Skip to main content

Skip to main content

Mongolia: Where No One Is Watching

Mongolia has 3.4 million people, seventy million livestock, and a first generation of private-sector founders who survived triple-digit inflation, six IMF bailouts, and catastrophic winters that killed millions of animals. Now aged 53 to 73, they built consumer brands in cashmere, hospitality, retail, and food with no playbook and no predecessors. The succession clock is running — and nobody is watching.

One City, One Generation: Mongolia's Succession Geography

Transformation Arc

Mongolia has 3.4 million people, seventy million livestock, and a first generation of private-sector founders who built consumer brands from nothing after the 1990 democratic revolution. Now aged 53 to 73, they survived triple-digit inflation, six IMF bailouts, and catastrophic winters that killed millions of animals — and not one of them has a succession plan.

Whitepaper № 1 documents a synchronized transition wave across emerging markets: reform-era founders ageing out simultaneously, institutional investors unprepared. Mongolia is what that thesis looks like at the country level — compressed into a single decade, concentrated in one city, and entirely undocumented.

Unlike Russia’s oligarch-dominated privatization, Mongolia’s 1990 transition produced a broader base of small-to-medium founder-owned businesses across consumer sectors that institutional investors have never documented. Half the population lives in Ulaanbaatar — which means the stories are geographically concentrated and the brands are findable. But the total addressable pool at commercial scale is structurally smaller than in larger markets, and the intelligence gap is almost total. No systematic succession research exists. No dedicated consumer-sector PE targets Mongolia. What these founders built has been hiding in plain sight.

The compressed wave

Mongolia's senior talent market is a talent puddle.

Mongolia’s succession wave is not a gradual demographic shift. It is a compression event — the most extreme in Brandmine’s coverage.

In most emerging markets, founder cohorts formed over two or three decades as successive reform waves created entry points for private enterprise. China’s wave spans 1978 to 2001. India’s runs from 1991 to 2005. Russia’s stretches across the late 1980s to the late 1990s. In Mongolia, the entire private sector was created in roughly two to three years.

The 1990 democratic revolution dismantled every state enterprise, every supply chain, every guaranteed procurement contract simultaneously. In 1991, citizens received privatisation vouchers for state assets — the same mechanism Russia used, but in an economy with no private-sector tradition, no capital markets, and no predecessors to learn from. By 1992, the first consumer brands were appearing in the middle of economic freefall: cooperatives that would become retail conglomerates, tourism operations launched into a country with no tourist infrastructure, cashmere ventures navigating a supply chain that was collapsing and restructuring at the same time.

What makes this compression unusual is not just the speed but the simultaneity of the crises that followed. Every founder in this cohort faced the same sequence: hyperinflation in the early 1990s, banking system collapses in 1996 and 1999, catastrophic dzud winters that killed millions of livestock and shattered cashmere supply chains, a commodity boom that created Mongolia’s first real consumer middle class after 2004, a commodity crash in 2014 that tested whether these brands could survive without mining-fuelled demand, and a pandemic that collapsed tourism to zero. No other country in Brandmine’s coverage compresses this many existential crises into a single founder generation.

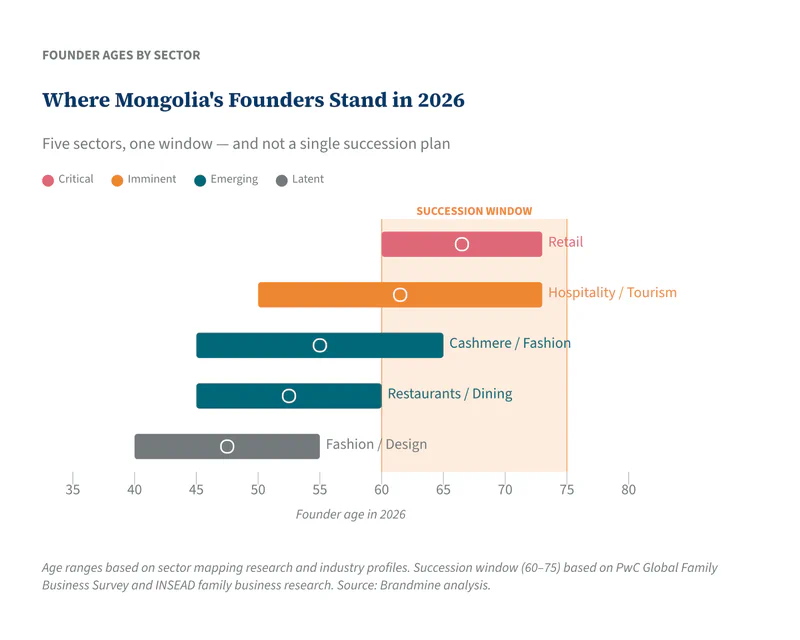

The result is a cohort that is extraordinarily crisis-hardened — and extraordinarily synchronised. Founders across five consumer sectors are now aged 53 to 73, with the heaviest concentration between 58 and 68. Retail founders are already deep in the succession window. Hospitality founders are entering it. Cashmere and dining founders are approaching. Fashion designers, the youngest cohort, have another decade. But the compressed founding window means the transition pressure is hitting all sectors within the same narrow timeframe — and there is no succession infrastructure to absorb it.

Where the transition pressure is building

Brandmine’s sector mapping identified ten consumer sectors with founder-owned brand activity in Mongolia. Five show meaningful succession pressure — sectors where established founder-owned brands exist at scale, founders are within the transition window, and no succession infrastructure has been built. A complete sector study of Mongolia’s natural beauty and wellness sector is already published — sixteen brands profiled, crisis narratives documented. Beyond beauty, here is where the wave is breaking.

The sector that built the international reputation — and is now losing its heirs

Mongolia is the world’s second-largest cashmere producer. An estimated 12–18 founder-owned brands operate at or near commercial scale, with founders typically aged 45–65 — succession urgency: emerging. One corporate group commands over 70% of the domestic retail market, but beneath that dominance a founder-owned segment is building international distribution from the ground up: exhibiting in Paris, supplying private-label clients, navigating a supply chain where roughly half the raw material is smuggled to China before it reaches domestic manufacturers.

The sector’s most visible succession attempt — at the industry’s largest company in 2024-25 — ended with the heir fleeing the country. It is a warning signal for the entire founder cohort.

The founders who bridged two worlds — and have no one to hand off to

Mongolia’s hospitality and tourism sector carries the most acute succession pressure in the country. An estimated 15–25 founder-owned brands, with founders aged 50–73 — succession urgency: imminent. Several are already deep in the window. The sector attracted adventure travellers and cultural tourists at growing rates before COVID collapsed inbound arrivals to zero. Tourism receipts that had been climbing through the 2010s vanished overnight — a crisis that hit founders in their sixties harder than it hit the younger operators who could wait it out.

A distinctive diaspora-return pattern recurs across this sector: Western education, Mongolian heritage, businesses built to bridge both worlds. Several of these founders hold decades of international recognition — awards, press coverage, relationships with international travel platforms that took years to build. The pandemic added a severe crisis narrative to founders already approaching the succession window, and no institutional buyer has appeared to catch what they built. The assets that make these operations valuable — supplier relationships, international booking networks, cultural credibility — are personal, not institutional. No succession plan exists that addresses how those assets transfer.

The conglomerate that holds 1% of the national economy — with no visible successor

Mongolia’s retail sector is the smallest brand pool (5–8 founder-owned operations) but carries the highest individual stakes — succession urgency: critical. At least one retail conglomerate accounts for a measurable share of national GDP, employs thousands, and has operated under its founding generation since 1992. No public succession plan is visible. No second-generation leadership appears in corporate materials. Two conglomerates — Tavan Bogd and MCS — span retail and multiple other sectors, and distinguishing founder-owned brands from conglomerate subsidiaries requires analytical frameworks that do not yet exist for Mongolia. This is founder-dependent risk at a scale that affects the national economy, not just a sector.

The designers building a new Mongolian identity — time still on their side

Mongolia’s fashion sector is younger and less commercially mature than cashmere, but produces the most internationally visible brand stories: Olympic uniforms, global press coverage, a generation of designer-founders building contemporary fashion from traditional Mongolian elements — deel-inspired silhouettes, nomadic aesthetic references, felt and leather craft.

Most of these founders are younger than the succession-window cohort — aged 40 to 55 rather than 53 to 73 — succession urgency: latent. The intelligence opportunity here is emerging rather than urgent.

The dining founders who outlasted six crises — and are just starting to think about exit

Ulaanbaatar’s dining sector is smaller than the other priority sectors but contains founder-owned operations with 25+ locations and mining-site catering contracts that generate revenue streams invisible to consumer-facing analysis — succession urgency: emerging. Several of these founders built their chains during the mining boom years, when Erdenet and Oyu Tolgoi demand created a catering economy that dwarfed anything the domestic market alone could support. The broader café market is dominated by Korean franchises, which limits the founder-owned pool but makes the surviving Mongolian-founded chains — built through six successive crises — all the more significant.

Why this wave breaks differently

The compressed founding window that created Mongolia’s founder cohort also explains why its succession crisis will be more acute than in larger markets.

Mongolia’s private sector is one generation old. There are no succession traditions to draw on — no family business councils, no established heir-training practices, no precedent for the transfer of founder-built consumer brands to a second generation. In Russia, at least some oligarch families had a decade to experiment with succession structures. In India, family business governance draws on centuries of merchant-caste tradition. Mongolia has nothing. The entire concept of private-sector succession is as new as the private sector itself.

The talent constraint makes this structural. Executive search firms describe Mongolia’s senior leadership market as a “talent puddle” — not a pool, a puddle. In a country of 3.4 million, the number of executives with the experience to run a founder-built consumer brand through a leadership transition can be counted in dozens, not thousands. When a founder steps back, there may be no one qualified to step forward. The compressed wave means this constraint hits every sector simultaneously rather than sequentially.

The Gobi Corporation succession attempt is the first visible signal of what happens when the compressed wave meets the infrastructure gap. Mongolia’s largest cashmere company — its most internationally recognised consumer brand — transitioned from founding-generation CEO to his son in 2024. The heir fled the country after an altercation in mid-2025. This is not an isolated failure at one company. It is the preview of what the compressed wave produces when first-generation wealth meets the absence of institutional succession infrastructure: a sector-defining brand in crisis, with no system to catch it.

In a $23.6 billion economy, the revenue threshold that defines “commercial scale” may need recalibration — some of Mongolia’s most compelling founder stories operate at $1–4 million. But the succession dynamics operate at full force regardless of scale. A founder who built a 200-person cashmere operation from a 1992 cooperative faces the same transition challenge as a founder who built a billion-dollar conglomerate. The wave does not distinguish by size.

The window and what it means

The compressed wave is already breaking. Across five sectors, founders aged 53 to 73 are approaching or inside the transition window simultaneously, with no infrastructure to absorb their exit. There are no PE firms specialising in consumer-brand buyouts in Mongolia. No family business advisory sector. No second-generation leadership pipeline. The founders who built these brands from crisis will face the succession question alone — and the compressed founding window means they will face it at the same time.

The investor who documents these brands before the transition wave peaks holds a structural advantage that cannot be acquired after the event. What disappears when a founder exits without a plan is not just a brand — it is the relationships, the crisis-hardened knowledge, the supplier networks built over three decades of improvisation. The intelligence to find these founders, understand what they built, and act before the window closes exists. It is scattered across Mongolian business press, sector research, and thirty years of crisis documentation. It has not been assembled anywhere.

These brands have been here all along. Hiding in plain sight — and the window to move first is narrowing.