Skip to main content

Skip to main content

Kenya: The Invisible Wave

Kenya's founder cohort built consumer brands through multi-party liberalisation, two election crises, a drought, and COVID-19 -- then distributed them across East Africa without a single institutional investor noticing. Only 17% have succession plans. The wave is invisible. That will not last.

Kenya's Founder-Owned Brand Geography

Transformation Arc

Kenya has the strongest English-language business press in Sub-Saharan Africa outside South Africa. Business Daily Africa, Nation Media Group, How We Made It In Africa, and Forbes Africa have documented Kenyan founder-owned consumer brands since the liberalisation era of the early 1990s. The coverage is extensive, digitised, and searchable. Yet when Brandmine’s sector mapping team evaluated Kenya as a transition wave candidate, the finding was not a shortage of intelligence – it was a structural blindspot in how that intelligence is consumed. Every brand is visible in Nairobi. None of them appear in PitchBook, Bloomberg, or any institutional investor pipeline.

The wave that created this founder cohort is thirty-five years old. It is now arriving at the succession window. Only 17% of Kenyan family businesses have documented succession plans. The demographic mechanics driving this pattern – the global founder transition wave first documented in Brandmine’s founding research – are not unique to Kenya. But Kenya represents one of the clearest single-country expressions of it.

The single reform wave and its two layers

Only 17% of Kenyan family businesses have documented succession plans.

Kenya’s founder cohort is structurally different from Argentina’s serial-crisis builders or Russia’s voucher-privatisation opportunists. It was created by a single decisive event – the 1991 repeal of Section 2A and the return to multi-party politics – and the economic liberalisation that followed. Price controls were lifted, import licensing was dismantled by 1994, foreign exchange controls were removed by 1993. The founders who launched consumer businesses in this window did so on genuinely open terrain for the first time in Kenya’s post-independence history.

That wave has two distinct cohort layers, now compressing into the same transition window simultaneously.

The first layer formed during the early liberalisation era, from 1991 to 1997. Kimani Rugendo, who lost the Lang’ata parliamentary seat to Raila Odinga in 1992, pivoted immediately to FMCG manufacturing. His Kevian Kenya – Afia juice, Mt. Kenya water, Pick N Peel – was built entirely from personal savings, bootstrapped to become East Africa’s leading juice manufacturer without a single round of institutional capital. Rugendo is now estimated to be in his late sixties. No succession plan has been publicly disclosed. In the same era, Kim Fay East Africa (est. 1991) built a 251–500 person tissue paper and household products operation whose founder identity remains undisclosed – the company is visible in every Kenyan supermarket, invisible to every institutional investor.

The second layer formed during the Kibaki era, from 2003 to 2010. When Mwai Kibaki’s election in December 2002 delivered Kenya’s first peaceful democratic transfer of power, GDP growth accelerated from 0.6% to 7% by 2007. A new cohort of consumer entrepreneurs launched in food, beverages, hospitality, and services. These founders are now aged 48 to 58 – at the leading edge of the succession window. The 2010 constitution deepened the wave, as devolution opened 47 county markets and M-Pesa’s maturation enabled distribution models that required no institutional capital at all.

The Indian-Kenyan diaspora – approximately 100,000 people, recognised as Kenya’s “44th tribe” in 2017 – adds a third dimension. This community controls outsized manufacturing and FMCG share through patriarchal family structures now in second or third generation transition. These are not founder-owned brands in the strict Brandmine definition, but they represent the most acute succession dynamics in the market: family enterprises at $10M–$100M+ revenue, transitioning between generations without formal governance structures, in a diaspora community where the succession conversation is actively suppressed.

Where the transition pressure is highest

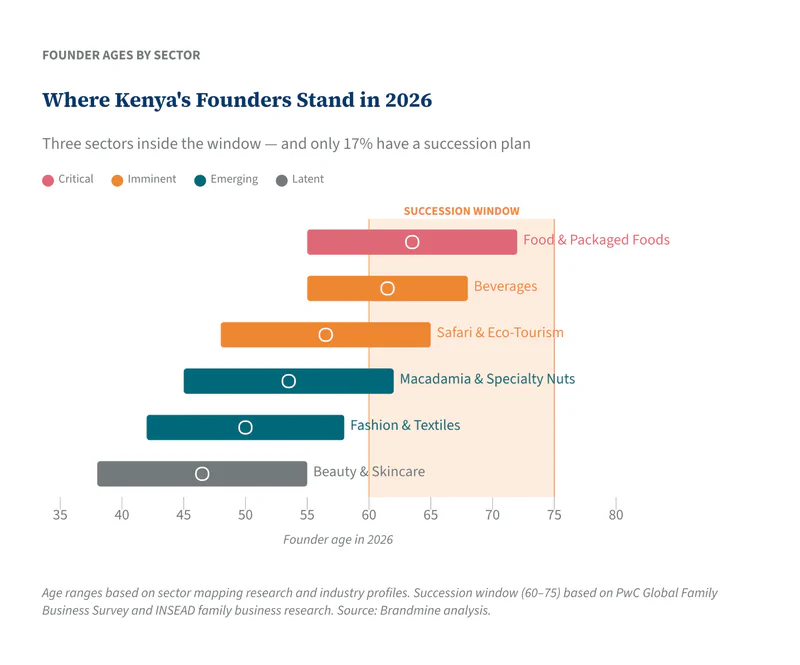

Brandmine’s sector mapping identified twelve candidate consumer sectors in Kenya. Six show meaningful founder-owned brand activity at commercial scale. Three are already inside the succession window.

The sector with the most acute single crisis on record

Kenya’s beverages sector – independent brands outside the EABL/Diageo duopoly – contains an estimated 8 to 15 founder-owned brands at commercial scale. Founder ages run 55 to 68. Succession urgency: imminent. The anchor case is Keroche Breweries.

Tabitha Karanja founded Keroche in Naivasha in 1997 with personal savings and no political capital – a decision that put her in direct competition with a government-backed monopoly that spent decades trying to remove her. She survived EABL’s market pressure, regulatory attacks, and KRA tax claims totalling over KSh 22 billion filed in 2023. She now simultaneously serves as Nakuru County Senator. The compound crisis documentation – monopoly pressure, tax warfare, COVID, and political life – makes Keroche one of the richest Narrative Due Diligence subjects in all of Brandmine’s emerging market coverage.

In December 2022, her co-founder and husband Joseph Karanja died in a road accident. Tabitha is now sole principal of a brewery with estimated peak revenues of KSh 8–10 billion, no institutional capital on the cap table, and no disclosed succession arrangement. She is 61 years old. This is not a succession risk. It is a succession event that has already begun.

The sector where the wave is richest but the pool is smallest

Kenya’s food and packaged goods sector – founder-owned FMCG manufacturers outside the multinationals – contains an estimated 15 to 25 brands at commercial scale, with an estimated actual pool of 50 to 100 when fully researched. The NSE/Asoko Insight study identified over 500 East African family-owned businesses at $5M+ annual turnover, with food and beverages ranked second only to industrial manufacturing. Founder ages cluster 55 to 72, driven by the Indian-Kenyan diaspora cohort in the upper range. Succession urgency: critical.

The signal that confirmed sector valuations came from Kenafric Industries in January 2025: private equity firms Amethis and Metier seeking exit from their 40% stake at a $100M+ valuation. Kenafric is a third-generation Chedda/Shah family business – not a first-generation founder-owned brand in the Brandmine definition, but the exit signal confirms what buyers will pay for well-documented Kenyan consumer FMCG brands. The first-generation founder-owned brands in this sector are priced at a discount to Kenafric precisely because they have never been institutionally valued. That discount closes the moment the first comparable transaction completes.

The sector’s flagship invisible brand is Norda Industries, makers of Urban Bites premium potato crisps, Ringoz, and Bitez – distributed across East Africa with celebrity endorsement partnerships and no evidence of institutional capital. The founder is undisclosed. The revenue is estimated in the mid-single-digit millions. The brand is in every East African supermarket and on every Kenyan social media feed. It does not exist in any investor database.

The sector where the NDD material is deepest

Kenya’s safari and eco-tourism sector contains an estimated 10 to 20 founder-owned hospitality brands at commercial scale – single lodge operations running $1–4M, multi-property collections running $5–20M+. Sixty to seventy per cent of Kenya’s premium safari lodges remain founder or family led. Succession urgency: imminent.

The Safari Collection – Giraffe Manor, Sala’s Camp, Sasaab, Solio Lodge – is the most prominent example. Mikey and Tanya Carr-Hartley, a fourth-generation Kenya conservationist family, describe their six-property group as “the last Kenyan-owned, Kenyan-run safari collection.” Revenue is estimated at $10–20M+. No institutional capital. Founder age approximately 52. No disclosed succession plan.

Governors’ Camp Collection tells a different story: a live generational succession, forty years in the making. Aris and Romi Grammaticas founded their first Maasai Mara camp in 1972. Their children – Dominic, Justin, Damian, and Ariana – now run seven-plus properties across Kenya and Rwanda. The transition is happening. The question is whether it is happening on institutional terms or on family terms, and what the governance gaps look like from the outside.

Angama, founded by Steve and Nicky Fitzgerald above the Maasai Mara escarpment, crystallised the sector’s key-person risk acutely: co-founder Steve Fitzgerald died, and the CEO succession from founder family to professional management created visible instability before stabilising. In a sector where every brand is built on personal relationships – with conservancies, with wildlife organisations, with high-net-worth travellers who chose the brand because they trusted the founder personally – founder death or exit without succession planning is a category-specific existential risk.

The NDD material generated by the 2007–08 post-election violence alone is extraordinary. Kenya’s tourism GDP growth collapsed from 7% to 1%. Every safari operator in the Mara, Laikipia, and Samburu documented survival strategies – empty camps, cancelled seasons, emergency diversification. The English-language press archived it all. For an institutional buyer evaluating crisis resilience in an East African hospitality asset, this is the richest single source of documentary evidence in the continent.

The sectors in formation

Three additional sectors warrant monitoring without immediate action. Macadamia and specialty nuts (an estimated 6–12 founder-owned brands, founders aged 45–62, succession urgency: emerging) has standout candidates – Jungle Nuts specifically – but the pool is small and the export dependency creates valuation complexity. Fashion and textiles (an estimated 10–20 founder-owned designers and textile brands, founders aged 42–58, succession urgency: emerging) is building but has not yet reached the $5M+ revenue threshold consistently. Natural beauty and skincare (the youngest cohort, founders aged 38–55, succession urgency: latent) is the Silicon Savannah era’s most visible consumer category but remains pre-succession for the foreseeable window.

Why this wave is invisible

The invisibility of Kenya’s founder-owned consumer brands to institutional capital is not a function of press coverage – which is excellent – nor of market size – which is the largest in East Africa. It is a structural consequence of how institutional investors approach African consumer markets.

The active institutional investors in Kenya – Catalyst Principal Partners, Centum, AfricInvest, Actis – drove $5.83 billion in 2025 deal flow. They overwhelmingly target corporate-scale assets: $50M+ revenue, existing governance structures, clean cap tables. The $5–50M founder-owned consumer space falls below their minimum ticket and above their tolerance for governance complexity. The PE firms that scoped Kenya’s coffee sector in the 2010s comprehensively harvested it – Java House, Artcaffe, and Dormans all transitioned to institutional ownership. Zero qualifying founder-owned coffee brands remain. The PE playbook ran its course in the most visible sector and moved on. The less visible sectors – food processing, beverages, safari lodges, macadamia – were never in the playbook.

The Indian-Kenyan community’s resistance to external visibility compounds this. The diaspora’s strongest FMCG brands are identifiable by product – available in every Nakumatt and Naivas outlet – but founder profiles are deliberately kept out of the press. Business Daily Africa covers Kenyan-African entrepreneurs with enthusiasm. Indian-Kenyan family businesses appear in coverage only at the moment of a succession dispute, a tax controversy, or a PE exit. The intelligence gap is not accidental. It is culturally maintained.

The EAC common market is the multiplier that makes this sector intelligible. Kenyan brands distributing to Uganda, Tanzania, Rwanda, Ethiopia, and South Sudan are operating at a scale that their Kenya-only revenue does not reveal. Kevian Kenya’s reach across East Africa, Keroche’s distribution network built despite EABL’s market pressure, the Safari Collection’s regional reputation – these are brands with EAC-wide footprints that no single country’s reporting captures. The compound revenue picture is only visible to someone who has mapped the full EAC distribution chain, not just the Nairobi filing records.

The window and the documentation that already exists

Unlike Russia, where the post-1991 founder cohort operated in an environment of deliberate opacity, or Iran, where sanctions create structural research barriers, Kenya’s founder-owned consumer brands are documented. The wave is not hidden. It is simply not aggregated in a form that institutional capital can act on.

The Business Daily Africa archive. Nation Media Group’s decades of founder profiles. How We Made It In Africa’s systematic coverage of East African entrepreneurship. Forbes Africa’s Kenya features. The Startup Grind Nairobi podcast catalogue. LinkedIn profiles where Kenyan business leaders are more active than almost any comparable cohort in Africa. The raw material for Narrative Due Diligence on Kenya’s founder-owned consumer brands is the most complete in Sub-Saharan Africa. It has never been synthesised into the form that a family office, a PE fund, or a strategic acquirer can use.

The crises that generated this material are well-documented and distinct. The 1997 El Niño floods. The 2007–08 post-election violence – the single most comprehensively documented commercial disruption in East African history. The 2011 Horn of Africa drought. The 2017 election crisis. COVID-19’s collapse of tourism revenues. The 2023 Gen-Z protests and cost-of-living contraction. Each event produced a layer of crisis response documentation – founders who redirected supply chains, who kept staff employed without revenue, who rebuilt distributor relationships from nothing. The accumulated record spans three decades of documented resilience. No other East African market produces this depth of source material.

The succession window opened in 2023 for the earliest liberalisation founders. It will remain open through 2032 as the Kibaki-era cohort matures. The Indian-Kenyan diaspora succession dynamics are already in motion and will accelerate as third-generation family members educated abroad either return to take over or sell to outsiders. The combination – three cohort layers entering transition simultaneously, across six sectors with documented crisis histories, in a market with Africa’s strongest English-language business press – makes Kenya the most actionable single country in Brandmine’s East and Central Africa coverage.

What disappears when a founder exits without a plan is not just a brand. It is the distributor relationships built over thirty years of navigating EAC trade barriers. The supply chain redundancies assembled after the 2007 violence. The conservancy partnerships that took a decade of trust-building to establish. The consumer loyalty that lives in the founder’s face, not in the company’s org chart. By the time these brands surface through conventional channels – if they ever do – the founders who carry this knowledge will have retired, sold to a competitor, or simply wound down operations.

Kenya’s founder-owned consumer brands are invisible. The documentation to make them visible already exists. The window to act on it is open.