Skip to main content

Skip to main content

Kyrgyzstan: the bazaar founders nobody mapped

Kyrgyzstan's first consumer brands were built not from capital or connections but from sheep. The founders who launched Shoro in 1992 and Kulikovsky in 1991 survived four political crises, two currency collapses, and a pandemic. They are now in their sixties. No investment database has mapped what they built. No PE firm is watching.

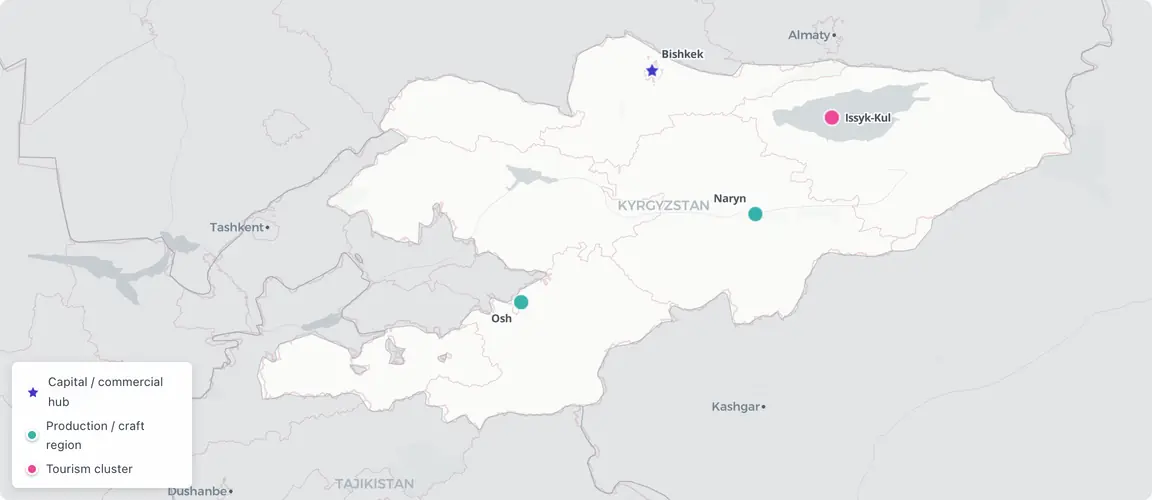

Where Kyrgyzstan's founder-owned brands cluster

The Dordoi generation, 1991–2026

In 1992, Tabyldy Egemberdiev sold four sheep and two goats — roughly two hundred dollars — to buy equipment for a small fermented-drink business in Bishkek. He had no investors, no business plan, and no bank willing to lend. What he had was a recipe for maksym, a traditional Kyrgyz drink fermented from grain, and a folding table in the Dordoi bazaar. The first eighty litres sold out in two hours. Thirty years later, Shoro controlled approximately 30 percent of the Kyrgyz soft drink market and had crossed one billion som in annual revenue. Egemberdiev did not live to see it: he died in 2015, aged sixty-four, having handed the company to his family and documented remarkably little of how it was built. No investment database has filed it. No PE firm has assessed it. The succession question remains open.

Shoro is not an isolated case. Kyrgyzstan holds an estimated fifty to ninety founder-owned consumer brands at commercial scale — across fermented foods, confectionery, dairy, honey, felt crafts, and adventure tourism — built by a generation of entrepreneurs who emerged from one of the most turbulent founding environments in post-Soviet space. Whitepaper No 1 documents the synchronized transition wave across emerging markets: reform-era founders ageing out simultaneously, with no institutional infrastructure prepared to manage the transitions. In Kyrgyzstan, the wave is not only synchronized — it has been filtered by four political ruptures that left only the most resilient brands standing.

The generation that four revolutions made

Every country’s founder cohort has a shaping mechanism. In Senegal it was a single devaluation. In Serbia it was the end of sanctions. In Kyrgyzstan it was the opposite of stability: a succession of crises that functioned less as obstacles than as tests.

The first wave launched in chaos. Between 1991 and 1998, Kyrgyzstan’s entire private economy was built on bazaar foundations — Dordoi in the north, Karasuu in the south. Capital was absent. Banking barely functioned. Founders improvised from local materials and local knowledge. Oleg and Ilvina Kulikov opened a confectionery operation in a seven-square-metre kitchen in 1991, scaling by the decade to approximately a hundred stores in three countries and two hundred product lines. The Abdullaev family launched Umut i Ko dairy in 1997, eventually reaching 70 percent export volume with Kazakhstan and Russia as primary markets. What united this cohort was not capital or connections but an extraordinary tolerance for structural risk — the capacity to build meaningful businesses in an economy that had no formal infrastructure for them.

The second filter arrived in 2005. The Tulip Revolution ousted President Akayev and suppressed commercial activity across the country for the better part of two years. Founders whose operations could absorb political uncertainty — centralised in Bishkek, with local supply chains, low reliance on state contracts — emerged intact. Those who couldn’t, didn’t. The survivors gained an NDD record that no crisis-management framework manufactured in stable conditions can approximate.

The third and most severe filter came in 2010. Ethnic Kyrgyz-Uzbek violence in Osh and Jalal-Abad killed hundreds and displaced 300,000. The southern economy collapsed. Karasuu bazaar — the commercial engine of the Fergana Valley — shut down entirely for months. For southern-based food and textile producers, the rupture was existential. The founders who rebuilt after 2010, without insurance settlements or government reconstruction funds, built again from zero. Their businesses carry a structural resilience that standard due diligence cannot quantify — and that Narrative Due Diligence is specifically designed to document.

The fourth disruption — EAEU accession in 2015 — was different in character but equally demanding. Kyrgyzstan’s entry into the Eurasian Economic Union opened Russia and Kazakhstan duty-free to Kyrgyz exports, creating significant new revenue for dairy, honey, and processed food producers. But it also removed tariff protection from Russian and Kazakh competitors, who entered the domestic market freely. Brands that had operated behind an implicit price advantage now competed directly with larger, better-capitalised EAEU rivals. The firms that survived this competitive pressure — building on product differentiation, brand equity, and the distribution networks only a Dordoi-origin founder knows how to operate — are the brands Brandmine’s methodology is designed to find.

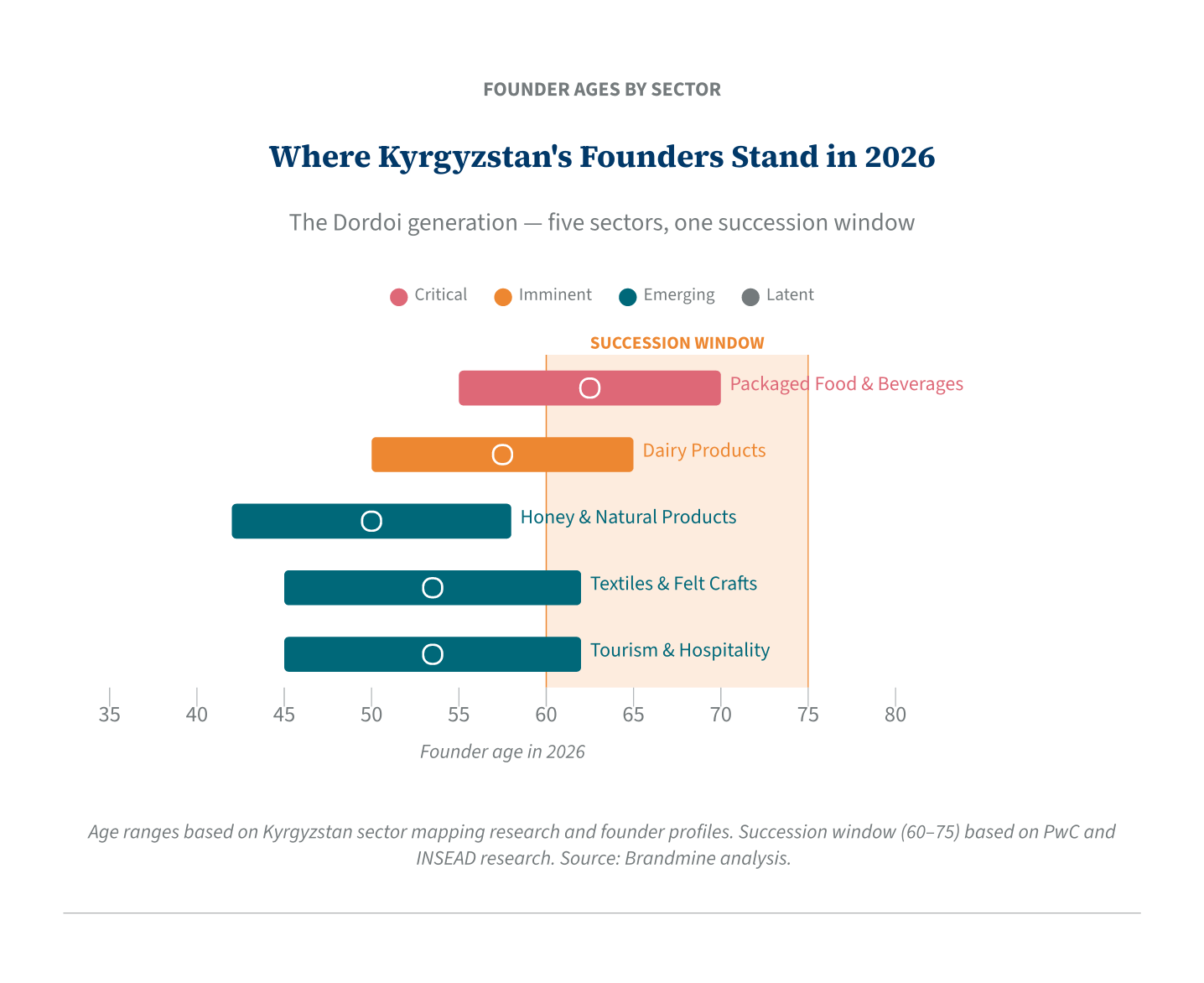

The five clusters approaching the window

Packaged food and beverages is the most urgent sector — succession at the critical threshold. The anchoring brands are the Dordoi generation itself: Shoro under the Egemberdiev family (Tabyldy died in 2015; the company continues under family control but with no documented succession structure), Kulikovsky under Oleg Kulikov’s family, and an estimated fifteen to twenty-five additional food and beverage producers that the research record suggests exist but cannot fully enumerate without scoping. The sector holds roughly 600 food-producing companies nationally — the largest single manufacturing category — with the qualifying founder-owned tier concentrated in the mid-market. Crisis documentation in this sector is unusually available: the 2023 Anti-Monopoly Service investigation of Shoro’s pricing provides a moment of institutional visibility rare for a bazaar-origin brand. A Sector Spotlight is on Brandmine’s research roadmap.

Dairy products carries imminent succession pressure. Umut i Ko — founded in 1997 by the Abdullaev family and built to dominant regional export position — is the sector’s anchor case, complicated by the 2023 arrest of co-owner Zhurat Abdullaev in a still-unresolved legal matter that has disrupted operations at Kyrgyzstan’s most documented dairy exporter. The crisis arc is extraordinary NDD material: a business that survived the 1998 currency shock, the 2005 revolution, the 2010 violence, and EAEU competitive pressure is now navigating a founder-level legal crisis. Whether the business survives in its current form depends on succession dynamics that are not visible from any public database. Alongside Umut i Ko, approximately six to twelve additional dairy producers at commercial scale operate across the country, with founder age bands clustering at 50–65.

Honey and natural products is Kyrgyzstan’s most globally distinctive export niche. Tien Shan alpine honey — produced in high-altitude conditions that no temperate-region competitor can replicate — has accumulated more than forty-three international awards and found export channels to China, the United States, and the EU. Honey exports grew 44 percent year-on-year in the first half of 2023, with China absorbing 43 percent of volume and the United States taking 12 percent. The founder cohort here is younger — primarily 2000–2015 wave, with founders aged 42–58 — placing succession urgency at emerging rather than critical. But the raw-to-brand arc (apiary operations formalised into certified export brands over the course of a decade) is exactly the kind of transformation story that institutional buyers have shown willingness to pay for, as similar moves in Ethiopian coffee and Ethiopian honey have demonstrated. An estimated ten to eighteen qualifying brands exist at commercial scale.

Textiles and felt crafts is the sector most likely to be underestimated by a surface survey. The estimated pool of eight to fifteen qualifying brands carries a conservative flyby multiplier: prior Brandmine experience suggests this tier is five to ten times understated at reconnaissance depth. Tumar Art Group — founded in 1998 by three women, producing up to ten thousand pairs of felt footwear per month with approximately two hundred maker-partners, with export reach via eBay and Etsy — is the anchor case. The sector is UNESCO-linked, women-founder-heavy, and connected to a pastoral supply chain that runs through Naryn and Talas regions that no investor database has mapped. Cultural durability is not the investment argument; crisis resilience and export credentials are. The founders who built certified artisan brands through the 2005 and 2010 disruptions while sustaining international buyer relationships did so without any institutional support — and the documentation of how they did it exists in USAID programme reports, UN News coverage, and industry association records that no single investor has assembled.

Tourism and hospitality sits at the edge of the qualifying threshold. Vladimir Komissarov founded ITMC in 1989 — the oldest private tour company in Kyrgyzstan, with more than 350 documented high-altitude ascents and twelve peaks above 7,000 metres. The Danichkin family has operated Kyrgyzland from a guesthouse on the south shore of Issyk-Kul since 1997. Abdyrazak Nyshanov’s Pamir Nomad yurt camp reaches approximately fifteen hundred tourists per season and has visible second-generation involvement. The challenge for this sector is the $5M revenue threshold: many operators sit below it, and verification requires direct research. The broader adventure tourism boom since 2010 — Kyrgyzstan now appears regularly in Lonely Planet, Explore, and international trekking media — has created a cluster of twelve to twenty potentially qualifying operators whose succession status is invisible to any institutional observer.

What the investor base cannot see

The structural feature that makes Kyrgyzstan most valuable as an intelligence target is not the quality of its founders — though that quality is real — but the absence of any institutional mechanism to find them.

Every identifiable institutional investor active in Kyrgyz consumer brands is a development finance institution. The Russian-Kyrgyz Development Fund had directly funded 79 projects totalling $209.7 million as of 2022, with a further $207.2 million on-lent through commercial banks supporting 3,107 SME projects. IFC funds infrastructure and agribusiness. EBRD operates through local banking channels. None of these institutions is conducting consumer brand succession intelligence. None is asking whether Shoro or Kulikovsky or Umut i Ko have succession structures in place. They are not designed to ask those questions.

In July 2025, IFC approved a loan of up to $10 million to Adal Azyk LLC — a sausage and poultry producer occupying roughly 55 percent of the Kyrgyz sausage market — and CEO Myrzabek Orumbaev called it “a significant milestone.” It is a milestone, but not primarily because of the capital amount. It is a milestone because it marks the first documented instance of a major institution naming a Kyrgyz consumer brand as an investment target.

The 2010 ethnic violence produced a geographic split in the Kyrgyz brand landscape that further complicates any surface-level assessment. Bishkek-centred brands have a reasonable documentation record: Forbes.kg founder profiles, AKIpress coverage, Tazabek business press. Southern brands — built in the Osh and Jalal-Abad economy, sourcing from the Karasuu bazaar and Fergana Valley supply chains — are severely under-documented. The Karasuu economy, which before 2010 was processing and distributing food products across the Fergana Valley, produced a layer of founder-built businesses that survived the violence, rebuilt their distribution networks, and continued operating for fifteen years in conditions that precluded any formal investor documentation. These brands survived more disruption than their Bishkek counterparts, which makes them more valuable as NDD targets, and they are precisely the ones that any investor working only from Russian-language business press will not find.

Succession in Kyrgyz family business follows an informal but consistent pattern: intra-family transfer, typically to an adult son or daughter who has been working inside the business, with no codified process and no outside advisors. There is no family business advisory sector in Kyrgyzstan, no succession-planning culture in the banking system, and no PE fund that has experience structuring these transitions. The transfer happens — or doesn’t — based on whether the founder’s family has the capacity and the will to continue. When it doesn’t happen, the business typically closes or is absorbed into a larger Kazakh or Russian food group at a fraction of its intrinsic value. That structural absence is the intelligence gap: no institution has documented what these brands built or what they survived.

The bazaar founders the databases never reached

When IFC structured its Adal Azyk loan in 2025, the due diligence focused on financials, market share, and management depth — the standard DFI checklist. It did not ask how CEO Myrzabek Orumbaev built to 55 percent market share without institutional capital, what he did when the 2010 violence disrupted his supply chain, or whether he has a succession plan. That is not what DFI due diligence is for.

The investment intelligence gap in Kyrgyzstan is not the absence of companies. It is the absence of documented founder narratives — the account of how these businesses were built, what they survived, and what that survival means for the next owner. The Egemberdiev family launched Shoro from four sheep and two goats and built to national category dominance in thirty years. Tabyldy Egemberdiev died in 2015 without that account being assembled for any capital-markets audience. The family continues. The crisis record — 1998, 2005, 2010, 2015 EAEU — sits in Forbes.kg archives and AKIpress files that no international investor has synthesised.

The Kulikov family is still building. Oleg Kulikov’s seven-square-metre kitchen is now a hundred-location confectionery chain. The NDD record of how that happened is assembling itself, event by event, in Kyrgyz business press — in a language that no investor working from English-language intelligence sources will read.

Sixty-four was the age Tabyldy Egemberdiev died. The founders who built alongside him are approaching that age now. The intelligence that explains what they built — and what it is worth to whoever acquires it next — does not exist in any form accessible to the buyers who would pay for it.