the basic question of which brands exist at what scale. FAME Pharmaceuticals solved the documentation problem through certification: ISO and WHO GMP are credentials that read outside Myanmar. Most competitors in the sector have no such credentials. They operate, earn revenue, and age outside the sight of any system that could manage the transfer of their business.

Specialty coffee, reaching international markets

Myanmar’s Arabica coffee, grown at altitude in the Shan Plateau around Pyin Oo Lwin and the Ywa Ngan district, is beginning to reach international specialty markets. The founder cohort here is younger — typically 35 to 52 — which places succession pressure in the latent category.

The coup complicated this sector specifically: many specialty coffee founders were also socially engaged entrepreneurs who faced post-coup targeting. The Bangkok and Chiang Mai diaspora communities have become de facto incubators for the sector’s continued development. Myanmar’s specialty coffee market is small by global standards, but its advantage lies elsewhere: Shan Plateau Arabica has a cup profile that buyers in Japan, South Korea, and Northern Europe will pay for by the lot. This segment does not require scale — it requires documentation and relationships.

What the databases miss

PitchBook has no Myanmar consumer brands. Bloomberg covers nothing below the SGX-listed Yoma Strategic Holdings. Crunchbase has fragments. The Economist Intelligence Unit covers Myanmar’s macroeconomics, not its brand landscape. The intelligence gap is not because the brands are small — it is because the documentation infrastructure does not exist.

What does exist is a Burmese-language Facebook ecosystem. Most Myanmar consumer brands at commercial scale operate primarily through Burmese-script Facebook pages — some with 200,000 to 600,000 followers. No English corporate registry captures these entities. No international business press has profiled them. They are completely visible to any Burmese-speaking researcher with Facebook access and completely invisible to any institutional investor working through conventional channels.

Myanmar has a specific compounding factor: the Burmese script is a barrier even for those who are searching. The three alphabets a typical Asian markets analyst reads — English, Mandarin, Thai — give no access to the Myanmar corpus. A Facebook page with 400,000 followers written in Burmese script is invisible to an English Google search. The invisibility is not incidental. It is structural.

Two transactions prove this matters. Grand Royal and Laser toothpaste were not discovered through standard due diligence pipelines. They were known quantities within the Myanmar business community that eventually reached institutional buyers through relationships. Myanmar consumer brands demonstrably attract institutional capital. What does not yet exist is a system for identifying the next generation before the founders who built it are gone.

The ownership filter

Not every Myanmar brand can be engaged. The military conglomerate filter is mandatory and non-negotiable.

MEHL (Myanmar Economic Holdings Limited) and MEC (Myanmar Economic Corporation) are the military’s two primary investment vehicles. Together they control beer (Myanmar Brewery), jade, gems, tobacco, banking, and multiple consumer goods categories. The UN Fact-Finding Mission in 2019 documented MEHL’s structure and named its key conglomerate partners. US, EU, and UK sanctions have since targeted specific entities and individuals within this network. Any engagement with Myanmar consumer brands requires a pre-screen against MEHL/MEC ownership structures and the broader crony network documented by Justice For Myanmar.

The sectors that matter for Brandmine’s coverage — food manufacturing, beauty, tea, and traditional medicine — are substantially independent of military ownership. MEHL’s interests concentrate in extractives, utilities, and a few consumer categories (beer, cigarettes). The beauty founders who built on thanaka and local botanicals are not MEHL subsidiaries. The laphet producers in Mandalay are not MEC partners. The SLORC-era licensing process did create dependencies, but the consumer brand founders who obtained those licenses are not, as a group, military-affiliated.

The FATF blacklisting is a separate and more pervasive challenge. Myanmar was placed on the FATF blacklist in October 2022 — alongside North Korea and Iran — for deficiencies in anti-money-laundering frameworks and terrorist financing controls. The practical consequence is that most international banks refuse any Myanmar transactions regardless of the specific counterparty’s ownership or compliance status. This is not targeted sanctions; it is a blanket banking refusal that affects legitimate founder-owned brands as severely as it affects military-adjacent entities.

The Singapore pathway is the most viable current route. Singapore-registered entities can legally transact with non-sanctioned Myanmar businesses. Singapore’s Ascent Myanmar Growth Fund and Yoma Strategic Holdings (SGX-listed) were the pre-coup entry points for legitimate Myanmar investment. Post-coup, these vehicles have contracted but not disappeared. FAME Pharmaceuticals’ Singapore distribution hub is a proof point: a Myanmar founder-owned company that built an international commercial infrastructure through the Singapore gateway before the coup made that pathway harder.

The FATF blacklisting is not permanent. Myanmar’s trajectory toward removal will depend on political developments that are difficult to forecast. The ownership filter itself, however, does not depend on that timeline: the MEHL/MEC pre-screen, the Singapore-registration status of individual founders, and the sector-by-sector documentation of which clusters sit clear of military entanglement are facts that can be established now, independent of when — or whether — the blacklisting changes.

Dr. Sai Sam Htun is 80

The standard framing for emerging-market opportunity is forward-looking: here is what will happen when the market opens. The Myanmar case is different. It is already late.

Dr. Sai Sam Htun is 80 years old. The succession window for the food and beverage cohort — defined by PwC’s Global Family Business Survey and INSEAD research as ages 60 to 75 — has already been missed for the upper end of that range. The brands that founders in the 65-to-80 cohort have built over thirty years are approaching a transition point with no infrastructure to manage it. When a founder at this age exits without a plan, the outcome is typically not a graceful sale — it is brand erosion, family conflict, or quiet disappearance.

Myanmar’s most urgent succession cases — brands worth $5 million to $500 million-plus in consumer sectors untouched by institutional capital — remain undocumented while the 80-year-old cohort approaches exit without succession plans. Left to conventional channels, these cases do not surface through managed transactions; they resolve through the unmanaged exits that happen when nobody was watching — brand erosion, family conflict, quiet disappearance.

Myanmar is not a market to enter. It is a market to document — in Burmese, through the Singapore gateway, against the MEHL/MEC screen — before the 1992–2000 cohort finishes ageing out. The next Grand Royal already exists. Whether it transacts, fragments, or quietly disappears depends on whether anyone assembled the intelligence while the founder was still at his desk.