Skip to main content

Skip to main content

Cambodia: The Generation That Rebuilt Everything

Cambodia's entire founder-owned consumer brand ecosystem was built from literal zero after 1993 — not from a low base, but from a country the Khmer Rouge had intentionally de-commercialised. The founders who rebuilt it are now 55 to 72, and no institutional investor has ever mapped what they created.

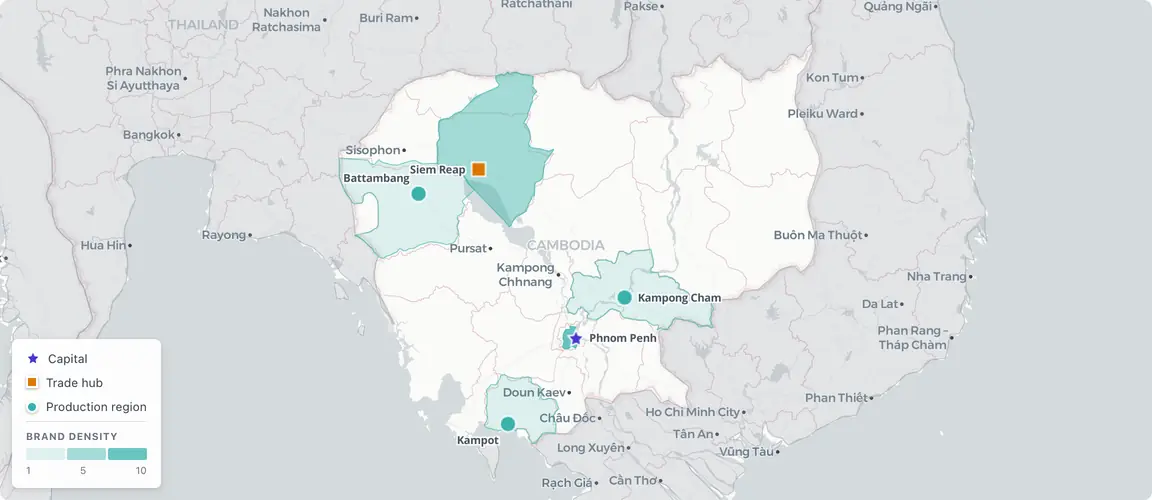

Capital and provenance: Cambodia's diaspora-return brand geography

The post-genocide generation, 1993–2024

In December 2024, Grab acquired Nham24, Cambodia’s leading food delivery platform — the country’s first significant consumer technology exit. The transaction proved something long theoretically possible but never demonstrated: regional strategic buyers will pay meaningful prices for scaled Cambodian consumer platforms. For the diaspora-return founders who built Cambodia’s hospitality and specialty food brands over three decades, the deal changed something. Exits are possible. The infrastructure to prepare for them barely exists.

Cambodia’s consumer brand ecosystem was not built from a low base. It was built from nothing. The Khmer Rouge’s systematic destruction of the commercial class between 1975 and 1979 — the forced evacuation of cities, the abolition of money, the killing or exile of merchants, professionals, and the educated — erased the country’s entire institutional memory of private commerce. When UN-supervised elections restored political stability in 1993 and Cambodia’s Investment Law opened the economy to private capital, the founders who answered were largely diaspora returnees from France, the United States, and Australia. They came home to a country that had been intentionally de-commercialized, carrying Western market knowledge, personal savings, and something more difficult to quantify: the specific ambition of people who had spent fifteen years waiting to rebuild what genocide erased.

No database has mapped the diaspora-return cohort that created Cambodia’s first generation of consumer brands. The founders of Shinta Mani hotels, Thalias restaurants, and Amru Rice have never appeared in PitchBook, Bloomberg Terminal, or Tracxn — and what they built represents exactly the kind of intelligence gap that Narrative Due Diligence was designed to fill.

The diaspora-return compression

Cambodia's consumer brands were built by people who had to rebuild everything — themselves first, then their country.

Cambodia’s succession wave has a shape unlike any other in Southeast Asia. China’s private sector wave spans from 1978 to 2001 — a 23-year founding window. India’s liberalisation cohort ran from 1991 to approximately 2005. Vietnam’s Đổi Mới reforms produced a founding wave from 1986 to 2000. Cambodia’s primary founding window — the period when the conditions existed to build founder-owned consumer brands at meaningful scale — ran from roughly 1993 to 2008: fifteen years.

Within that already-compressed window, the highest-succession-urgency cohort is narrower still. The diaspora-return founders who arrived between 1993 and 2000 — those who rebuilt their brands through the Asian financial crisis, the 2008 GFC, and then survived COVID’s annihilation of Cambodian tourism — are now between approximately 60 and 72 years old. They entered the succession window simultaneously. They have no institutional infrastructure to manage the transition. And they are the cohort whose NDD documentation is richest, because their founding stories begin not with an MBA and a business plan but with a flight from genocide and a decision to come back.

What makes Cambodia’s wave particularly unusual is not just its duration but its founding psychology. China’s Wave 1 entrepreneurs were responding to policy liberalisation in a country that had never fully erased its commercial traditions. India’s 1991 cohort inherited family business structures that traced back generations. Vietnam’s Đổi Mới founders built on regional trading networks that had survived the war years. Cambodia’s diaspora-return founders had none of that. The Khmer Rouge had not merely suppressed private commerce — they had physically eliminated the commercial class and abolished the institutional framework of money itself. The founders who came back after 1993 were building not on a low base but on a deliberately cleared site. The ambition required to do that is a specific kind of crisis-born resilience that no other founding cohort in Southeast Asia shares.

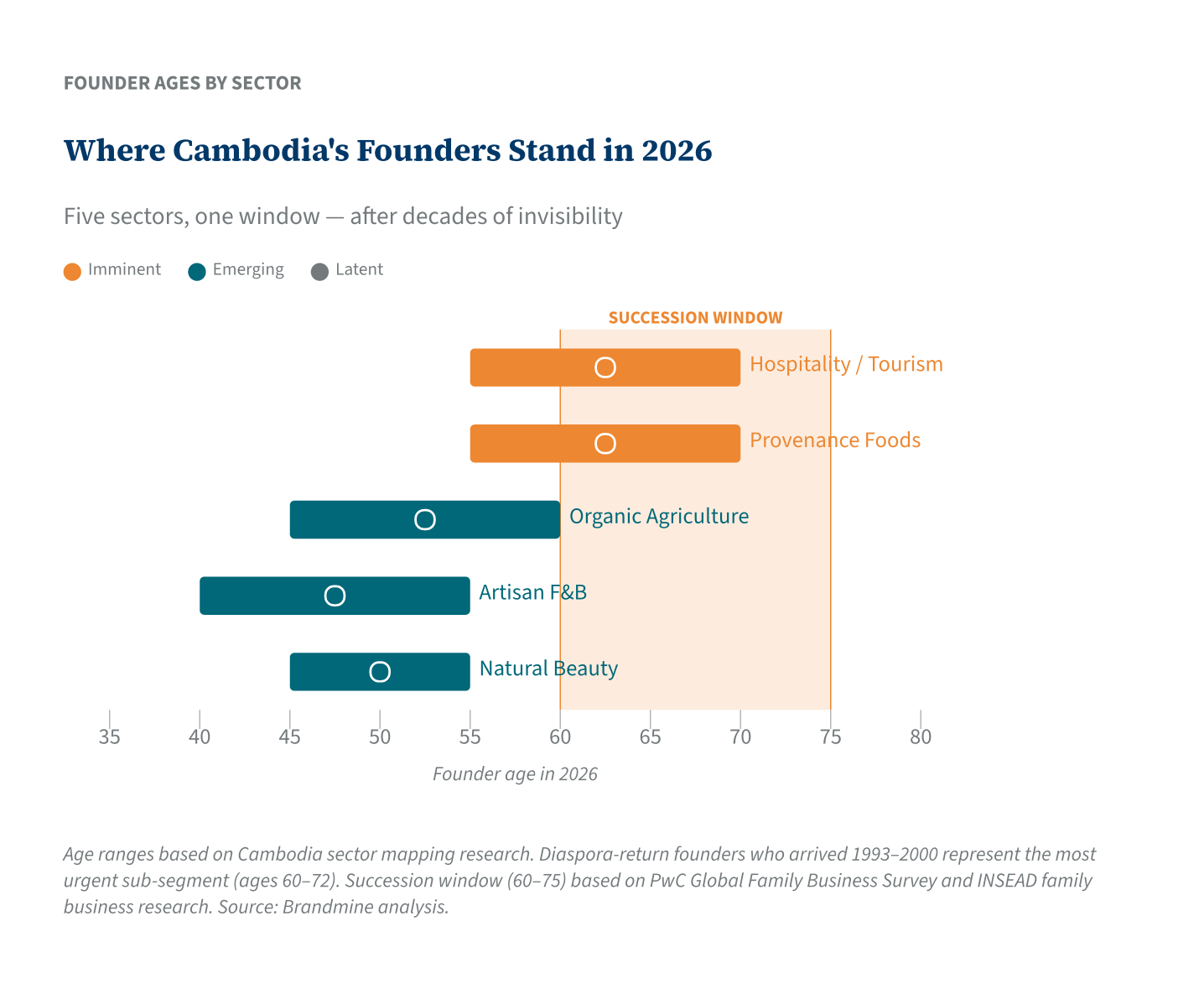

The domestic-market founders who arrived slightly later — those who built urban food and beverage, artisan retail, and wellness brands between 2001 and 2010 — are younger (roughly 48 to 62) and represent emerging rather than imminent succession pressure. But the hospitality and provenance food founders who represent Cambodia’s most commercially significant and internationally visible brands are ageing out now, without plans, without successors, and without any institutional investor having ever looked closely at what they built.

Hospitality, Kampot provenance, and the diaspora-return founders

Hospitality and tourism is Cambodia’s most urgent sector for succession intelligence. An estimated 8–15 founder-owned brands at meaningful commercial scale operate in this space — a figure that is almost certainly a floor; full sector scoping typically reveals pools 3 to 5 times larger. Founders skew 55–70, predominantly diaspora-return, and succession urgency is imminent across the cohort.

The sector’s NDD material is the richest of any in Cambodia — precisely because COVID produced the most severe stress test in the sector’s history. International arrivals fell from 6.6 million in 2019 to roughly 200,000 in 2020–21, a collapse that generated exactly the kind of crisis documentation that Narrative Due Diligence seeks: how did founders actually respond when 79% of revenue evaporated in a single year? Shinta Mani’s charitable foundation, led by Sokoun Chanpreda — a founder who fled Cambodia in 1970 as civil war erupted, was raised in Bangkok, studied at Boston University, and returned in the early 1990s — pivoted to food relief for thousands of displaced hospitality workers during the pandemic. Luu Meng’s Thalias Group, with more than 500 staff across its restaurants and hotel properties, partnered with the royal family on food distribution in Phnom Penh. Bodia, the natural beauty brand whose presence in hotel spas makes it a de facto part of the hospitality ecosystem, preserved its 300-person workforce without redundancies throughout the pandemic shutdown.

These are not press-release responses. They are decisions under existential pressure, documented in real time by English-language Cambodian business press, that no institutional investor has ever assembled into a coherent intelligence picture. The sector’s crisis arc — from Cambodia’s highest-ever tourism revenue in 2019 to near-zero arrivals in 2020–21 and the subsequent recovery to 6.7 million international arrivals in 2024 — is the most completely documented founder-resilience story in Southeast Asia’s hospitality sector.

Cambodia’s tourism sector generated $3.6 billion in revenue in 2024, representing 9.4% of GDP. It supports more than 1,028 registered hotels with 44,428 rooms, and the government has deployed a $50 million Cambodia Tourism Board fund to support sector recovery.

Specialty food — geographic provenance carries succession urgency that matches hospitality and adds a layer of international commercial validation that few sectors in any emerging market can claim. The Kampot Pepper story is Cambodia’s most internationally legible brand narrative: a geographic indicator product rebuilt from near-extinction after the Khmer Rouge destroyed an estimated 1 million pepper poles, organised through the Kampot Pepper Producers Association (formed 2009), reaching EU Protected Geographical Indication status in 2016, and winning six of nine possible three-star Great Taste Awards in 2022. That ratio — six of nine — does not happen by accident. It reflects the accumulation of artisan knowledge, terroir, and quality infrastructure that the sector has rebuilt over three decades from nothing.

GI-protected Kampong Speu palm sugar and Kep salt round out a provenance cluster with genuine global distribution and a brand story rooted in the same revival-from-genocide arc that makes Cambodian brands different from their regional peers. The sector has 5–8 founder-owned brands at meaningful commercial scale, with high founder-led concentration and founders predominantly in the 55–70 age band.

Confirel — founded in 2001 by Dr. Hay Ly Eang, a pharmacist trained in France who returned specifically to build Cambodia’s countryside economy — holds triple certification for EU, US, and Japanese organic markets, won the Palme d’Or at Natexpo Paris in 2005, and in 2025 holds Cambodia’s first international patent for a herbal tea infusion process. Institutional investors have never heard of it.

The provenance food sector does carry one complication that requires a decision before scoping proceeds: French and European expat founders are significantly represented across this sector and natural beauty, reflecting France’s post-colonial relationship with Cambodia and AFD/EU aid channel dynamics. A filter decision is required — whether to include long-term expat founders with Cambodian co-founders, or to restrict to Khmer-origin founders — before Brandmine invests full scoping time in these sectors. The intelligence value is present regardless of the filter; the filter determines which brands qualify for Brandmine’s core NDD methodology.

Organic and specialty agriculture anchors around Amru Rice, founded in 2011 by Song Saran — whose grandfather Li Song (李松) established a rice mill in Kampong Cham province that the Khmer Rouge destroyed during the genocide years. Song Saran rebuilt the family’s rice business not as a restoration but as a scaled organic export operation: approximately $45 million in annual revenue, roughly 90% market share in Cambodia’s organic rice exports, 25,000 contracted farmers across 11 provinces, and exports to more than 52 countries, backed by IFC debt financing and Ex-Im Bank credit. Revenue grew from $10 million in 2012 to $38 million by 2018. Song Saran has served as President of the Cambodia Rice Federation. No institutional investor has documented this story; no succession plan is publicly visible, though at approximately 45–55 Song Saran sits in the emerging rather than imminent succession band.

Food and beverage — artisan and premium represents a younger founder cohort (approximately 40–55) with emerging rather than imminent succession urgency. Brown Coffee, with more than 39 outlets and Sino-Khmer founders, anchors the sector at meaningful commercial scale and represents Cambodia’s developing urban middle class as both market and founding base. Luu Meng’s restaurant group — Malis (Cambodian fine dining), Topaz (French), and Khéma (European brasserie) — sits at the intersection of the hospitality and food sectors and benefits from the same COVID crisis documentation. The commercial fit for succession intelligence is moderate, given the founder age band, but brand-level intelligence has value for regional F&B acquirers and strategic partners tracking Cambodia’s urban dining market.

Natural beauty and wellness has a qualifying pool of 2–4 brands, with Bodia as the clearest example: founded by a Cambodian-French partnership, ISO-certified, with more than 300 staff and estimated revenue in the $5–15 million range. Bodia’s hotel spa partnerships make it an organic part of the hospitality ecosystem — the two sectors’ succession dynamics overlap. ASEAN business awards and ISO certification document institutional credibility that neither a PitchBook entry nor a Bloomberg terminal record captures. The French-founder filter decision applies to this sector as well, pending CEO direction.

Building on a site the Khmer Rouge deliberately cleared

Cambodia’s succession wave does not break the way India’s, China’s, or Vietnam’s does, because the founding conditions were categorically different. In those markets, first-generation founders built on at least some institutional foundation — family business traditions stretching back generations, established banking relationships, nascent PE ecosystems, some cultural framework for managing succession. In Cambodia, there was nothing. The genocide did not merely disrupt the commercial class; it erased it. The founders who returned after 1993 built with no predecessors, no templates, no mentors from the previous generation of Cambodian entrepreneurs — because that generation was gone.

The succession infrastructure gap is not simply a matter of underdeveloped family business advisory services. Cambodia’s Trust Law was enacted in 2018 — a full generation after the founding wave began — and has accumulated only approximately 1,175 registered trusts in a country of 17 million people. There are no PE firms systematically targeting Cambodian consumer brand transitions. Leopard Capital, which once operated in Cambodia, has wound down citing poor exit environment. Mekong Strategic Partners and similar vehicles operate at venture scale and focus on technology, not consumer brands. The IFC concentrates on financial services infrastructure and agribusiness at the supply chain level.

The adverse selection from CPP entanglement is significant: the most visible Cambodian brands are often the least investable for institutional capital, while genuinely founder-owned brands with clean governance structures remain invisible. Diaspora-return founders with French or American citizenship offer cleaner governance and greater accessibility — a priority sub-segment precisely because their backgrounds are more legible to foreign capital.

The single most important recent event in understanding Cambodia’s succession dynamics is the Grab/Nham24 acquisition in December 2024. It is Cambodia’s first major consumer exit. The deal demonstrates that regional strategic buyers exist, that they will pay for scaled Cambodian consumer platforms, and that the country’s consumer economy has reached the maturity threshold where exits are commercially viable. What the deal does not demonstrate is that the infrastructure exists to prepare Cambodia’s founder cohort for those exits. It doesn’t. The absence is precisely the opportunity.

The window and what it is

Cambodia’s diaspora-return founders built brands in the hardest possible conditions — from a country with no commercial infrastructure, through a decade of post-conflict instability, through the Asian financial crisis, through the 2008 GFC, and then through the most catastrophic tourism collapse in Southeast Asian history. The ones who survived all of it are now entering the succession window without a playbook, without a succession planning infrastructure, and without institutional investors who understand what they built or how they built it.

Fewer than 15% of Cambodian founders have any formal succession plan — below the Asia-Pacific average of 24%, which is itself not a high bar. The Trust Law has accumulated only ~1,175 registered trusts in a country of 17 million, and no family business advisory firms operate in Cambodia targeting the consumer sector. For the 60–72 cohort, the transition is not hypothetical — it is imminent, and it will happen without infrastructure.

The Grab/Nham24 deal proved that exits are possible in Cambodia. But the intelligence needed to move through that door — who the founders are, what crises they survived, whether they have any transition plan — exists in local press coverage, in GI certifications filed in Brussels, and in the COVID pivot decisions that Shinta Mani and Thalias made in real time in 2020–21. None of it is in any investment database.

The brand may survive a founder’s departure; the story that created its value does not transfer automatically.

That intelligence is being assembled for the first time. The diaspora-return cohort that built Cambodia’s consumer brand ecosystem is between 60 and 72. Grab’s arrival in December 2024 set the reference price for the next transaction of this kind.

Cambodia is not a market to enter. It is a market to document before the founders who rebuilt it from zero finish handing it over.