Skip to main content

Skip to main content

Argentina: The Crisis That Never Stops Teaching

Argentina has 875 registered wineries, a chocolate cluster in Patagonia that exports to Switzerland, and a generation of consumer-brand founders who survived hyperinflation, sovereign default, currency controls, and 211% annual inflation -- all within one career. Fewer than 34% have a succession plan. The window is open, and the first institutional buyer is already inside.

Buenos Aires leather, Mendoza wine, and Patagonia premium: Argentina's three-pole succession map

The default-survivor generation, 2001–2024

Argentina has 875 registered wineries, and in 2025 alone, three of its most prominent founder-owned bodegas hit succession crises simultaneously – one entering creditor protection, one sold to a political insider’s consortium, one embroiled in a family lawsuit alleging gender discrimination in asset distribution. This is not a sector in trouble. It is a sector revealing what happens when a generation of founders, forged in the convertibility boom of the 1990s and hardened by five macroeconomic crises since, reaches the transition window without a plan.

Whitepaper No 1 documents a synchronized transition wave across emerging markets: reform-era founders ageing out simultaneously, institutional investors unprepared. Argentina is what that thesis looks like in a country where every surviving founder carries four to five documented crisis responses – hyperinflation, sovereign default, currency controls, peso crashes, and 211% annual inflation – and where the succession infrastructure gap is not a future risk but a present reality unfolding in real time.

The intelligence exists. It is scattered across Forbes Argentina, Apertura, El Cronista, Ambito Financiero, and decades of Argentine business journalism – one of the most extensive and digitized business press traditions in Latin America. What does not exist is a synthesis: which sectors contain founder-owned brands at commercial scale, which founders are in the succession window, and where the transition pressure is highest. That synthesis is what follows.

Menem’s convertibility cohort and the Kirchner rebuilders

The dominant obstacle is the founder's inability to relinquish control.

Argentina’s succession wave is not a single compression event. It is a layered wave – two distinct founding cohorts, created by two different reform eras, hitting the transition window at different speeds.

The first layer formed during the Menem convertibility era (1991–2001). When one peso equalled one dollar, a generation of consumer entrepreneurs launched wineries, leather goods companies, chocolate makers, and specialty food brands. The artificial stability made long-term investment in product quality rational for the first time – and it attracted European-trained winemakers, Italian-tradition leatherworkers, and Swiss-influenced chocolatiers back to Argentina or into the market. Founders from this era are now 60 to 77 years old. They are squarely in the succession danger zone.

The second layer formed during the Kirchner rebuilding era (2003–2015), when crisis-born entrepreneurs emerged from the wreckage of the 2001 sovereign default. Cachafaz – now one of Argentina’s premium alfajor brands and Havanna’s principal rival – was literally born during the 2001 collapse, when a widowed mother began making alfajores in her kitchen in Liniers to survive. Founders from this era are younger: 48 to 63 today, with the earlier cohort beginning to enter the succession window.

What makes Argentina’s wave shape distinctive is not just the layering but the serial crisis testing. Unlike Mongolia’s compressed wave, where the entire founder cohort was created in two to three years, or Russia’s privatisation wave, where oligarch families had at least a decade to experiment with governance structures, Argentina’s founders have been stress-tested repeatedly across their entire careers. The 1989 hyperinflation (3,079%), the 2001 sovereign default, the 2011–2015 currency controls, the 2018 peso crash, and the 2023 inflation spike (211%) each demanded different survival strategies: dollarisation, barter networks, export pivots, import substitution, stockpiling. Every surviving founder has four to five documented crisis responses. No other country in Brandmine’s coverage produces this density of Narrative Due Diligence material.

The result is a founder cohort with extraordinary resilience – and an extraordinary succession gap. Only 30% of Argentine family businesses survive to the second generation. Fewer than 34% have formal succession plans. The cultural resistance is specific and well-documented: the dominant obstacle, according to PwC and IAE Business School research, is the founder’s inability to relinquish control. In a country where the founder personally navigated hyperinflation, a sovereign default, and 211% annual inflation, the reluctance to hand over is not irrational. It is the logical consequence of a career built on personal crisis management.

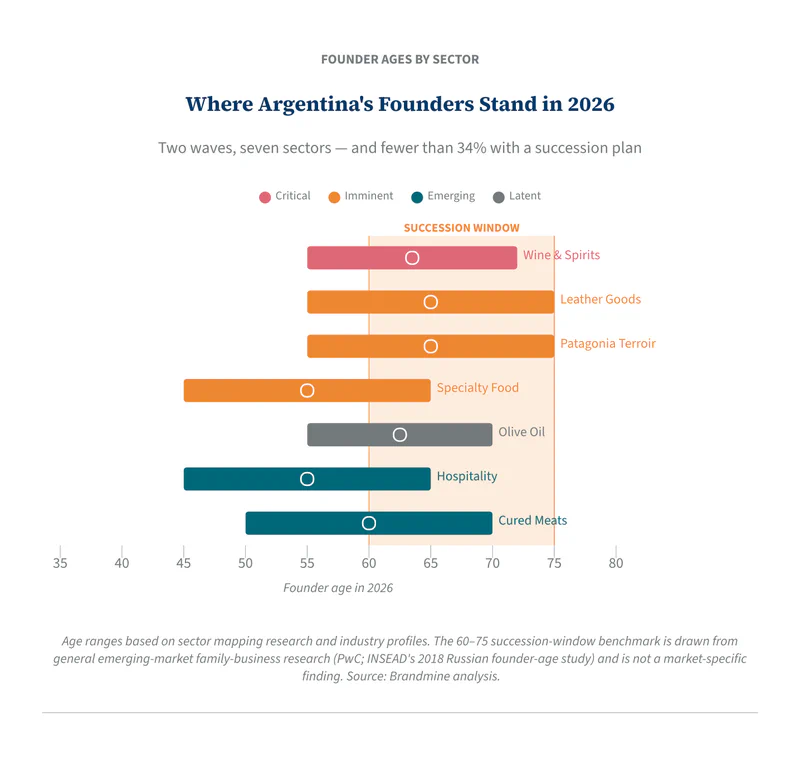

Wine, specialty food, and Patagonia terroir — 70 to 120 brands

Brandmine’s sector mapping identified twelve candidate consumer sectors in Argentina. Seven show meaningful founder-owned brand activity at commercial scale. The top three – wine, specialty food, and Patagonia terroir – collectively contain an estimated 70 to 120 founder-owned brands meeting transition wave criteria. Here is where the wave is breaking.

The sector in acute distress – and the buying window it creates

Argentina’s wine sector is in its worst crisis in fifteen years. Exports hit $810 million in 2023 – the lowest since 2014 – and fell a further 6.8% by volume in 2025. An estimated 40 to 70 founder-owned wineries operate at commercial scale, with founders aged 55 to 72 – succession urgency: critical. Three succession or governance events in 2025 alone signal the crisis is structural: Bodega Norton entered concurso preventivo with over $30 million in debt after internal family conflict; Bodega Atamisque was sold to a group led by a former government minister; and the Mendoza Supreme Court ordered José Alberto Zuccardi to pay $12 million to his sister Cristina after ruling that their parents’ asset distribution had favoured the son – applying a gender perspective that sent shockwaves through Argentine family business circles. These are not isolated failures. They are the first visible cracks in a sector where the Malbec revolution’s founding generation is exiting simultaneously.

The brands that were born in crisis – and have never known stability

Argentina’s specialty food sector – alfajores, dulce de leche, chacinados, and artisan products – contains an estimated 15 to 25 founder-owned brands at commercial scale, with founders aged 45 to 65 – succession urgency: imminent. The sector’s most compelling story is also its most opaque: Cachafaz, founded by the Alcaraz brothers – one of whom has since sold his stake – who have never given a press interview, grew from their widowed mother’s kitchen during the 2001 crisis to become Havanna’s main premium rival, exporting to Brazil, Chile, Spain, and the United States. A hundred regional alfajor brands operate nationally, and the World Alfajor Championship creates international visibility for artisan producers that no database has captured.

The terroir cluster that sells chocolate to Switzerland

Patagonia’s terroir brands – chocolate, berries, craft beer, smoked products – contain an estimated 15 to 25 founder-owned brands, with founders aged 55 to 75 – succession urgency: imminent. The crown jewel is Rapanui/Franui: 1,400 employees, exports to 25 countries including Switzerland, a new $10 million plant in Pilar and a EUR 3.5 million facility in Valencia, Spain. The Bariloche chocolate cluster – Mamuschka, Del Turista, Fenoglio – represents a concentrated geography of founder-owned brands within a single town, each with succession dynamics underway. Patagonia as a terroir marker carries validated international pricing power: when an Argentine chocolate maker sells to Switzerland, the origin premium is real.

The leather houses that said no to LVMH

Argentina’s leather goods sector contains an estimated 15 to 25 founder-owned brands, with founders aged 55 to 75 – succession urgency: imminent. Prune operates over a hundred stores with a second-generation transition already underway. La Martina rejected acquisition offers from both LVMH and Adidas – a founder’s decision that preserved independence but deferred the succession question. The sector faces structural headwinds (exports collapsed from $1 billion to $250 million over two decades), but individual brands with international distribution have decoupled from the industry decline.

The sectors still forming

Three additional sectors warrant monitoring. Olive oil (8–15 founder-owned brands, founders aged 55–70, succession urgency: latent) contains standout targets but remains predominantly a bulk commodity export sector. Boutique hospitality and wine tourism (10–15 founder-owned brands, founders aged 45–65, succession urgency: emerging) has proven exit precedents – the Cavas Wine Lodge acquisition validates the model – but operates as a different asset class. Cured meats from Tandil and Colonia Caroya (10–20 family businesses, founders aged 50–70, succession urgency: emerging) represent Italian-immigrant multigenerational enterprises with Denominacion de Origen protection – different dynamics from first-generation founder-owned brands, but the transition pressures are converging.

Five crises, tacit knowledge, and the Zuccardi ruling

The layered wave structure means Argentina’s succession crisis arrives with a specific character that distinguishes it from any other market in Brandmine’s coverage.

The serial crisis testing that made these founders extraordinary also made the succession gap more acute. A founder who personally navigated hyperinflation at 3,079%, a sovereign default that froze bank accounts, and inflation at 211% has accumulated crisis management knowledge that is almost entirely tacit. It lives in relationships with suppliers who extend credit during peso crashes, in reflexes honed by decades of overnight price adjustments, in the ability to read political signals months before policy changes. None of this transfers in an org chart handover. The Narrative Due Diligence material is the richest in Latin America – but the very depth of crisis experience that makes these founders exceptional makes succession planning harder.

The talent constraint operates differently in Argentina than in smaller markets. Unlike Mongolia’s “talent puddle,” Argentina has a deep professional class – but the pool of executives who have both the crisis management experience and the entrepreneurial instinct to run a founder-built consumer brand through a leadership transition is far smaller than the country’s GDP would suggest. The 67 distinct fiscal obligations that Argentine businesses face create an operational complexity that only experienced operators can navigate. Founders know this. It is part of why they do not let go.

The Zuccardi ruling is the signal event. This is not a small family business failing to plan. Familia Zuccardi is the fifth-largest wine exporter in Argentina, a Forbes Top 50 winery, with an olive oil division spanning 300 hectares. The Mendoza Supreme Court’s decision – ordering the son to pay $12 million to his sister after finding that their parents had favoured the male heir in asset distribution – is a preview of what the layered wave produces when first-generation wealth meets the absence of institutional succession infrastructure in a country where family governance traditions are strong but formal business succession frameworks are not. Norton’s creditor protection and Atamisque’s distress sale confirm the pattern: the wave is not coming. It has arrived.

L Catterton is already in Buenos Aires

One institutional buyer has understood this thesis for years. L Catterton – LVMH’s private equity arm – holds positions in Rapsodia, Luigi Bosca, Caro Cuore, and Baby Cottons. Grupo Perez Companc, through Molinos Rio de la Plata, is the dominant domestic strategic acquirer and is actively seeking consumer brand acquisitions. Linzor Capital Partners, Advent International, and Southern Cross Group maintain Argentine consumer deal teams. The intelligence gap is not total – it is asymmetric. A handful of buyers are already inside the window. Everyone else is still looking at Brazil and Mexico.

The Milei government’s cepo removal in April 2025 – individuals and businesses permitted to buy dollars freely for the first time since 2019 – and the $20 billion IMF Extended Fund Facility approved the same week are changing the calculus. For the first time in a decade, foreign capital can enter Argentine consumer brands without navigating a labyrinth of currency restrictions. The investment climate normalisation means the window of asymmetric access – distressed valuations plus regulatory barriers that kept most institutional capital out – is narrowing. The buyers who moved during the cepo years acquired at prices that the post-cepo market will not offer again.

What disappears when a founder exits without a plan is not just a brand. It is the crisis management knowledge that took five macroeconomic collapses to accumulate. The supplier relationships that survived hyperinflation. The export networks built despite currency controls. The reflexes that kept a business alive through a sovereign default. By the time these brands surface through conventional channels – if they ever do – the founders who carry this knowledge will have retired, sold, or simply closed.

Argentina’s founder-owned brands have been documented everywhere except where institutional capital looks — in Forbes Argentina, in Apertura, in decades of business press that speak the language of half a billion consumers. The buyer who waits for the next Zuccardi ruling, the next Norton-style concurso, the next Atamisque sale will be paying post-cepo prices to intermediaries who have already sorted the cohort. The asymmetric-access discount is a 2025 asset, not a 2027 one.