Skip to main content

Skip to main content

The 50,000-to-9,000 Floor: Penang's Food Houses

Between 2008 and 2024, George Town's UNESCO heritage core lost four of every five residents — from roughly 50,000 to 9,000 — even as six million tourists arrived each year. The century-old food houses that define the quarter didn't fold. They handed over to a fourth generation rebuilding around e-commerce and diaspora demand.

Malaysia Gourmet Foods: A Five-Region Heritage Cluster

When 50,000 became 9,000

In April 2021, a Cantonese sundry shop on Campbell Street switched on its first website. Kwong Tuck (廣德) had sold dried seafood, preserved goods and rice wine to George Town for 185 years without one. It went online in the middle of a pandemic, in a quarter that had just shed four of every five residents it once served.

The shop is not an outlier. It is the oldest documented member of one of Southeast Asia’s most concentrated — and least catalogued — founder-owned food ecosystems. The cluster reaches well beyond Penang: it runs from George Town’s shophouses through the coffee roasters of Ipoh and the soy-sauce houses of Taiping and Kelantan, down to the dodol makers of Melaka, and across the South China Sea to the layer-cake factories of Kuching. Five regions, roughly 1,500 kilometres apart, held together not by geography but by a shared craft lineage and, lately, a shared problem.

What survived the repeal

The houses descend from a single migration. Between the 1820s and the 1940s, Hokkien, Cantonese, Teochew and Hainanese traders carried their pastry, preserving and fermentation crafts into the Straits Settlements, where they crossed with Peranakan and Malay sweets. The result was a distinct repertoire — biscuits, soy sauces, palm-sugar caramels, sesame oils — sold from the same pre-war shophouses for three, four and five generations.

For most of the twentieth century, rent control kept those shophouses affordable. That ended in 1997, when Malaysia repealed the Control of Rent Act, with effect from 2000. Protection on George Town’s pre-war buildings vanished, and a slow displacement of resident trades began.

For a food trade, the threat was particular. These were never destination restaurants living on visitors; they were neighbourhood houses selling soy sauce, biscuits and preserved goods to the families who lived upstairs and next door. When a landlord could finally raise the rent, the residents left first — and the daily custom that sustains a sundry shop or a bakery left with them, long before any tourist arrived to take their place.

UNESCO inscription in July 2008 accelerated it. World Heritage status was meant to protect the quarter; instead it priced out the people who lived in it. Rents and house prices climbed, tourists arrived, and the residents who had bought biscuits and soy sauce as daily staples drained away. By November 2024, Penang Heritage Trust president Clement Liang could put a number on the loss: the heritage-core resident population had fallen from roughly 50,000 before 2008 to about 9,000 — an 82% collapse in sixteen years, even as Penang welcomed some 6.39 million tourists in 2019 alone.

A food trade built on neighbours had lost its neighbourhood. What it had not lost was its recipes, its premises, or — crucially — its successors.

Five regions, one lineage

The cluster’s strength is that it was never only Penang. Each region developed its own specialism, and each carries the crisis differently.

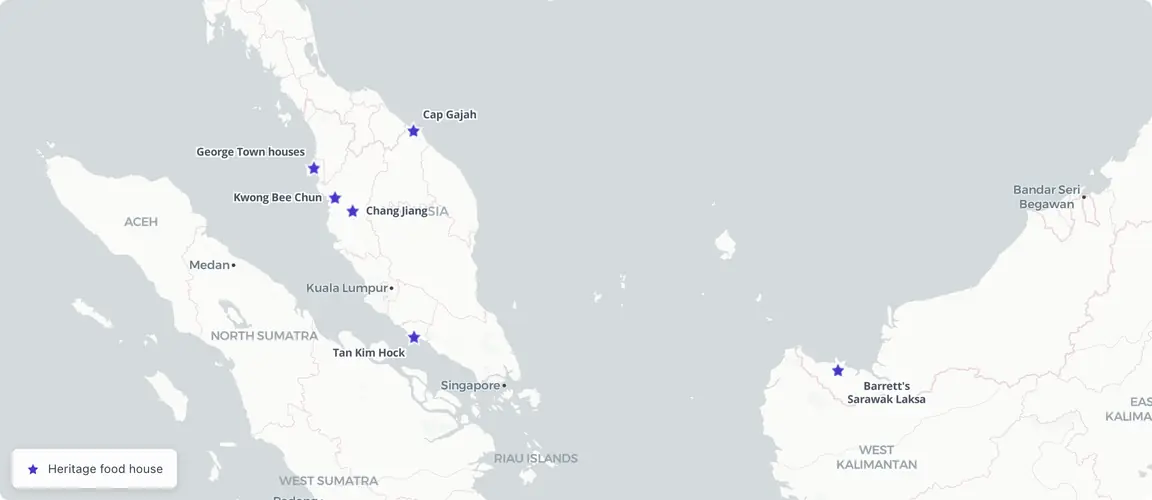

Penang is the epicentre and the wound. George Town’s biscuit and sundry houses — Kwong Tuck, Ng Kee, Loong Nam, alongside anchors such as Ghee Hiang (1856) and Him Heang — sit inside the 259-hectare UNESCO zone that lost its residents. Their pastry often uses pork lard, a deliberate non-halal positioning that locks them out of Malay-domestic and Gulf markets but cements them with Chinese-diaspora buyers who reject any substitution.

Perak turned coffee and fermentation into export goods. Ipoh’s limestone-cave water and Hainanese coffee-shop tradition produced Chang Jiang’s white-coffee powder; Taiping’s Kwong Bee Chun (廣美珍) has run a months-long natural soy-sauce fermentation since 1926.

Sarawak, a thousand kilometres east in Borneo, is the cluster’s clearest counter-example to the Penang stereotype. Here the heritage-food economy is Malay, female-led and halal-certified: kek lapis, granted Protected Geographical Indicator status by the state in 2010, is made by entrepreneurs such as Datin Masnah of Mira Cake House and Dayang Salhah, with one of the few non-Muslim operators, Maria Ngui, holding strict halal certification to compete in the same category.

Melaka is dodol and gula melaka country, built on Peranakan heritage and the Jonker Walk tourist axis. Kelantan, on the conservative east coast, is soy-sauce territory — Poh Yuen Chan’s Cap Gajah (大象牌, “elephant brand”) has carried its kicap across Kelantan, Terengganu and the Thai border town of Golok for three generations.

Different products, different faiths, different islands. The same inheritance.

What the databases miss

None of this appears where institutional capital looks. Search PitchBook, Crunchbase or Bloomberg for the firms in this article and you will find nothing — not because the businesses are small or informal, but because three barriers stack on top of one another.

The first is structural. Almost every house is a private Sdn Bhd whose accounts sit behind paid SSM filings; revenue is genuinely opaque, even to a diligent analyst. A ranking framework that defaults to financials simply cannot see the sector, which is why founding year and verified generation count are the only durable proxies.

The second is linguistic. The richest documentation of these brands lives in Chinese- and Malay-language press — Sin Chew Daily, Oriental Daily, the Borneo Post in Bahasa Malaysia — and in the oral histories archived by George Town World Heritage Incorporated. An English-only screen returns a tourism backdrop, not a founder ecosystem.

The third is interpretive. When the world does look at George Town, it sees a UNESCO postcard. The Penang Institute and Penang Heritage Trust have spent years arguing the opposite case — that these old trades are “cultural definers,” not tourism props — and their June 2020 crisis survey is the kind of primary intelligence that exists in plain sight and is almost never assembled into an investable picture. The gap is not that the information is missing. It is that no one has put it together.

That is the gap this article closes. The cost of assembling this picture is measured in language access and patience, not in proprietary data feeds — and the houses themselves, having just survived an existential decade, have rarely been more willing to talk about how they did it.

Who’s still standing

The cluster’s response to two simultaneous shocks has been bimodal, and the brands that demonstrate it are not adjectives in a directory — they are people who made specific decisions when quitting was the rational choice.

Kwong Tuck is the clearest case. When the pandemic erased the walk-in trade that gentrification had already thinned, the fourth-generation owner — by then in his late eighties — did not retire the 185-year-old shop. In April 2021 he registered kwongtuck.com and moved to nationwide WhatsApp delivery, naming his successors publicly the same year the trade won a George Town World Heritage Platinum award for cultural continuity.

Ng Kee, the Cantonese bakery on Cintra Street, did the opposite first and the same thing after. Though the food sector was exempt from closure, the family voluntarily shut for three months in 2020 — and used the rupture to bring in the fourth generation, daughters Joyee and Esther Loh, who now run an online channel selling mooncakes nationwide and into Singapore.

Loong Nam (隆南) split itself in two. The 1928 house relocated its heritage retail face to Chowrasta Market while opening a modern factory at Penang Science Park under the name Ha’ritage, earning GMP, ISO 22000, HACCP, halal and MeSTI certification in a single pandemic year — heritage and scale pursued as separate strategies under one family.

Tan Kim Hock (陳金福) is the cautionary version. Dr Tan Kim Hock (1924–2020), the “Dodol King” of Melaka, died in December 2020 at 96, mid-pandemic; succession passed to his sons under a new corporate entity and more than a hundred product lines continued, but no inheriting successor has yet stepped into public view. It is the cluster’s starkest reminder that a recipe outliving its founder is not the same as a brand surviving one.

The export-led houses leaned the other way. Chang Jiang (長江), having effectively invented packaged Ipoh white coffee in 1988, used the collapse in domestic demand to push outward: CEO Foong Choa Mun told Bernama in May 2024 that the brand reaches eight countries — Indonesia, Singapore, Hong Kong, Taiwan, Australia, the United States, Canada and England — at an estimated RM5 million a year, a claim lent weight by Ipoh white coffee’s 10th-of-39 placing on TasteAtlas in March 2024. Barrett’s Sarawak Laksa Paste, born from a family-recipe split after the patriarch’s death, built a diaspora-direct model on sarawaklaksa.com, couriering paste to Sarawakian expatriates from Melbourne to Glasgow who organise gatherings around each shipment.

The pattern is consistent enough to count as a finding. The houses with the deepest local roots — Kwong Tuck, Ng Kee, Loong Nam — answered the crisis by digitising distribution while keeping production exactly where it had always been. The houses with a transportable product — coffee powder, laksa paste — answered it by leaving the country. Neither group waited for the tourist trade to come back. Both read the collapse as a forcing function rather than a verdict, and the speed of their response is documented in the same public record as the collapse itself.

Around these six sit the brands a single sentence cannot do justice to but a future profile will: Kwong Bee Chun’s Taiwan-trained third generation; Cap Gajah’s cross-border soy sauce; the Sarawak kek lapis houses of Dayang Salhah and Mira; Sin Joo Heong’s Tiger Head biscuits out of Teluk Intan. None of them is a press release. Every one is a crisis decision with a name attached.

Lard, layers, and the halal line

The cluster’s deepest division is not regional but religious, and it shapes where each house can sell. Penang’s lard-based Hokkien pastry is, by design, unexportable to Malay-domestic and Gulf markets — and that constraint has become a structural advantage in its own market. Diaspora buyers in Singapore, Sydney and the United Kingdom seek precisely the unmodified original, and pay for nostalgia that cannot be reformulated.

Sarawak’s kek lapis runs on the opposite logic. An Indonesian Betawi import of the 1970s, it became by 2010 a state-protected indication and a category where Malay women built the businesses — and where a non-Muslim founder competes only by holding halal certification more strictly than her rivals. Two faiths, two distribution maps, one craft economy.

This is why the houses read as cultural definers rather than commercial units to the institutions that study them. They carry a hybrid inheritance — Hokkien craft, Peranakan sweetness, Malay technique — that makes them legible as identity long before they are legible as investments.

A handover already in motion

What makes this a moment rather than a museum is timing. The crisis did not kill the cluster; it compressed a generational handover that might otherwise have taken another decade, and that handover is happening now, in public, documented house by house.

The signals are dated and specific. Founders in their late eighties are naming successors and going online. Fourth-generation owners in their twenties and thirties — Esther Loh at Ng Kee, the next generation at Loong Nam, the Taiwan-trained heir at Kwong Bee Chun — are rebuilding distribution around e-commerce, halal-certified modern factories, and diaspora consumers. The export channels that were experiments five years ago are now proven: eight countries for Chang Jiang, a working courier model for Barrett’s, Singapore shelves for Ng Kee and Sin Joo Heong.

Tan Kim Hock’s death without a public successor documents what the undocumented version looks like; the unnamed fourth generation at Loong Nam shows how thin the documented succession pipeline still is.

A structure documented for the first time

Verified multi-generation continuity, products with provenance no private label can manufacture, and founders who have just proven they adapt rather than fold — these facts exist across the cluster, but not as a list.

The intelligence exists — in the Penang Institute’s surveys, in George Town World Heritage’s oral histories, in Chinese- and Malay-language obituaries and succession profiles, in SSM filings nobody has read across. It has simply never been assembled in one place.

Kwong Tuck has traded on Campbell Street since 1836; Cap Gajah has carried its trademark out of Kuala Krai since 1935. Both are handing the recipe down right now — to children rebuilding the trade for diaspora screens in Sydney and Singapore. But Tan Kim Hock died with no successor named in public, and Loong Nam’s fourth generation has no name on record at all. Each house that completes its handover undocumented takes generations of provenance with it — legible afterward only to whoever happened to be standing in the kitchen.