Skip to main content

Skip to main content

Beast

Strip the narrative and you have a candle from a Zhejiang factory. Amber Xiang built 野兽派 on one thesis: Chinese consumers pay for the story, not just the product. COVID emptied the stores. The OEM scandal shredded credibility. Neither killed it. By 2024, Beast led domestic fragrance on Tmall — the only Chinese-origin brand above ~3.5% share.

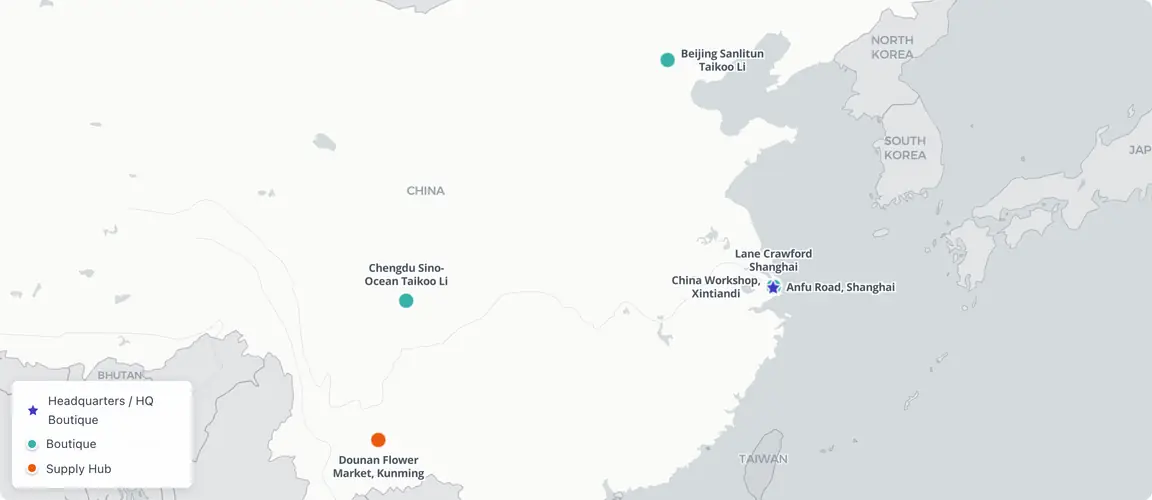

From Anfu Road to Four Cities: Beast's Retail Arc

Story as strategy — and the two crises that tested it

The story that started on Weibo

On 29 November 2011, Amber Xiang opened a Weibo account and began selling flowers. Not arrangements — stories wrapped in flowers. Each bouquet came with a narrative: a reference to a painting, a literary character, a specific emotional state. There was no storefront, no inventory system, and no precedent for this model in China’s flower market.

Xiang had left a position as marketing director at Dragon TV. Her co-founder, Zhuang Ying, had left a senior role at a global cosmetics group. Both were approaching forty. The thesis they were betting on — that Chinese consumers would pay a premium for the story around a product, not just the product itself — had no proven equivalent in domestic luxury.

The timing was structurally favourable. Weibo in 2011 was at its peak as a discovery platform, before WeChat had migrated Chinese social commerce to a private-channel model. A brand that could build on Weibo’s open social graph — where a single compelling post could reach millions of strangers — had infrastructure that no physical store could replicate. Beast was a Weibo-native business before that was a recognized model. Its founding category — luxury floristry — was also near-absent in China at the time. The market Xiang and Ying were entering did not yet exist at scale; they were building the demand, not competing for an established one.

Within six months, the Weibo account had 100,000 followers. The breakthrough format was the Monet’s Garden box: an art-referencing flower arrangement priced at a significant premium to the market. Consumers weren’t buying a flower box. They were buying an aesthetic position — an entry point into a curatorial sensibility that Xiang and Ying were broadcasting daily through the account’s editorial voice. By the end of 2012, Beast had 180,000 followers and had been named a Top 10 Weibo user. The online channel was validated. The next test was whether the story could survive physical retail.

The Lane Crawford proof point

On 10 October 2013, The BEAST House opened inside Lane Crawford Shanghai — the luxury department store whose tenants were, at that point, exclusively Western or Hong Kong brands. Beast was the first China-origin brand to hold dedicated space in the store. The placement was not incidental. It was the brand’s argument made visible: a Weibo-native Chinese startup occupying the same retail floor as European luxury maisons.

Series A funding followed in 2014, led by Matrix Partners China. A Series B round in December 2015 brought H Capital and Trustbridge into the cap table. The capital enabled what the thesis required — not manufacturing differentiation (Beast’s products are manufactured at contract factories, as most lifestyle brands’ products are), but story infrastructure: museum licensing deals, celebrity collaborations, a Tmall flagship with curated campaign architecture.

The celebrity strategy ran through 2014 and 2015 with floristry for the weddings of Zhou Xun, Zhao Youting, Gao Yuanyuan, and Angelababy. These were not endorsement deals. They were editorial placements — Beast flowers at the most-photographed moments in Chinese celebrity culture, reinforcing the brand’s positioning as the domestic luxury floristry reference.

In February 2015, the Tmall flagship launched, generating RMB 14M in first-year sales. The e-commerce channel did not replace the boutique strategy — it ran parallel to it. Beast’s retail presence served as a physical expression of the brand’s curatorial identity; the Tmall channel converted that brand awareness into purchasable volume. The two-channel architecture — boutique credibility, e-commerce scale — would become the structural template for the brand’s next decade.

Museum licensing and the pre-crisis peak

The 2016 Van Gogh Museum licensed series was a structural marker. No Chinese lifestyle brand had previously secured a major Western-museum collaboration of this type. The series signalled that Beast’s art-referencing model was not merely aesthetic posturing — the Van Gogh Museum had assessed the partnership and found it credible. For a brand built on the premise that story confers value, a Western cultural institution’s formal endorsement was a significant validation of the model’s legitimacy to an international audience.

By 2017, Tmall sales had reached RMB 160M. The brand had split into sub-labels: Ms Beast for gifting and personal lifestyle, Beast Home for residential objects. The 2018 T-B-H sub-brand and the 2019 V&A Museum home series extended the model further. When the boutique-hotel concept — Beast x Gubi House on Taojiang Road — opened in 2019, and Wallpaper and Design Anthology ran coverage, Beast had achieved something rare for a domestic Chinese consumer brand: genuine international design-press credibility.

The brand’s position entering 2020 was strong. Its thesis — story-led domestic luxury, culturally self-confident, museum-credentialed, celebrity-adjacent — appeared structurally sound. Then the stores went dark.

The first crisis: COVID and the fragrance pivot

Spring 2020 lockdowns closed Beast’s boutiques and sealed its warehouse. Perishable floristry inventory — the category on which the brand had been built — had no buyers and no path to market. Amber Xiang described it as “the hardest moment in Beast’s 9-year history.”

The pivot decision was strategic in form but intuitive in character: launch a healing fragrance product, the Golden Teardrop, designed to channel quarantine anxiety into a purchasable emotional object.

The logic followed directly from Beast’s founding thesis. If consumers would pay for a story around flowers, they would pay for a story around a fragrance — especially a fragrance that acknowledged, rather than ignored, the emotional reality of a locked-down spring.

The bet held. The Golden Teardrop gave Beast a product category that was both compatible with its existing story model and immune to the perishability constraint that had made 2020 so damaging. Fragrance could be warehoused. It could ship. It could be sold without a boutique.

The thesis was confirmed at scale on 29 November 2021 — the brand’s 10th anniversary. The Unrequited Love fragrance, framed as a farewell to an era, sold RMB 10M in its first hour. The COVID pivot had not been a crisis workaround. It had been a category pivot that would define the brand’s next decade.

The second crisis: the OEM scandal

In 2022, investigative reporting revealed that Beast fragrance products shared a contract factory — 湖州御梵 — with Miniso, the budget lifestyle retailer. The price differential was roughly 14x. A concurrent mislabelled-tea regulatory fine added a second credibility layer. Over 360 million Weibo views at the scandal’s peak made this the largest public test of Beast’s story thesis in the brand’s history.

The core charge was not about product safety. It was about whether the story justified the price. If a Beast candle and a Miniso candle came from the same factory, was the story worth the premium?

The structural context matters here. OEM manufacturing — producing goods at third-party factories that serve multiple clients — is standard practice across the global lifestyle and fragrance industry. LVMH subsidiaries, independent perfumers, and mass-market retailers all draw from overlapping manufacturing ecosystems. The scandal did not reveal a Beast-specific deception. It revealed that Beast’s premium was allocated to design, curation, and narrative construction, not to proprietary manufacturing infrastructure. That is a legitimate business model. But it required consumers to understand and accept the distinction — to believe that what they were paying for was the editorial layer, not the factory floor.

The brand did not issue a comprehensive public rebuttal. What it did instead was continue building — new products, new museum collaborations, and a positioning shift in 2023 toward Chinese cultural heritage over European aesthetic reference. The argument by action: the story’s value was in the design decisions, the licensing agreements, the editorial choices that surrounded the physical product. The question was whether Chinese consumers would accept that argument at scale.

The resolution: RMB 418M and a repositioned story

By 2024, the answer was measurable. According to Mirror Insight data reported by Jiemian, Beast’s Taobao and Tmall fragrance sales reached RMB 418M — making it the only domestic Chinese brand to hold above approximately 3.5% category share in domestic fragrance. International luxury fragrance houses dominated the category; Beast was the only Chinese-origin brand with a significant domestic foothold.

The domestic fragrance category in China is predominantly held by French and European maisons — Chanel, Dior, Jo Malone, Diptyque. These brands carry decades of institutional narrative. Beast’s position as the sole domestic competitor with a meaningful share is therefore a structural anomaly. It holds that position without the heritage provenance that justifies a Maison Margiela or Acqua di Parma premium. What it has instead is cultural specificity — fragrance concepts, naming conventions, and campaign architecture designed for a Chinese consumer who does not experience luxury through a Western-filtered lens.

The store count told a more cautious story. At its 2023 peak, Beast operated 47 boutiques. By end of 2024, the number had contracted to 41 — a reflection of the consumption downgrade pressure affecting premium discretionary spending across Chinese retail, not a Beast-specific deterioration. The broader luxury sector in China saw similar boutique rationalizations in the same period.

The February 2025 opening of China Workshop at Xintiandi, Shanghai, marked the clearest repositioning signal since the COVID fragrance pivot. Where the Van Gogh and V&A collaborations had anchored Beast’s story in Western art institutional credibility, the China Workshop pivoted toward Chinese heritage craft — traditional techniques, domestic artisans, materials with Chinese cultural provenance. The OEM scandal had raised a question about authenticity. The repositioning was, in part, an answer: the story Beast was now telling was one that Zhejiang factory origins could not easily undermine, because it was rooted in Chinese craft traditions rather than in the brand’s distance from Chinese manufacturing reality.

The thesis, tested twice

Beast’s 14-year history is a sequence of proof points for a single commercial thesis: Chinese consumers will pay for the story around a product, provided the story is precise, aesthetically coherent, and culturally self-confident enough to sustain scrutiny.

Both the COVID crisis and the OEM scandal tested that thesis directly. COVID tested it by removing the product category entirely. The OEM scandal tested it by revealing that the product’s physical basis was shared with a brand positioned at one-fourteenth the price point. The brand survived both because, in each case, the strategic response was to build a more defensible story — not to abandon the story model.

What the RMB 418M figure demonstrates is that the domestic Chinese market for narrative-led lifestyle luxury is real, large, and durable enough to sustain a category leader. What the 47→41 boutique contraction demonstrates is that the premium discretionary segment is not immune to macroeconomic pressure. Beast enters 2025 as the dominant domestic fragrance brand on China’s largest e-commerce platform, with a heritage-craft repositioning underway and a founder who has spent 14 years building the thesis that makes the brand worth the premium.

Strip the narrative and you have a candle from a Zhejiang factory. The question Beast has always been answering is whether the narrative is worth something. By 2024, the market had answered: yes, at scale.