Skip to main content

Skip to main content

Côte d'Ivoire: The Value-Added Generation

Côte d'Ivoire produces 40% of the world's cocoa and more cashew than any other country. The founders who built the consumer layer above that raw material wealth survived a decade of civil war, rebuilt, and are now entering a succession window with no institutional investor paying attention. That ends now.

Where Côte d'Ivoire's brands cluster

The value-added generation, 2002–2024

Côte d’Ivoire produces roughly 40 percent of the world’s cocoa and more cashew nuts than any other country on earth. The infrastructure to turn those commodities into branded consumer goods — the processing lines, the packaged SKUs, the cold-chain logistics networks connecting Abidjan to Kinshasa — was built, almost entirely, by a generation of Ivorian founders who launched businesses during the post-devaluation recovery of the 1990s, survived a decade of civil war between 2002 and 2011, and emerged into a reconstruction era whose growth story has been reported in French, in Jeune Afrique and Agence Ecofin, and essentially nowhere else.

The brands they built are sold across West and Central Africa. One competes directly with Danone in infant cereals and distributes across Cameroon, Senegal, Togo, and the DRC. Another processes 15,000 tonnes of cashew nuts annually into branded retail SKUs sold in Abidjan’s modern-trade supermarkets. A third dressed Nelson Mandela and heads of state across the continent, and runs twenty boutiques in seven countries. None of them appear in PitchBook, Bloomberg, or any institutional investor pipeline. The facts are all on the record — in French, scattered across a decade of West African business press. No one has assembled them into a picture an investor could act on. Whitepaper No 2 makes the structural case for why; Côte d’Ivoire is its West African test case.

The miracle, the fire, and the generation between

In 2024 we are processing 341,000 tonnes of cashew — more than four times what we processed ten years ago.

To understand who built these brands and why they are simultaneously approaching succession in 2026, you need the country’s layered economic history — because Côte d’Ivoire produced not one founding wave but two, separated by a decade of armed conflict that reshaped everything between them.

The first wave emerged from what Ivoirians call the Ivorian Miracle: the Houphouët-Boigny era from independence in 1960 through the early 1980s, when cocoa and coffee revenues sustained one of sub-Saharan Africa’s highest per capita incomes and a first generation of entrepreneurs built the country’s initial consumer businesses — textile ateliers, fashion houses, early food processors — with state encouragement and commodity revenue behind them. Aimé Pathé Ouédraogo opened his first Treichville atelier in 1977 in this milieu, dressing the political class and regional elites at a moment when Abidjan was West Africa’s most modern city. That cohort is now aged 65 to 80 or older. Pathé’O is 76.

The second wave was created not by abundance but by adjustment. The January 1994 devaluation of the CFA franc halved Ivorian purchasing power overnight, but simultaneously doubled commodity prices in local currency. Agricultural processing — transforming cashew, cocoa, shea, and grain into packaged consumer goods — suddenly became viable at small industrial scale. Marie Diongoye Konaté founded PKL Protéines Kissèe-La in 1994 with 400,000 to 600,000 CFA francs of personal capital, building from a kitchen to a company that would eventually rank second in Ivorian infant cereals behind Danone. Massogbé Touré Diabaté incorporated SITA the year of Côte d’Ivoire’s first coup, in 2000, having spent the previous two decades building the cashew cooperative that would anchor it. This devaluation-era cohort is now aged 50 to 68.

Between these two waves came the decade of fire. From 2002 to 2011, Côte d’Ivoire endured a rebellion that split the country geographically, two coups, and a post-electoral crisis that produced open urban warfare in Abidjan before Ouattara was installed with French and UN military support. For founders already operating in 1994, this decade was not merely a disruption — it was an existential test. PKL survived the Probo Koala toxic waste dumping of 2006, which directly contaminated its facility, compounded by a simultaneous land dispute and the ongoing electoral violence. SITA’s cashew cooperative was based in the rebel-held north, navigating ten years of supply chain management across a live conflict zone. Every founder who emerged from 2011 still operating carries a crisis archive that no database has indexed — and that exists only in French.

This layered structure creates an unusual pattern in 2026: two distinct cohorts are simultaneously at or past the succession threshold, with different urgency profiles, different documentation levels, and no institutional framework designed to handle either of them.

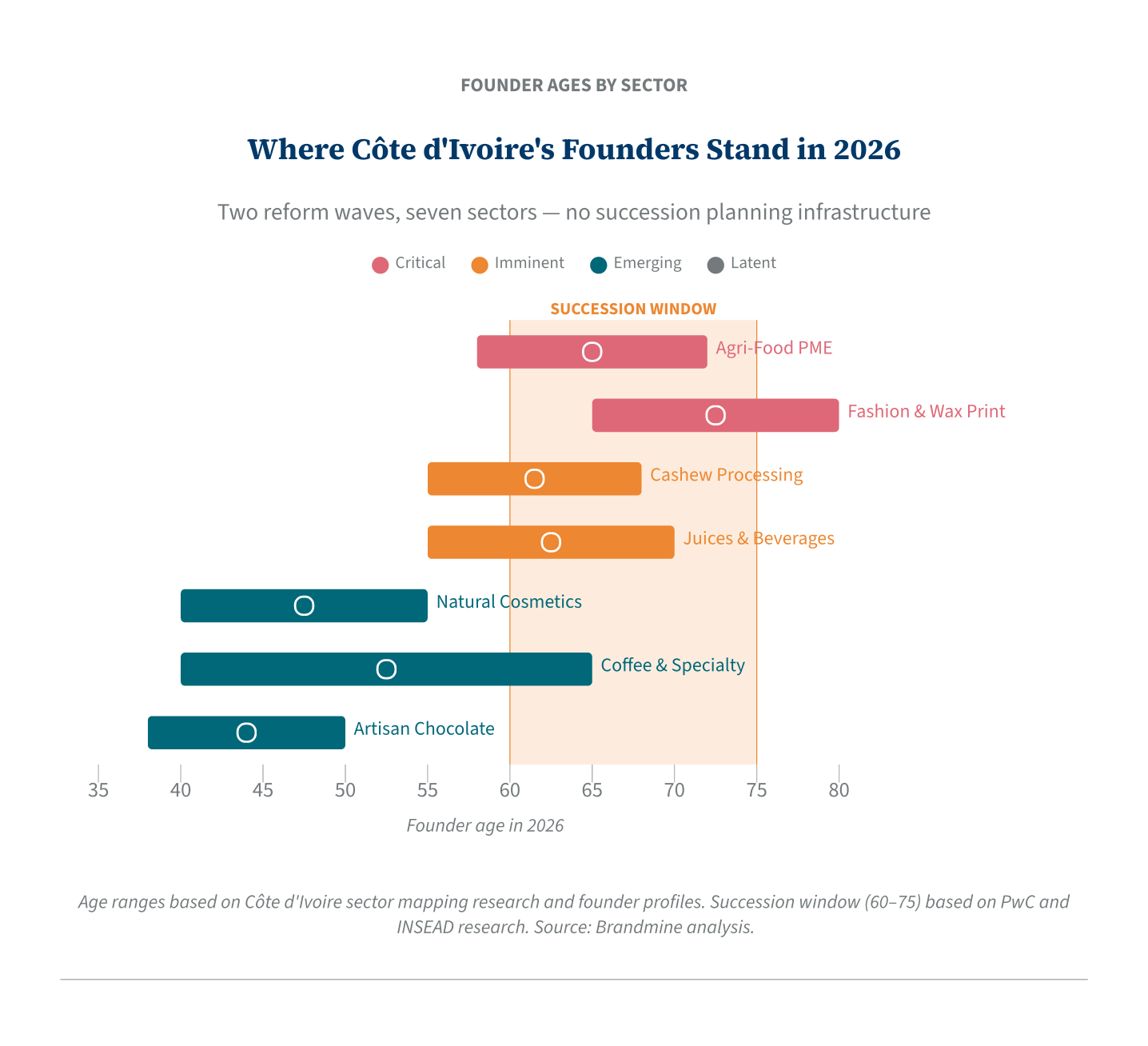

Seven sectors, one succession clock

Côte d’Ivoire’s viable founder-owned consumer sectors break across seven clusters, each with a distinct urgency rating shaped by the founding cohort and civil-war survival history of its dominant brands.

Cashew processing and branded nuts holds 8 to 12 founder-owned brands at commercial scale, with founders clustered between 55 and 68 years old. Urgency is imminent. Côte d’Ivoire is the world’s largest cashew producer, and its local processing capacity has quadrupled since 2014 — from 77,000 to 341,000 tonnes annually — as 37 industrial units came online under a government program targeting 45% local processing by 2026. That infrastructure was built largely by indigenous Ivorian founders navigating a commodity cycle that no Western analyst has systematically covered. Massogbé Touré Diabaté, who founded SITA in 2000 and its predecessor cooperative in 1981, is approximately 62 and holds multiple succession decisions pending across diversified holdings in rice, microfinance, and transport. A Sector Spotlight on cashew processing is on Brandmine’s research roadmap.

Agroalimentaire founder PMEs — cereals, infant nutrition, condiments — hold 5 to 10 brands at commercial scale, with founders aged 58 to 72. Urgency is critical. PKL/Protéines Kissèe-La is the sector’s defining case: ranked second in Ivorian infant cereals behind Danone, distributing across four ECOWAS markets, with an active capital raise — Keystone Partners mandated to place €4.5 million — that has been in the market since 2016. Founder Marie Diongoye Konaté is in her late sixties. The succession conversation is not theoretical; it is ongoing and time-sensitive.

Natural cosmetics, shea and cocoa beauty holds 10 to 15 brands, predominantly female-founded, with founders aged 40 to 55. Urgency is emerging. Côte d’Ivoire’s post-2011 reconstruction era produced a cluster of women-led cosmetics businesses — Adeba Nature (Laboratoires ADEBA), Yohou Cosmetic, Sahel Emmanuelle, Kanafrik — drawing on shea, cocoa butter, and indigenous botanical inputs, documented in Jeune Afrique, Elle Côte d’Ivoire, and Setalmaa. These founders are a decade or more from the succession window. The investment signal here is formation, not transition — the early documentation opportunity before the wave builds.

Fashion, wax print and African luxury apparel holds 8 to 15 brands at commercial scale, with founders spanning 40 to 76 years old. Two urgency levels apply simultaneously. Pathé’O — Aimé Pathé Ouédraogo — represents the legacy cohort at critical urgency: twenty boutiques across Côte d’Ivoire, Burkina Faso, Mali, Angola, Gabon, Cameroon, and Congo, built over four decades and still without a documented succession plan. A younger generation supported by Birimian Ventures represents an emerging cohort. The two urgency levels are not a contradiction; they are the structural shape of a sector where the founding generation and its successors are visible simultaneously.

Cocoa transformation and artisan chocolate holds 3 to 6 brands at commercial scale — a thin pool at the $5 million threshold today, though the cocoa-to-cosmetics adjacency that Abidjan-based founders are developing is expanding it. Axel-Emmanuel Gbaou founded Le Chocolatier Ivoirien around 2010 and is approximately 43 years old — emerging cohort, not yet approaching the succession window, but operating the only indigenous Ivorian brand building the “world’s largest cocoa producer with no consumer brand” narrative with any documentary depth.

Tropical juices and beverages holds 4 to 8 brands at commercial scale, with founders aged 55 to 70. Urgency is imminent. Ivoirienne des Produits Tropicaux (Fruit Nature) has operated for approximately 30 years in a space partially dominated by SOLIBRA/BGI’s licensed products, building its independence on local pineapple, mango, and bissap rather than imported concentrate. A younger edge is forming alongside it — N’ZanToukou, founded by Edith N’da Amoin, is turning artisanal koutoukou palm spirit into a packaged retail brand, the kind of formalisation that converts an informal tradition into an investable category. The founder layer is real and documented; the urgency aligns with the 1993–2005 cohort profile.

Coffee processing and specialty café holds 3 to 6 brands, with a mixed cohort spanning 40 to 65. Urgency is emerging. Despite Côte d’Ivoire being a significant robusta producer, only approximately 6,500 tonnes are roasted locally — against 9,000 tonnes lyophilised by Nestlé’s Abidjan facility. SATOR/Little Café, founded by the Bédié family in 2019, and Ivory Blue/Arabusta, founded by Mariam Braud-Mensah, represent the indigenous roasting layer, alongside Jasmin Café out of Grand-Bassam. The pattern is the same one that defines the country: a commodity exported raw at vast scale, with the branded consumer product an afterthought left to a handful of under-documented founders. Documentation is thinner here than in the top sectors, but the gap between production and branding is structurally compelling.

What Abidjan has built that no one knows to ask about

Three structural features distinguish Côte d’Ivoire’s succession challenge from any other market in Brandmine’s Africa coverage.

The first is the Lebanese filter. Approximately 40 percent of Côte d’Ivoire’s formal commercial economy is controlled by Lebanese family conglomerates — Fakhoury, Gandour/NPG, Khalil/Eurofind, Prima Center — that have operated across two to three generations and have no meaningful first-generation succession dynamic. Multi-generational family governance structures are already in place. When international capital or press attention turns to Côte d’Ivoire’s business community, it often encounters this layer first. The indigenous Ivorian founder cohort that built the processing economy sits behind and beneath it, documented in French, operating at smaller scales, and invisible to any analyst who doesn’t know the filter to apply.

The second is what might be called the civil war documentation paradox. The decade of conflict from 2002 to 2011 created exceptional Narrative Due Diligence material — virtually every surviving founder has a documented crisis arc involving supply chain disruption, toxic contamination, electoral violence, forced evacuation, or some combination of all four. That material exists in Jeune Afrique’s archive, in Abidjan.net, in Fratmat.info, in Classe Export. It is extensive, specific, and searchable. No institutional investor has ever systematically read it, because it exists entirely in French, and because the connection between civil-war business journalism and succession intelligence has never been made explicit to the people who need it.

The third is institutional absence. Birimian Ventures, Joliba Capital, Comoé Capital, and Adawale Partners are active in Côte d’Ivoire’s consumer and innovation economy. None has announced a transaction in cashew processing or artisan chocolate. No family business advisory infrastructure operates at the level of the 1993–2005 PME cohort. No formalized succession planning culture exists in either the Muslim north or the Christian and animist south. The infrastructure that would catch this transition wave when it breaks does not yet exist — and the wave is already in motion.

What the tailor won’t be able to leave behind

The succession signal in Côte d’Ivoire is not a forecast. It is already documented in specific names and specific facts.

Marie Diongoye Konaté’s capital raise is the most time-sensitive single data point in the country’s founder landscape. Keystone Partners has been mandated since 2016 to place a €4.5 million investment or partner stake in PKL. A transaction in which a partial stake changes hands will define the terms on which Konaté transitions from operator to shareholder. PKL’s Probo Koala crisis response, its ECOWAS distribution network, and its competitive position against Danone are documented facts that exist independently of whether any counterparty has assembled them before that conversation begins — which is exactly what Narrative Due Diligence produces.

Aimé Pathé Ouédraogo is 76. He built twenty boutiques across seven countries while Abidjan burned and rebuilt and burned again. The distributor relationships maintained in silk and wax print through a decade of embargo and curfew, the supplier trust accumulated across forty years of operating at the intersection of West African politics and luxury fashion, the institutional memory of how a multi-country luxury business survives when the city it was born in goes to war — none of it is documented in any language that institutional capital reads. None of it transfers through a conventional M&A process.

What is at stake in Côte d’Ivoire is not a market position. It is the knowledge held by the founders who built this market before anyone thought to ask — civil-war knowledge whose shelf life is measured not in quarters but in the number of years these founders remain able to talk about it. Aimé Pathé Ouédraogo is 76. The clock here is not abstract.