Skip to main content

Skip to main content

Jordan: Two Founder Cohorts, One Succession Moment

Jordan holds two distinct founder cohorts entering the succession window simultaneously — Palestinian merchant families who rebuilt their brands in exile after 1948, and an IMF-reform generation that built from 1989 onward. No investor database tracks either wave. Saudi acquirers already know this.

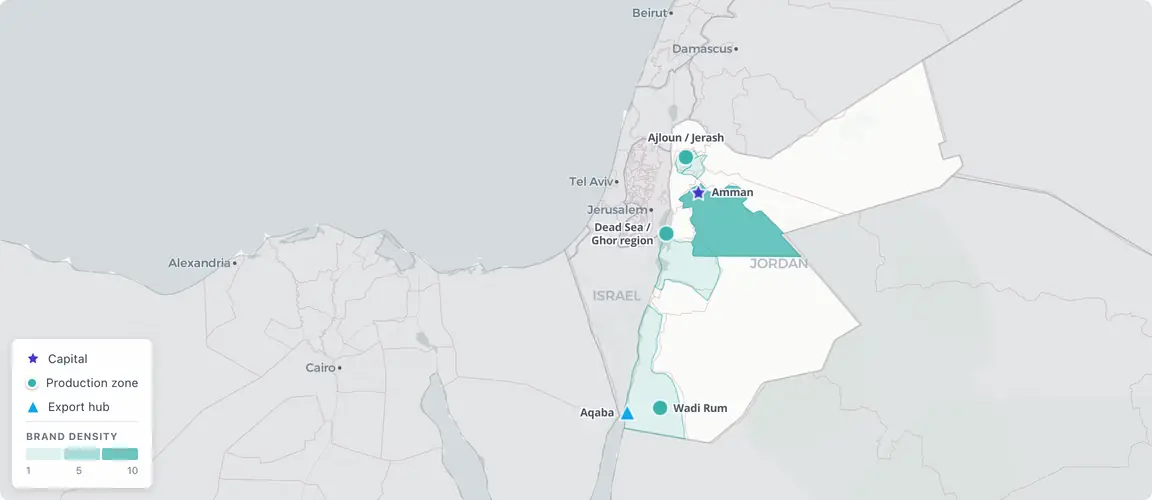

Jordan's founder-owned brand ecosystem

The twice-displaced generation, 1948–2024

In October 2023, SADAFCO — one of Saudi Arabia’s largest food companies — partnered with Kasih Food to distribute its Mezete brand into more than 20,000 Saudi retail outlets. Kasih Food was founded in 1926. Its CEO, Khaled Kasih, is the fourth generation of the family. The deal proved something that no Bloomberg terminal or PitchBook database could have surfaced: Saudi strategic buyers are actively identifying, evaluating, and selecting Jordanian consumer assets — and they found this one without institutional investors noticing.

Kasih is not an isolated case. Jordan holds two distinct founder cohorts that are both entering the succession window simultaneously, with no investor infrastructure watching either of them. The first cohort was created not by economic reform but by displacement: Palestinian merchant families who rebuilt their commercial lives in Amman after 1948 and 1967. The second was created by the IMF stabilization program of 1989 and the trade liberalization that followed through WTO accession and a US free trade agreement. Both cohorts built durable consumer brands. Both are now reaching the transition point. And the institutional intelligence required to act on this moment does not yet exist in English.

The mechanics of a double wave

Conflicts of interest, poor teamwork, internal rivalry, and unstable management tenure represent the key issues facing current exporting entities.

Jordan’s succession wave has a shape unlike almost any other market Brandmine maps. Most countries present a single founding cohort aligned with a single reform moment: Russia’s voucher privatization, Vietnam’s Doi Moi, Mongolia’s 1990 democratic revolution. Jordan presents two distinct waves with different origins, different sectors, and different urgency levels — but both cresting at roughly the same time.

The older wave is the Palestinian merchant diaspora. Habibah Sweets was founded in Jerusalem in 1947 and relocated to Amman in 1951. The Zalatimo family’s sweets business, tracing roots to Ottoman-era Jerusalem, established in Amman around the same time. The Masri family’s Nabulsi soap-making tradition arrived after 1967. These families came with craft knowledge, commercial instincts, and the specific determination of founders who had lost one home and were building another. Their businesses — concentrated in Levantine sweets, specialty foods, and artisan production — are now operated by second and third generations whose founders or senior operators are 65 to 75 years old. Zalatimo’s 5th-generation chairman, Abdallah Zalatimo, is now in his mid-sixties; the 6th generation is already entering the business. Habibah’s Hani Habibah runs the Amman flagship. The succession is underway in real time.

The IMF-reform wave runs roughly ten years younger. Jordan’s 1989 structural adjustment and subsequent trade liberalization created the conditions for a new generation of consumer-facing companies built between 1989 and 2004. The Dead Sea cosmetics cluster is the clearest example: Bloom Dead Sea Life was founded on June 28, 1993 by chemical engineer Elham Ziadat, who is still operating. Jordan Co. for Dead Sea Products (La Cure brand) followed in 1994, Jordan Integrated in 1995, Rivage Natural Dead Sea Minerals in 1998. All four were founded within five years of each other; all four founders are now 58 to 72. A fifth-year window of founding has produced a five-year window of succession pressure, arriving now.

The Dead Sea cosmetics example also illustrates why the geographic exclusivity matters. Dead Sea minerals cannot be sourced from anywhere else. The specific mineral composition — the salinity, the magnesium, the potassium concentrations — is a function of geology that no competitor can replicate. The brands built on this foundation have a structural advantage that has nothing to do with marketing. It has everything to do with the fact that their founders found the right place, at the right moment, and built something durable before anyone was paying attention.

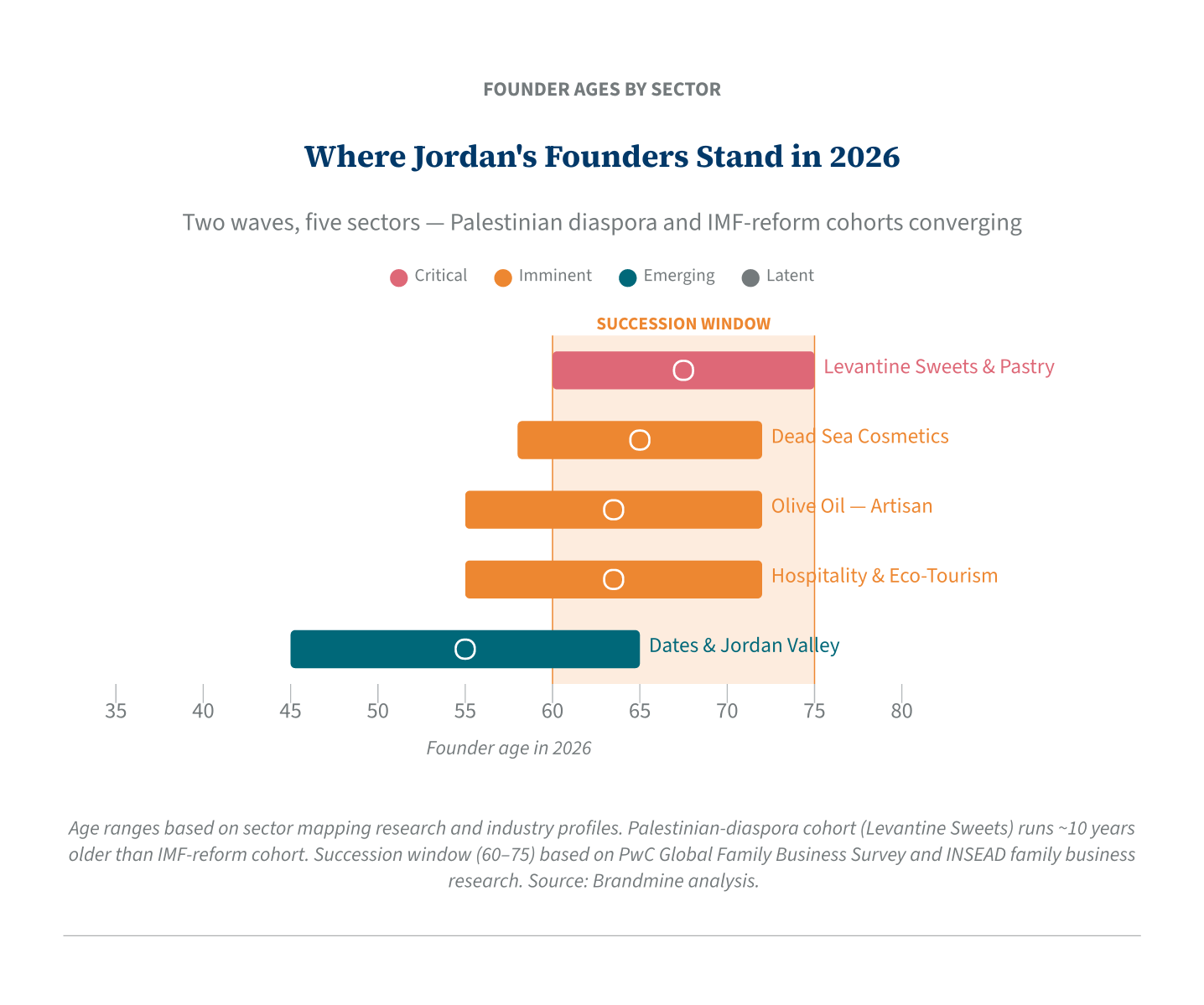

Five sectors, two urgency bands

Levantine sweets and pastry sits at the top of Jordan’s succession urgency table. The estimated pool of 8 to 12 founder-owned brands at commercial scale has a founder age band of 60 to 75 — the heart of the succession window — and many of them are already in the process of generational transfer. The Palestinian Nablus-origin heritage of brands like Habibah and Zalatimo is not merely aesthetic. It is a provenance story — displacement, rebuilding, survival, expansion — that provides the narrative foundation for premium positioning in Gulf and Western markets. Zalatimo’s placement in 230 Walmart Supercenters is not an accident. It is the result of a family that spent seventy years building distribution before anyone in institutional finance was watching. A Sector Spotlight is in preparation.

Dead Sea cosmetics and mineral skincare presents a different profile: imminent rather than critical urgency, but with a geographic exclusivity that no other market can match. The 1993 to 1998 founding cluster produced 10 to 15 founder-owned brands now entering the succession window together. Gulf and European distribution is already proven — La Cure exports to 53 or more countries; the Aqaba Special Economic Zone provides export infrastructure. The state-owned Numeira (an Arab Potash subsidiary) occupies the industrial mineral extraction segment but has largely avoided the consumer cosmetics layer, which remains founder-owned. A Sector Spotlight is in preparation.

Olive oil — premium and artisan requires more caution than the other top sectors but has a distinct signal. Jordan ranks among the world’s top ten olive-producing nations, with 20 million trees and an industry generating roughly $141 million annually. The Ajloun and Jerash foothills have produced a consumer-brand layer — Majdal Olive Oil, Levant Liquid Gold, Il Siru, the Bedouin Company — on top of a commodity export industry. What makes this sector legible for Brandmine is a public admission from the Jordan Olive Products Exporters Association: “conflicts of interest, poor teamwork, internal rivalry, and unstable management tenure represent the key issues facing current exporting entities, and they are the reason behind their failure.” JOPEA is diagnosing succession failure in the language of trade associations. The intelligence is explicit; it simply has not been assembled. The revenue floor ($5 million minimum) requires verification at scoping — many olive oil operators are commodity exporters, not consumer brands.

Hospitality and eco-tourism in Wadi Rum presents the best narrative material of any sector in Jordan, and moderate commercial fit. The ~40+ Bedouin camp operators who built after UNESCO’s 2011 World Heritage inscription form a distinct succession cohort — founders 55 to 72, several with sons already managing operations. Captain’s Desert Camp (Abdul-Fattah Suleiman) is the clearest example of next-generation stewardship already underway. The crisis record is exceptional: Arab Spring tourism collapse in 2011, COVID closure through 2020–21. Every surviving operator is crisis-tested in ways that make for authoritative Narrative Due Diligence. Commercial fit is moderate because hospitality businesses are harder to value and transact than food brands. The intelligence value, however, is disproportionate.

Specialty food — dates and Jordan Valley produce sits in the emerging category: founders 45 to 65, Gulf export footprint strong, but the primary succession wave has not yet arrived. Kareem Dates, Sedra Dates, Jordan River Dates, and Yaqout Dates all export Medjool and Barhi varieties to Gulf markets. This sector’s succession pressure opens in five to eight years, giving intelligence work here a longer runway than the top-tier sectors.

What the double wave produces

Jordan’s double succession wave creates a structural complication that most emerging-market frameworks do not account for. In a single-wave country, the succession clock is relatively uniform: one cohort, one age band, one urgency level. In Jordan, the Palestinian diaspora cohort is a decade older than the IMF-reform cohort, which means the urgency is already differentiated by sector. Levantine sweets founders are exiting now; Dead Sea cosmetics founders are approaching the window; dates and Jordan Valley produce founders are five to eight years away. An investor who treats Jordan as a single succession story will misallocate attention. The sectors require prioritization, not aggregation.

The cultural default compounds this. Jordan’s commercial culture defaults strongly toward son-inheritance and continued family management over professionalization or institutional capital. This is not unique to Jordan — it appears across most of the markets Brandmine covers — but in Jordan it has a specific texture. For the Palestinian merchant families, passing the business to the next generation is not merely a succession decision; it is a statement about continuity, identity, and the permanence of what was built in exile. Habibah’s 1966 brothers’ dispute — the schism that split the company into two distinct branding lines — is the cautionary tale that every family in this cohort knows. Without formal governance, family businesses resolve conflict through rupture.

There is also no institutional infrastructure to absorb or intermediate these transitions. No private equity firms actively target Jordanian consumer brands. No family business advisory sector has scaled to the commercial density these cohorts represent. The succession events that are happening — Zalatimo’s generational transfer, Rivage’s next-generation co-ownership since 2014, Captain’s Desert Camp’s son stepping into management — are happening without professional support. The ones that go wrong will go wrong quietly.

A further complication is Gulf market dependency. For most commercial-scale Jordanian consumer brands, a reported 40 to 60 percent of revenues flow through Saudi Arabia and the UAE. This is not a weakness — it is the structural reason SADAFCO identified Kasih Food as a priority acquisition target. Gulf distribution relationships built over decades by Jordanian founders represent exactly the market access that Saudi strategic buyers want to acquire. But the dependency also concentrates risk: a brand whose founder exits without a succession plan does not merely lose domestic continuity; it risks losing the Gulf distribution relationships that were built on personal trust, introductions, and decades of founder-to-buyer interaction. The brand may survive; the distribution may not.

This is the intelligence gap that matters for Gulf-oriented investors. It is not enough to know that these brands exist at commercial scale. The question is which ones have founder-built Gulf distribution networks that are durable enough to survive a transition — and which ones will see those networks atrophy the moment the founder steps back. Answering that question requires Narrative Due Diligence: documenting how the founder built the relationship, what crises tested it, and whether the next generation has been introduced into those networks already. None of this information appears in any database. It exists in Arabic-language business press, in trade association records, in the background of the press photographs that ran in regional food industry publications when the deals were signed.

Before the next transaction

The 2015 Syrian refugee crisis added a further layer of complexity that most market analyses ignore. Jordan absorbed approximately 1.3 million Syrian refugees, reshaping labor pools in food processing and hospitality. USAID’s LENS program documented roughly 11,000 home-based food businesses emerging from that community — an informal competitive layer that pressures established founder-owned brands in za’atar, condiments, and traditional foods. This is not primarily a threat; it is a signal about the depth of food production knowledge distributed across Jordan’s population. The informal layer and the formal brand ecosystem exist in parallel, with very different succession dynamics.

SADAFCO’s October 2023 Kasih deal did not happen because SADAFCO had access to a proprietary database of Jordanian consumer brands. It happened because Saudi acquirers with sector knowledge and Gulf distribution relationships were already evaluating the landscape — and they found a target that met their criteria before any institutional intelligence platform had assembled the case.

That is precisely the condition Brandmine’s sector mapping documents. The brands exist. The succession pressure is real. The Gulf acquisition appetite is demonstrated. What does not exist is the systematic intelligence — who the founders are, what crises they survived, which sectors have the deepest commercial-scale pools, which succession events are already in motion.

Jordan’s Levantine sweets families built brands that crossed from Jerusalem to Amman under displacement and survived for three generations. Some of them reached Walmart. Others are still building. The question the SADAFCO deal has now made concrete is whether the third and fourth transitions happen under the terms a prepared seller would accept, or under the terms an unprepared one does.

The intelligence to answer that question is being assembled for the first time.