Skip to main content

Skip to main content

Mozambique: what peace built, succession tests

In 1992, a ceasefire created Mozambique's private sector almost overnight. Thirty-three years later, the founders who built during that peace dividend are entering succession simultaneously — and no institutional investor has been paying attention. Five sectors. One undocumented wave.

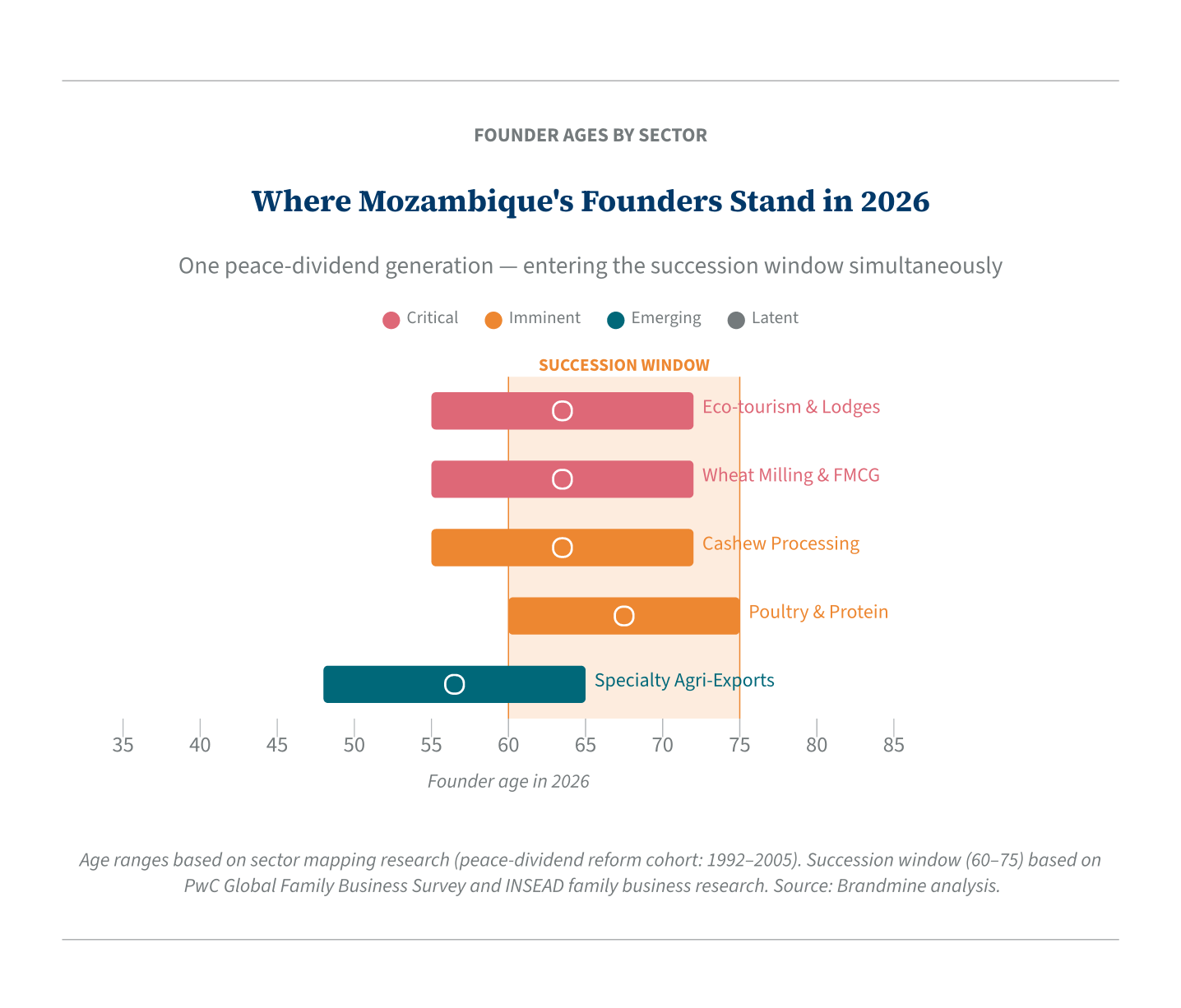

Five clusters, one peace-dividend generation: Mozambique's succession map

The peace-dividend generation, 1992–2026

In February 2025, Dubai-listed Invictus PLC quietly completed its acquisition of Merec Industries — a Maputo-based wheat milling and pasta operation founded in 1998 by Mozambican entrepreneur Mhamud Charania, who had built to roughly $60 million in annual revenue without a single share of external capital. The deal had been years in construction: Amethis, Proparco, and Kibo Capital had entered as minority shareholders in 2018, after Merec survived a national debt crisis that had wiped out the equivalent of Mozambique’s entire annual GDP in hidden government liabilities. When Invictus closed, twenty-seven years of founder-built milling infrastructure in Matola transferred to a foreign-listed company. No Mozambican successor was in the picture.

This is not an anomaly. It is Mozambique’s succession pattern made legible for the first time: first-generation founder builds through crisis; institutional partners orchestrate the transition; the brand exits to a foreign acquirer. Whitepaper No 1 documents a synchronized transition wave across emerging markets — reform-era founders ageing out simultaneously, institutional investors unprepared. Mozambique is what that thesis looks like when the founding window was opened not by economic liberalisation but by the end of a war — and when the founders who survived the opening have since survived four additional compounding shocks that no analyst has documented for a capital-markets audience.

From ceasefire to succession in thirty years

Unfair competition and the lack of financial support aggravated by the pandemic crisis have already caused the closure of around 10 factories.

Mozambique’s private sector was created by one date: October 4, 1992. The General Peace Accords signed in Rome ended sixteen years of civil war and opened the country’s first modern economic window. Within three years, the World Bank had structured the privatisation of more than 1,200 state enterprises, and a generation of founders was building consumer businesses — in cashew processing, wheat milling, lodge operations, specialty agri-exports, and poultry — from a base of near-zero private infrastructure.

The Mozambique founding window ran roughly 1992 to 2005: thirteen years of post-war reconstruction, accelerating privatisation, and a GDP growth rate that averaged nearly 8% annually between 2000 and 2016. That cohort is now 52 to 72 years old. And unlike some emerging market waves — India’s 1991 LPG reforms, which produced founders across a twenty-year arc; Russia’s extended 1990s privatisation, which layered cohorts across a decade — Mozambique’s wave is compact. A single ceasefire produced a single founding generation, building in similar conditions, now entering the succession window at almost exactly the same time.

The compression is different from Mongolia’s (where a 1990 democratic revolution created an entire private sector in roughly two years). Mozambique had a decade. But that decade still produced a tightly bounded cohort — and unlike India or Russia, Mozambique’s founders built without formal succession traditions, without family business advisory infrastructure, and without any preceding private-sector generation to learn from. Their succession is not a managed intergenerational transfer. For most, it will be a first-time event with no institutional framework to navigate it.

The sectors where that cohort concentrated trace the country’s peace-dividend story: cashew processing, rebuilt from near-zero after post-independence state mismanagement by a new generation of entrepreneurs; eco-tourism and lodges, a direct function of international re-engagement with Mozambique’s coastline post-1992; specialty agri-exports, shaped by 1990s export liberalisation and post-2000 DFI co-investment; wheat milling and branded FMCG, represented by the Merec generation; and poultry and animal protein, built to supply an urbanising Maputo.

Clusters formed by peace, shaped by crisis

These five clusters define the shape of Mozambique’s founder generation — and carry its succession urgency.

Cashew processing and branded nuts concentrates an estimated 15 to 25 founder-owned brands at commercial scale, with founders predominantly in the 55-to-72 range. Succession urgency: Imminent. The cashew sector is Mozambique’s most legible succession story: a post-2003 rebuild driven by TechnoServe-supported founder-entrepreneurs who built processing capacity from scratch, sourcing from roughly 100,000 smallholder farmers. By 2020, the INCAJU/AFD competitiveness audit found only 11 of 26 processing companies still operating — roughly 40% of the sector — following the combined impact of the 2016 debt crisis, unfair competition from raw nut exporters, and COVID. Gross cashew export revenues reached $121.6 million in 2025, suggesting that the survivors have consolidated meaningfully. The founders who held through that contraction built for resilience. The CEAM industry association provides a structured point of entry for scoping this cohort.

Eco-tourism, lodges and resorts covers an estimated 20 to 35 founder-owned brands at commercial scale, with founders concentrated in the 55-to-72 range. Succession urgency: Critical. Mozambique’s coastal lodge sector is the country’s most internationally visible cluster of founder-owned consumer businesses. The Inhambane, Bazaruto, and Niassa sub-clusters provide the geographic anchors. The founding cohort is distinctively Portuguese-Mozambican — families who built lodge operations in the post-1992 opening and maintained them through storms, pandemic, and a regional insurgency that closed the entire northern cluster. The quadruple disruption stack (Cyclones Idai and Kenneth in 2019, COVID from 2020, Cabo Delgado since 2017, currency devaluation) has made succession conversations explicit in this sector in ways they were not five years ago. Several founders have discussed exit timelines publicly with regional hospitality operators; the transaction infrastructure for that conversation has not yet materialised.

Specialty agri-exports — sesame, baobab, macadamia, coconut — covers an estimated 12 to 20 founder-owned brands at commercial scale, with a younger founder age band of 48 to 65. Succession urgency: Emerging. This sector reflects the growth-era cohort rather than the immediate peace-dividend cohort: founders who built during the 2000s export liberalisation and early DFI engagement period. Development finance has begun flowing into the corridor — AgDevCo into macadamia, Norfund and Zebu Investment Partners into agri-exports — signalling institutional confidence in founder-owned producers here ahead of the wider market. Macadamia exports reached €33.9 million in 2025. The DFI presence means transition infrastructure is already forming in this sector — which pushes succession urgency to Emerging rather than Imminent.

Wheat milling, pasta and branded FMCG concentrates an estimated 8 to 15 founder-owned brands at commercial scale, founders predominantly 55 to 72. Succession urgency: Critical. Merec Industries is the archetype, and the February 2025 exit establishes the pattern. Smaller millers in Beira, Nampula, and Quelimane likely trace the same founder profile — 1990s founding, no institutional capital, crisis survival, now at the age where succession decisions cannot be deferred. The sector is documentation-thin relative to cashew or lodges, which makes the Merec transaction more significant as a precedent: it proves the pattern is real, and it proves that institutional buyers are willing to pay for Mozambican FMCG assets once properly intermediated.

Poultry, animal protein and feed covers an estimated 5 to 10 founder-owned brands at commercial scale, with founders predominantly 60 to 75. Succession urgency: Imminent. The sector’s clearest brands were built in the early 1990s to supply an urbanising Maputo, and their founders have stayed at the helm ever since — tenures of four decades that span the peace accords, the debt crisis, and the cyclones. Institutional capital has begun to validate the sector’s scale: IFC debt financing for second-phase processing expansion signals that the largest founder-owned operations have reached commercial maturity at exactly the point their founders reach the succession decision. The pool is smaller than cashew or eco-tourism, but each brand carries strong NDD potential: the story of supplying a growing city through a decade of compounding disruption without a single year of institutional capital.

What four shocks in eight years produced

Mozambique’s succession urgency was not the result of ordinary founder ageing. It was accelerated by four compounding shocks between 2016 and 2021 that compressed the timeline, depleted reserves, and — for the founders who held through all of them — produced the deepest crisis documentation anywhere in sub-Saharan consumer brand history.

The first shock was fiscal. The 2016 Tuna Bond scandal — $2 billion-plus in previously undisclosed government liabilities, approximately equal to Mozambique’s entire annual GDP — suspended donor support, collapsed the currency, and reduced FDI by roughly 40%. Founders who had structured conservative exit timelines found the timeline accelerated by a macroeconomic event entirely outside their control.

The second and third shocks were meteorological. Cyclone Idai (March 2019) and Cyclone Kenneth (April 2019) constituted the most destructive back-to-back storm season in Mozambican recorded history. Idai destroyed Beira and its agricultural hinterland; Kenneth struck Nampula’s cashew-growing districts. Together, the storms disrupted cashew supply chains, damaged lodge infrastructure, and arrived while the debt crisis was still unresolved. COVID-19 followed within twelve months, closing the eco-tourism sector during its recovery period.

The fourth shock continues. The Cabo Delgado insurgency has effectively closed the Quirimbas Archipelago’s lodge cluster — Anantara Medjumbe, Vamizi Island, and the Pemba Beach Hotel — while disrupting cashew supply chains from Mozambique’s northernmost growing belt. The northern cluster is not in Brandmine’s viable scope; the impact on the viable clusters is the psychological and financial pressure it has added to founders already navigating three prior crises.

For the founders who survived all four, the operational intelligence is extraordinary and entirely undocumented. No analyst has written the resilience profile. The supplier relationships that held through a currency collapse and back-to-back cyclones, the export networks rebuilt after COVID, the ecological knowledge accumulated through thirty years of Mozambican coastal management — this is the NDD material. And its carrier is, right now, at the age where the decision to hold, transfer, or sell becomes unavoidable.

The succession events no one is watching

The Merec exit to Invictus PLC was Mozambique’s most legible succession event — PE-intermediated, announced in the press, closed with foreign capital at a documented premium. Most Mozambican succession events will not look like this.

They will be cashew factories passed to adult children who lack the founder’s supplier relationships with 100,000 smallholder farmers. Lodge operations absorbed by South African or Mauritian hotel groups for whom the ecological knowledge accumulated over three decades of Mozambican coastal management is an afterthought in the acquisition memo. Milling businesses sold informally to trading partners at valuations set by information asymmetry rather than market discovery — because no formal succession infrastructure existed to produce any other outcome.

The development finance institutions are already present: Amethis, Proparco, Kibo Capital in FMCG; Norfund and Zebu in agri-exports; AgDevCo in macadamia; IFC in poultry. Their investments validate commercial scale. But DFI exits typically produce foreign acquisitions or management buyouts — they do not produce Mozambican successor platforms, and they do not produce the qualitative intelligence on what these founders built through crisis. Undocumented, that intelligence disappears into the transaction.

No independent investment intelligence platform currently covers Mozambique’s founder-owned consumer sector in Portuguese. The fragments exist — in Noticias, in Club of Mozambique, in Canal de Mozambique, in the INCAJU audit, in the AgDevCo and IFC press releases, in the TechnoServe archives from the 2003 cashew rebuild. A founder cohort that survived a hidden-debt crisis, two category-five cyclones, a regional insurgency, and a global pandemic has produced thirty years of crisis documentation that no institutional buyer has ever synthesised. The intelligence exists in scattered form. The synthesis belongs to no one.

The founders of Mozambique’s peace-dividend private sector will make their succession decisions between 2026 and 2033. Merec went first. The cashew cohort — survivors of the 11/26 contraction, now sitting on consolidated market positions and export revenues that tripled in a single year — will go next. Then the lodge founders, who have already had the conversation privately with regional operators. Then the milling families in Beira and Nampula. Then the poultry family that IFC backed and that has been in the sector for four decades.

The Mozambican business press, read now, in Portuguese, and mapped against these founders before their decision point, holds intelligence that will not be recoverable once the transactions close. After 2030, only the acquisition records will remain — records whose terms were set in 2026, while the succession wave was still forming and the founders were still reachable.